Blog

Effective Debt Repayment Strategies: How to Get Out of Credit Card Debt Faster with the Right Tools

May 12, 2025

Table of Contents:

Introduction: Effective Debt Repayment Strategies

What Is a Debt Repayment Strategy?

The Debt Snowball Method

The Debt Avalanche Method

Debt Repayment Strategy Formulas

Modeling in Excel or FinanceOps.ai

Debt Repayment Tools to Accelerate Your Strategy

Choosing the Best Strategy for You

Best Practices to Stay on Track

Final Thoughts

Frequently Asked Questions

Introduction: Effective Debt Repayment Strategies

Paying off credit card debt can be overwhelming, especially when you're juggling multiple bills, high interest rates, and limited monthly income. But with the right repayment strategy, you can eliminate debt faster, save thousands of interest, and build long-term financial confidence. Whether you're motivated by quick wins or cost savings, choosing between the snowball and avalanche methods can completely transform your repayment journey.

What Is a Debt Repayment Strategy?

A debt repayment strategy is a structured plan for reducing and eventually eliminating your debt in a way that aligns with your financial goals and behavioral tendencies. Instead of making random payments or only paying the minimums, you follow a method that helps you either minimize total interest paid or maintain psychological momentum by knocking out debts one by one.

The two most trusted strategies, snowball and avalanche, offer proven paths to freedom from credit card debt, and they’re widely recommended by banks, credit counselors, and financial institutions.

The Debt Snowball Method

The debt snowball method focuses on repaying debts from the smallest balance to the largest, regardless of interest rate. You make minimum payments on all your accounts but put any extra funds toward your smallest debt first. Once that debt is gone, you apply that payment amount to the next smallest balance. This process repeats until you’re debt-free.

Why it works: This method gives you quick wins and psychological momentum. Seeing small balances disappear early on helps build discipline and confidence.

Downside: Because it ignores interest rates, you might end up paying more over time.

The Debt Avalanche Method

With the debt avalanche method, you focus on interest savings. You list your debts from the highest interest rate to the lowest, regardless of balance. After making minimum payments on all accounts, you apply extra money to the debt with the highest interest rate. Once paid off, you move to the next highest rate, and so on.

Why it works: This approach saves the most money and typically helps you pay off all your debts faster, mathematically speaking.

Downside: You might not feel motivated early on, especially if your highest-interest debt is also your largest.

Debt Repayment Strategy Formulas

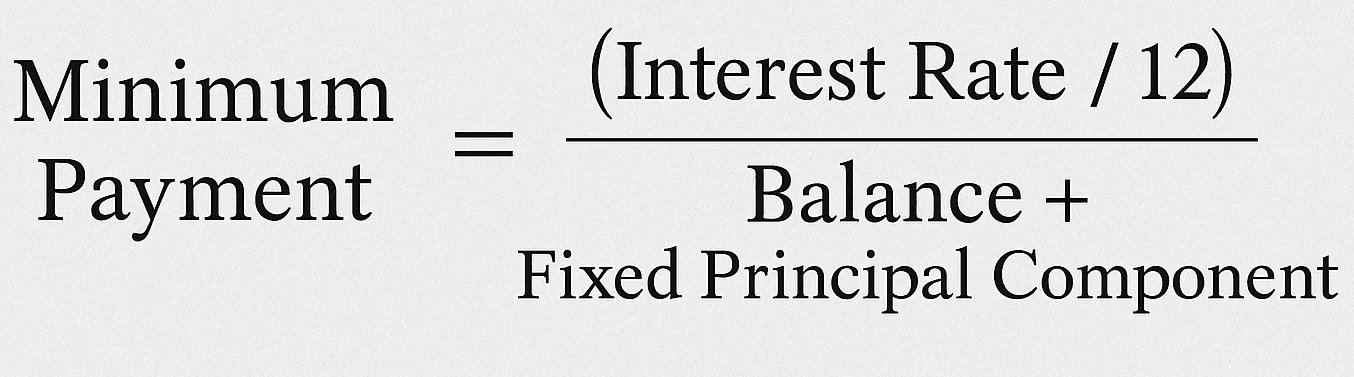

1. Minimum Monthly Payment Formula (applies to all methods)

Before customizing a snowball or avalanche strategy, calculate the minimum payment for each debt:

For example:

If your credit card balance is $5,000 at 18% APR, and the issuer requires 1% of the principal plus monthly interest:

2. Debt Snowball Method Logic

This method does not use a mathematical optimization formula, but you can represent it algorithmically:

Snowball Steps:

Sort debts by balance (ascending: smallest to largest).

Pay the minimum payment on all debts.

Allocate extra payment to the smallest balance.

Once that’s paid off, roll that entire payment (minimum + extra) into the next smallest balance.

Repeat until all debts are paid.

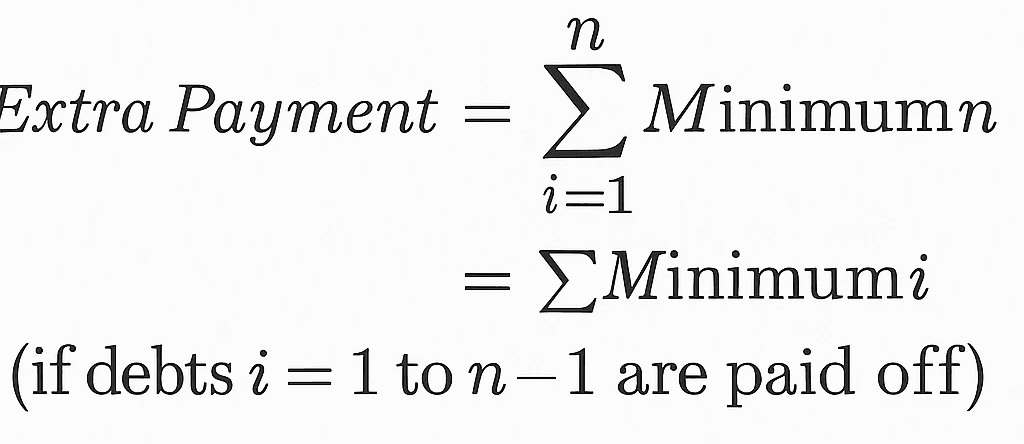

Pseudo-formula:

3. Debt Avalanche Method Formula

Like snowball, avalanche is sequential, but it’s optimized to reduce interest cost:

Avalanche Steps:

Sort debts by interest rate (descending: highest to lowest).

Pay the minimum on all debts.

Apply extra funds to the highest interest rate debt first.

Once that debt is gone, roll all payments to the next highest interest rate.

Repeat.

Pseudo-formula:

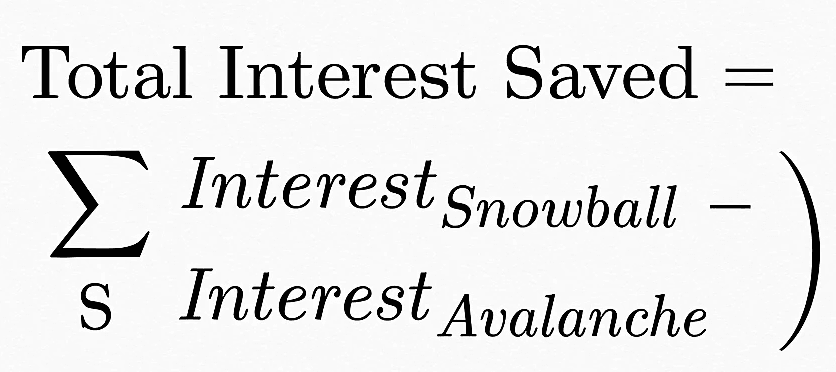

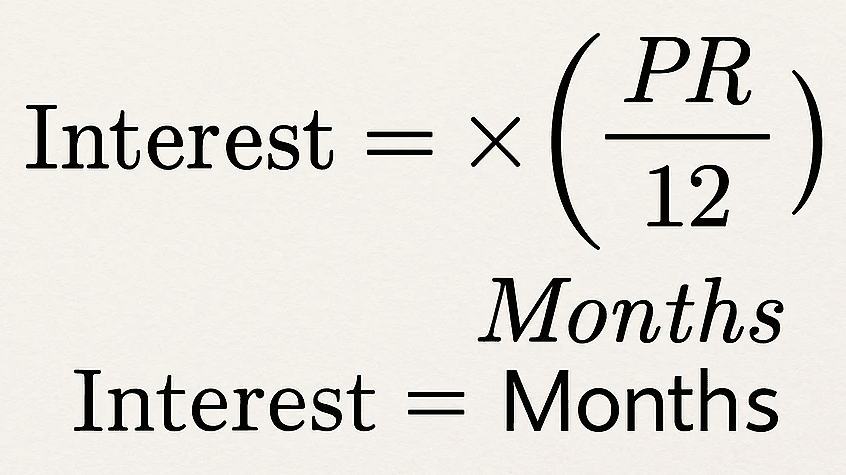

You can calculate interest per debt as:

Avalanche is mathematically superior if your goal is to minimize total interest, but it’s not always the best behavioral approach.

Modeling in Excel or FinanceOps.ai

Most online tools like FinanceOps.ai and DIY spreadsheets automate these formulas to:

Simulate amortization

Project payoff timelines

Compare total interest paid

Recommend strategy based on goals (speed vs. savings)

Debt Repayment Tools to Accelerate Your Strategy

1. Debt Repayment Calendar: Track all your payment due dates, payoff goals, and progress. A calendar offers visual accountability and prevents missed deadlines.

2. Balance Transfer Credit Card: Transfer high-interest balances to a credit card offering 0% APR for a limited time, often 12 to 18 months. This gives you a window to aggressively tackle your principal balance without accruing more interest.

3. Debt Consolidation Loan: Consolidate multiple debts into a single, fixed-rate loan, usually with a lower interest rate. This simplifies repayment and can reduce your total interest burden.

4. Automated Finance Tools: Platforms like FinanceOps.ai help you track due dates, prioritize repayments, and automate the snowball or avalanche strategy. With AI-driven insights, you’ll always know the smartest next step, especially helpful for individuals managing multiple credit cards or lines of credit.

Choosing the Best Strategy for You

There’s no one-size-fits-all strategy. If you crave momentum and small victories, the snowball method might be your best bet. If you’re focused on long-term savings, choose the avalanche method. Many people even switch strategies mid-way depending on how their financial situation evolves.

The most important part? Stick with it.

Best Practices to Stay on Track

Always pay at least the minimum to avoid penalties and protect your credit score.

Automate your payments so you’re never late.

Use a debt calculator to model different payoff timelines and compare savings.

Revisit your strategy monthly and adjust based on income changes or unexpected expenses.

Celebrate small wins to stay motivated, even if it’s just closing out a single card.

Key Takeaways:

The debt snowball method helps you stay motivated by paying off small balances first, while the avalanche method saves you the most interest by tackling high-rate debt first.

Automating your strategy with tools like FinanceOps.ai can help you stay consistent, avoid late fees, and fast-track your journey to being debt-free.

Final Thoughts

Becoming debt-free isn’t just a dream, it’s a goal you can plan for and achieve. Whether you choose the snowball or avalanche method, consistency is your most powerful tool. A lot of Collection teams are using smart strategies, lean on AI-led technology like FinanceOps.ai, and automate your financial recovery one payment at a time.

Collection teams, are you ready to take control of your debt and dispute management?

Book a demo with FinanceOps.ai to start building your personalized, AI-powered debt recovery tool today.

Frequently Asked Questions

1. Which debt repayment strategy is better: snowball or avalanche?

It depends on your priorities. Use the snowball method if you need motivational wins and the avalanche method if your goal is to save the most money on interest.

2. Can I combine the snowball and avalanche methods?

Yes. Many people start with the snowball method for motivation, then switch to the avalanche method once they feel more confident managing their payments.

3. How does FinanceOps.ai help with debt repayment?

FinanceOps.ai provides AI-driven repayment scheduling, prioritization tools, and automated tracking to help you choose the most effective strategy and stick to it effortlessly.

4. Should I use a balance transfer card or consolidation loan?

Both can help reduce interest, but balance transfer cards are best for short-term payoff (within 12–18 months), while consolidation loans offer longer repayment periods and fixed rates.

5. Is it bad to only pay the minimum on my credit cards?

Yes. Paying just the minimum prolongs your debt and increases the amount of interest you pay over time. Always pay more than the minimum when possible.

5 minutes

Posted by

Arpita Mahato

Content Writer

Other Blogs

View other blogs