Blog

A Guide to Understanding the Debt Collection Process

May 8, 2025

Table of Contents:

Introduction: A Guide to Understanding the Debt Collection Process

What Is the Debt Collection Process?

Step-by-Step Collection Process

Credit Card Collection Timeline

Handling Disputes

Legal Compliance in Collections

Best Practices for Success

Automate Collections with FinanceOps.ai

Why FinanceOps.ai?

FAQs

Introduction: A Guide to Understanding the Debt Collection Process

The debt collection process is crucial for protecting cash flow and minimizing bad debt. Whether you’re chasing overdue invoices or managing consumer debt, a clear, compliant strategy ensures timely recovery and preserves relationships.

Fact: Recovery rates drop by 50% after six months of delinquency, and by 75% after one year. Early action isn’t optional, it’s critical.

This guide covers every stage of collections, from first contact to legal action, plus dispute handling, compliance tips, and automation strategies that modern teams use to stay ahead.

What Is the Debt Collection Process?

The debt collection process is a series of structured steps to recover unpaid balances. Whether you’re collecting on credit cards, loans, or B2B invoices, the goal is the same: recover funds efficiently, stay compliant, and protect your brand. A strong understanding of this process ensures that no account falls through the cracks and that every stage is handled with clarity and control.

Step-by-Step Collection Process

Review the Account: Verify the debt amount and terms. Gather contracts, invoices, and history.

Send Early Reminders: Notify the debtor within days of the missed payment via SMS, email, or calls.

Negotiate Payment Plans: Offer options like installments, deferments, or settlements to help resolve the debt.

Issue a Final Demand Letter: Set a clear deadline and outline potential legal action if payment is not made.

Pursue Legal Collection: If unresolved, initiate claims, file lawsuits, or partner with attorneys to enforce collection.

Close the Case: Resolve through full repayment, negotiated settlement, or write-off after exhausting all options.

Credit Card Collection Timeline

0–30 Days: Gentle reminders via email, app, or SMS to encourage prompt repayment.

31–90 Days: Direct outreach begins with more frequent follow-ups, offering payment options or hardship plans.

91–180 Days: Escalation to internal collections or third-party agencies with potential settlement offers.

180+ Days: Charged off as a loss. Debt may be sold or assigned for external recovery. Legal action may be considered.

Automating early-stage reminders can significantly reduce charge-offs and increase recovery.

Handling Disputes

Disputes must pause collection efforts until resolved. Common triggers include:

Incorrect amount or due dates

Fraud or unauthorized transactions

Identity mismatches or outdated records

Dispute Resolution Steps:

Validate the debt with proper documentation

Pause collections during the investigation period

Resolve or escalate the issue internally

Resume collections once the issue is verified or settled

Efficient dispute workflows reduce legal risk and protect your customer relationships while maintaining compliance.

Legal Compliance in Collections

To stay compliant, collection efforts must follow:

FDCPA: Governs contact frequency, tone, disclosures, and timing to prevent harassment.

FCRA: Controls credit reporting and mandates accurate data handling, especially during disputes.

State Laws: May require debt collector licensing, additional notices, and stricter communication protocols.

Non-compliance consequences:

Lawsuits and fines

Brand reputation damage

Regulatory scrutiny and potential shutdowns

Best Practices for Successful Debt Collection

Act Fast – Early outreach increases the likelihood of recovery before the debt ages out.

Stay Human – Empathetic communication encourages cooperation and reduces resistance.

Offer Options – Flexible payment plans cater to different financial situations.

Document Everything – Maintain a full audit trail of all communications and agreements.

Use Automation – Scale operations with software that sends reminders, tracks status, and handles workflows efficiently.

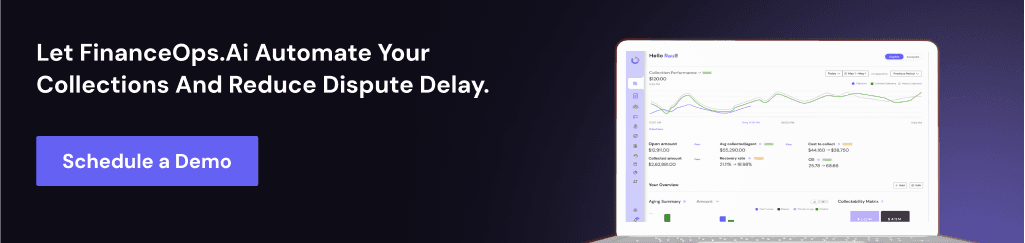

Automate Collections with FinanceOps.ai

FinanceOps.ai is your AI-first collections engine for fast, compliant recovery, without the overhead.

Multichannel outreach via SMS, email, and voice for maximum reach and engagement

Smart follow-ups with automated payment plan offers based on behavior and risk

Dispute management built-in with resolution workflows and documentation tracking

Legal-ready escalation triggers for complex or high-value accounts

Why FinanceOps.ai?

Recover more, faster with fewer manual interventions

Maintain full FDCPA/FCRA compliance at scale

No upfront costs, pay only on successful recoveries

Deploy and see results in under 45 days

Ready to automate and scale collections? Book a demo with FinanceOps.ai

Frequently Asked Questions (FAQs)

1. How long can debt be collected?

3–6 years typically, depending on your state’s statute of limitations.

2. Can I manage collections in-house?

Yes, with the right tools like FinanceOps.ai to automate early-stage efforts and track outcomes.

3. What if a debtor disputes a debt?

Pause collection, validate the claim with documentation, and resume after resolution.

4. What’s a charge-off?

A debt written off by the creditor, typically after 180+ days, but still collectible by agencies or legal means.

5. Do I need a lawyer to collect debt?

Not always. Legal help is useful for escalated or litigated cases, but many accounts can be managed with automated tools.

6 minutes

Posted by

Arpita Mahato

Content Writer

Other Blogs

View other blogs