Summary: With 2026 fast approaching, AI is transforming compliance in debt collection. This blog explores how AI empowers debt collectors to balance performance with regulation, enabling ethical, transparent, and fully CFPB-compliant customer interactions at every stage of the collections process.

Introduction

Imagine a small collections team managing 1,000+ low-dollar accounts while handling record keeping, calls, emails, debt validation, and customer follow-ups. With so much to juggle, even one mistake, like misreporting a debt or using an aggressive tone, can quickly escalate into compliance violations and CFPB scrutiny.

As we approach 2026, artificial intelligence is already transitioning from a futuristic concept to the backbone of regulatory compliance in today’s debt collection. Before AI, collection teams relied on manual lists, unstructured outreach, and inconsistent records, often leading to harassment, privacy breaches, and non-compliant communications that eroded consumer trust. To address these operational gaps, the U.S. government established the Consumer Financial Protection Bureau (CFPB) under the Dodd-Frank Wall Street Reform and Consumer Protection Act (2011) to set ethical communication standards and protect consumers from abusive or deceptive practices.

As regulations tighten, AI is helping collectors future-proof operations with fully compliant, ethical communication. It enables teams to meet performance goals, prioritize effectively, and maintain compliance through AI-powered monitoring, guided communication, and built-in CFPB-aligned assistance across calls, texts, and emails for improved payment recovery.

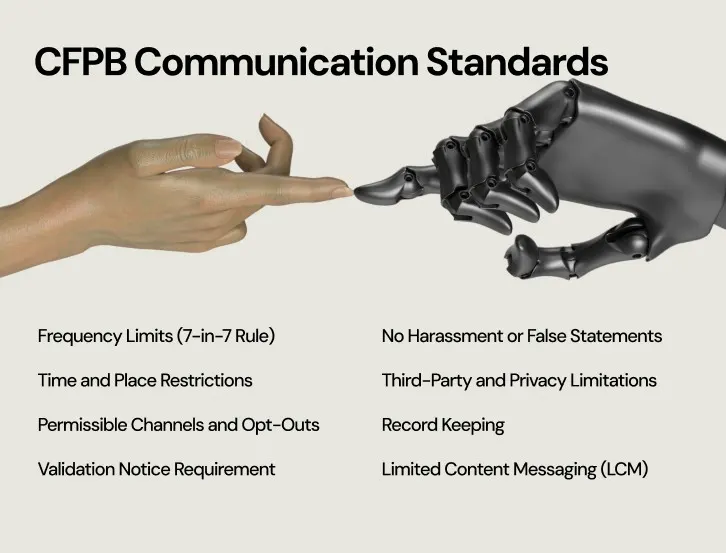

Major CFPB Communication Standards in Debt Collections

CFPB communication standards, outlined in Regulation F and the FDCPA, ensure debt collectors act ethically and protect consumer dignity. Here’s how:

Frequency Limits (7-in-7 Rule): Collectors can’t contact (telephonic attempts) a consumer more than 7 times in 7 days per debt and must wait 7 days after a conversation before reaching out again.

Time and Place Restrictions: Calls can’t be made before 8 a.m. or after 9 p.m. in the consumer’s local time zone.

Permissible Channels and Opt-Outs: Phone, email, SMS, and social media (direct messages only) are allowed, but opt-out options must be visible and respected immediately.

Validation Notice Requirement: Every initial communication must include details of the debt, the original creditor, and consumer rights to dispute.

Limited Content Messaging (LCM): Voicemails can only include basic callback info, not the purpose of the call to protect consumer privacy.

No Harassment or False Statements: Threats, intimidation, or misinformation are strictly prohibited.

Third-Party and Privacy Limitations: Collectors can only contact third parties to locate a debtor, and never to discuss debt.

Record Keeping: All communication logs must be stored for at least three years to ensure audit readiness and accountability.

Pro-Tip: With AI-driven automation, every rule, from outreach frequency to opt-out management, can be monitored, enforced, and documented automatically.

Common CFPB-Targeted Violations

Unsubstantiated debts: Collecting without valid documentation or legal backing.

Threatening legal action: Issuing or implying lawsuits without legitimate grounds.

Zombie debt collection: Attempting to recover expired or time-barred debts.

Misleading information: Misrepresenting amounts or debt status.

Harassment and privacy breaches: Using aggressive language, public disclosures, or unauthorized workplace contact.

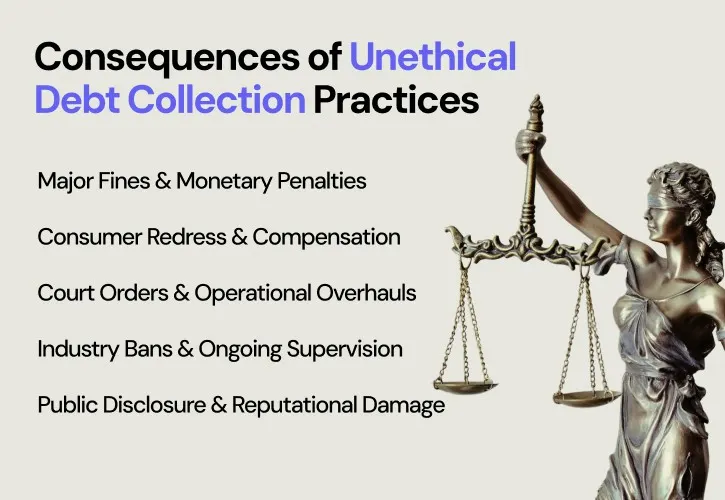

If CFPB rules are breached, there can be major consequences.

Consequences of Unethical Debt Collection Practices

1. Major fines and monetary penalties: The CFPB frequently imposes steep penalties for violating consumer protection laws, for example, fining Portfolio Recovery Associates over $24 million for collecting unverified and time-barred “zombie debts” and threatening legal action without proof. (Source).

2. Consumer redress and compensation: Collectors found guilty of misconduct must refund and compensate affected consumers, impacting finances and increasing legal scrutiny.

3. Court orders and operational overhauls: The CFPB can order non-compliant agencies to suspend operations, fix process gaps, and strengthen compliance programs, slowing business and raising administrative costs.

4. Industry bans and ongoing supervision: In severe cases, the CFPB can ban collectors or executives and impose ongoing audits, resulting in long-term oversight and reduced operational autonomy.

5. Public disclosure and reputational damage: CFPB actions are public, often damaging brand credibility, eroding consumer trust, and deterring investors and partners.

To prevent such consequences, AI ensures that all customer contact and communication are 100% compliant with CFPB rules and regulations, promoting ethical collection practices.

How AI Enables Ethical, and Compliant Debt Collection

By leveraging ML algorithms, natural language processing, and predictive analytics, AI enables ethical and compliant debt collection to manage every customer interaction without crossing compliance boundaries. Here’s how:

1. Real-Time Monitoring and Compliance Alerts

AI systems continuously monitor omnichannel communications across calls, emails, SMS, and chats, using NLP and rule-based triggers to detect potential violations in real time. Whether it’s frequency breaches, prohibited language, or unverified disclosures, the system flags anomalies before they escalate into compliance incidents.

2. Guided and Dynamic Communication Frameworks

AI-powered communication engines leverage pre-approved, compliance-validated templates aligned with CFPB Regulation F. Dynamic text generation ensures that each message is both personalized and regulation-safe, maintaining consistency, transparency, and professionalism across all touchpoints.

3. Tone, Sentiment, and Behavioral Analysis

AI detects aggressive or high-stress tones within voice and text interactions. Real-time feedback loops coach agents to maintain neutral or empathetic tones, reducing complaint rates and enhancing consumer trust while aligning with FDCPA behavioral standards.

4. Automated Audit and Recordkeeping

AI automatically indexes and archives all communications like messages, timestamps, call recordings, and disposition notes, into an immutable audit trail. This ensures full traceability and audit readiness in accordance with CFPB’s three-year record retention requirements.

5. Data Privacy, Security, and Governance

AI-driven compliance layers enforce encryption at rest and in transit, role-based access control (RBAC), and anomaly detection for unauthorized data access. These safeguards ensure adherence to FDCPA and data protection frameworks while maintaining operational transparency.

AI operationalizes compliance by automating rule enforcement in real time, making debt collection more transparent, efficient, and ethically grounded.

Note: Discover how FinanceOps uses AI automation to analyze sentiment and payment behavior in real time, ensuring every customer interaction is empathetic, data-driven, and 100% compliant with CFPB rules.

Why Compliance Matters for CFOs and Heads of Collections

For financial leaders, staying compliant is all about protecting the organization’s financial integrity and reputation. CFOs are under growing pressure to:

Minimize operational risks from human errors and outdated systems.

Maintain transparency and avoid litigation costs.

Ensure consistent, ethical communication across teams and channels.

AI is transforming collections by helping teams uphold ethical standards while improving recovery performance. By 2026, its integration into regulatory frameworks will ensure financial institutions maintain accuracy, transparency, and customer trust across every interaction.

Looking for an AI-powered solution to make your debt collection process more customer-centric, trustworthy, and fully compliant with CFPB rules?

Book a demo to discover how FinanceOps can help.

FAQs

1. What is the CFPB debt collection rule?

The CFPB Debt Collection Rule (12 CFR §1006.14a) prohibits collectors from harassing, oppressing, or abusing consumers, defining when, how, and how often they may contact debtors to ensure fair, respectful, and compliant communication.

2. What does CFPB stand for?

The CFPB (Consumer Financial Protection Bureau) is a U.S. agency established under the Dodd-Frank Act of 2010 to enforce consumer protection laws and prevent unfair or deceptive financial practices.

3. What is the “7-in-7” rule for debt collections?

Under CFPB Regulation F, collectors may not make more than seven calls in seven days per debt and must wait seven days after a conversation before calling again, preventing excessive contact.

4. How is AI used in debt collection to stay compliant with CFPB rules?

AI compliance tools monitor communications, detect violations, and guide agents in real time, ensuring every call, message, and email aligns with CFPB standards and ethical practices.