Introduction: Why Charge-Offs Matter

In both consumer and business finance, the ability to collect money owed is fundamental. Whether you are managing personal finances or operating a business with receivables, unpaid debts can quickly create serious challenges. One of the most critical terms to understand in this context is the concept of a charge-off.

At first glance, a charge-off might appear to be a simple accounting classification. However, for individuals, it can have long-lasting consequences on credit health. For businesses, especially those with limited resources or small margins, it represents lost revenue, reduced cash flow, and potential strain on operational efficiency.

In this guide, we will break down the charge-off definition, explain what happens when an account is charged off, and outline strategies to avoid or manage this scenario effectively.

What Is a Charge-Off?

A charge-off occurs when a creditor officially writes off a debt as uncollectible in their accounting records. This typically takes place after the borrower has failed to make payments for a prolonged period. It is a signal from the lender that they no longer expect to recover the outstanding amount through regular collection methods.

The charge-off definition can be summarized as follows:

A charge-off is a financial and accounting action taken by a lender to classify a delinquent account as a loss. It removes the debt from active receivables, but it does not eliminate the borrower’s legal responsibility to repay what is owed.

Importantly, a charge-off does not mean the debt is forgiven. The creditor may still attempt to collect the debt, either directly or by transferring it to a collection agency.

When Does a Debt Become a Charge-Off?

Lenders follow industry standards when deciding to charge off a delinquent account. The timeframe can vary depending on the type of credit.

Installment loans, such as personal loans or auto loans, are typically charged off after 180 days (or six months) of non-payment.

Revolving credit accounts, such as credit cards or business lines of credit, may be charged off after 90 to 120 days of continuous missed payments.

Once this threshold is reached, the lender removes the amount from their balance sheet and records it as a loss. The account is then reported as a credit card charge off or loan charge-off on the borrower’s credit report.

What Happens After an Account Is Charged Off?

Understanding the full impact of a charged off account requires looking at both the borrower and the creditor side.

For the Borrower

When an account is charged off:

The debt is reported to the major credit bureaus and appears on your credit report as a charge-off.

Your credit score may drop significantly, making it harder to obtain loans, credit cards, or even rental housing.

The debt may be sold to a third-party collections agency that will attempt to recover the full or partial amount.

Interest and penalties may continue to accrue, depending on the terms of the original loan agreement.

Even if the debt is eventually paid or settled, the charge-off will remain on your credit report for seven years from the original date of delinquency. It may be updated to "paid charge-off" or "settled charge-off," but the negative status still has an impact.

For the Creditor

When an account is charged off as bad debt, the business:

Classifies the debt as a financial loss and removes it from accounts receivable.

Takes a hit to its profitability and potentially its liquidity, especially if dealing with a large volume of unpaid accounts.

May incur additional expenses from hiring a collections agency or pursuing legal recovery.

Loses visibility and control over the recovery process if the debt is outsourced.

For businesses, particularly small and mid-sized enterprises, charge-offs represent more than just a one-time loss. They indicate potential issues in credit assessment, collections workflows, or customer relationship management.

Why Charge-Offs Are Detrimental to Businesses

When debts are charged off as bad debt, they affect more than just the accounting ledger. The consequences can include:

Reduced working capital, which limits the ability to invest in operations, inventory, or growth.

Strained lender-borrower relationships, as delayed follow-up on unpaid invoices can frustrate customers and reduce future engagement.

Lower investor or lender confidence, especially if charge-off rates are high and recurring.

Operational inefficiency, as finance teams spend more time on manual collection efforts that are unlikely to yield results.

While large institutions may have reserves to absorb these losses, smaller businesses often cannot afford repeated charge-offs. That is why it is essential to implement proactive credit management and intelligent collections processes.

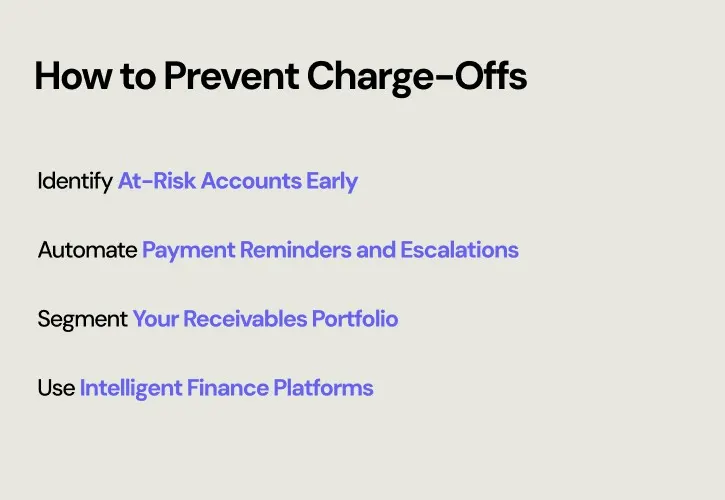

How to Prevent Charge-Offs

Preventing charge-offs requires a proactive, data-driven approach. Below are some of the most effective strategies:

1. Identify At-Risk Accounts Early

Use analytics and historical data to monitor payment behavior and flag accounts that are trending toward delinquency. Look for early warning signs such as partial payments, skipped invoices, or changes in communication patterns.

2. Automate Payment Reminders and Escalations

Manual outreach is not scalable. Leverage tools that send scheduled reminders, escalate overdue invoices, and alert your team when customer responses slow down.

3. Segment Your Receivables Portfolio

Not all customers carry the same risk. Segment your accounts based on creditworthiness, payment history, and balance size. Focus your collections efforts on high-risk or high-value accounts where the cost of recovery is justified.

4. Use Intelligent Finance Platforms

Modern software like FinanceOps.ai offers smart automation for collections. With AI-driven prioritization, automated workflows, and real-time insights, your finance team can reduce the risk of charge-offs without needing to hire additional staff.

Can You Recover From a Charge-Off?

If you are a borrower or a business owner wondering how to respond to a charge-off, here are a few important steps:

Negotiate a Settlement or Payment Plan: Creditors may accept a reduced lump sum or structured payment plan to close the account.

Request a Pay-for-Delete Agreement: In some cases, the creditor may agree to remove the charge-off from your credit report in exchange for payment, though this is not guaranteed.

Dispute Inaccurate Entries: If you believe a charge-off was reported in error, you can file a dispute with the credit bureau and provide supporting documentation.

Keep in mind that even after the seven-year credit reporting period ends, the debt may still be legally valid depending on your state’s statute of limitations.

Conclusion: Charge-Offs Are Costly, But Often Preventable

Understanding what a charge off is, and how to prevent it, is essential for anyone involved in finance, whether you're managing your own credit or leading a business with receivables.

An account charged off does not mean the debt has disappeared. It is a sign that an account has become severely delinquent, and that the creditor has stopped pursuing standard recovery methods. The financial and reputational consequences are real, both for borrowers and for lenders.

By taking early action, using automation to improve follow-up, and relying on intelligent platforms like FinanceOps.ai, finance teams can reduce the number of accounts that become charged off as bad debt. This leads to stronger cash flow, healthier customer relationships, and better long-term growth.

Looking to reduce charge-offs and optimize your collections strategy?

Book a demo today to learn how Financeops helps businesses to automate receivables, recover more revenue, and stay ahead of risk.

FAQs

1. What is a charge-off and how does it affect your credit?

A charge-off happens when a creditor writes off a debt as a loss after 90–180 days of non-payment. It stays on your credit report for up to seven years and can severely hurt your credit score.

2. What does “charged off as bad debt” mean?

It means the creditor deems the debt uncollectible and writes it off, but you still owe the money. It’s often handed to collections or legal recovery.

3. Can you pay a charged-off debt?

Yes. You’re still legally responsible. Paying or settling can reduce collection efforts and update your credit file to show a “paid” or “settled” status, though the charge-off remains for seven years.

4. How can businesses prevent charge-offs?

By monitoring delinquency signs, automating reminders, segmenting customer risk, and using AI-driven tools like FinanceOps.ai to recover debts early.

5. What’s the difference between charge-off and debt forgiveness?

A charge-off doesn’t cancel the debt, you still owe it. Debt forgiveness means the creditor fully cancels what you owe, which may have credit and tax consequences.