Why Does Medical Debt Persist Despite Health Insurance?

A recent study by RFF Polling showed that 90% of Americans have access to health insurance, but medical debt continues to plague millions. According to Gallup, 12% of adults, or around 3 million people, borrowed over $74 billion in 2024 to cover medical expenses. This statistic clearly signals a gap in healthcare coverage and understanding. (Source1) (Source2)

Why is this happening?

The issue stems from unexpected medical costs, even for insured patients. After treatment, patients are often shocked to find that their insurance only covers part of the bill, or excludes certain procedures. This leaves them with high out-of-pocket expenses, forcing many to borrow money, especially those with chronic conditions requiring ongoing care.For example, patients with cancer, diabetes, thalassemia, or those needing pregnancy or gender-affirming care face significant costs. In fact, 41% of U.S. adults have borrowed from family or friends or taken out loans to pay medical bills.

The SIPP survey estimates U.S. medical debt at $220 billion, with 14 million people owing over $1,000, and 3 million owing more than $10,000. People with disabilities, poor health, or lower incomes are most likely to incur significant medical debt.

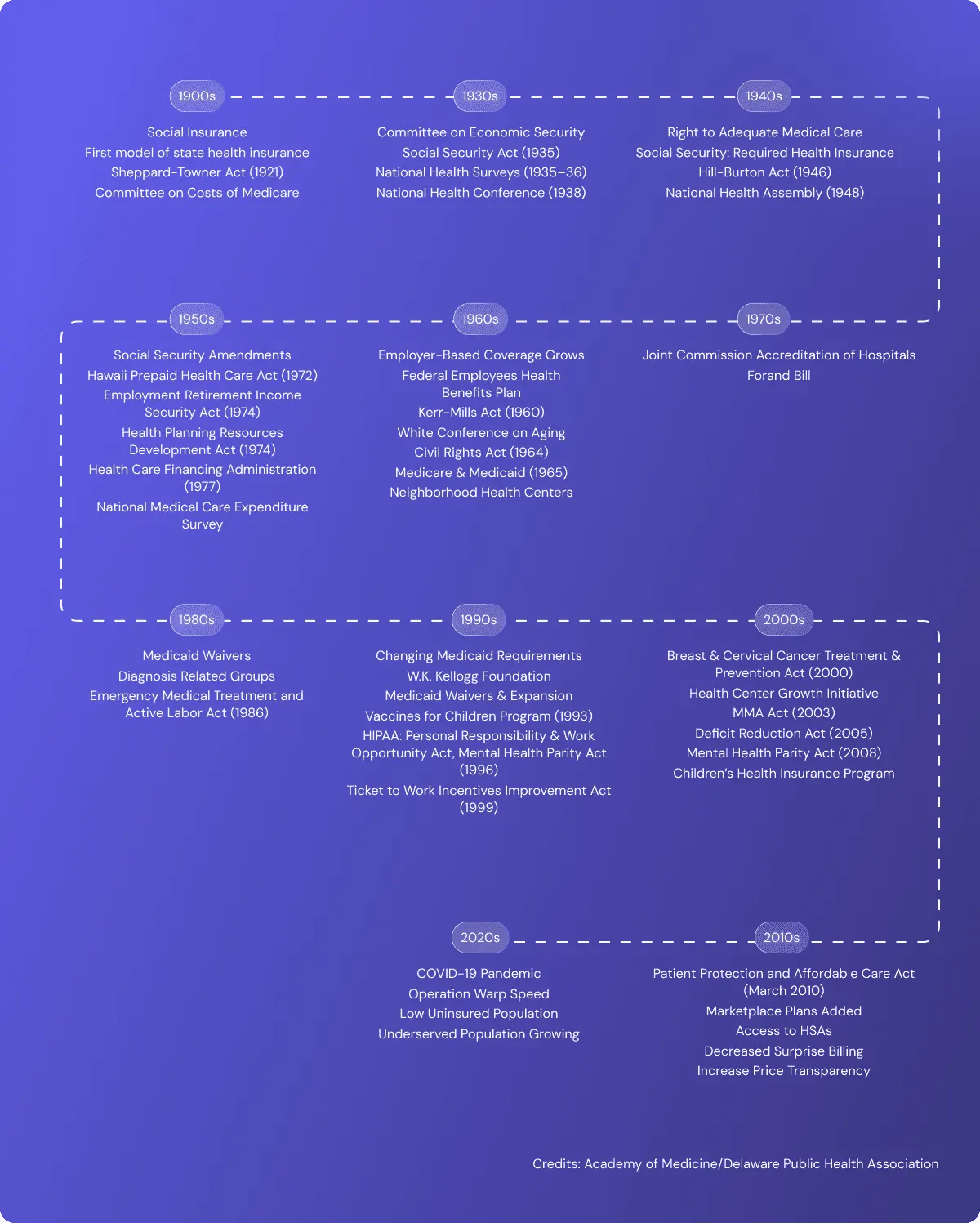

The History of Healthcare Costs: How Did We Get Here?

U.S. healthcare costs have surged over the years due to advancements in medical technology, rising service costs, and changing policies. The journey began in the early 20th century with Teddy Roosevelt's endorsement of health insurance, but it was the 1920s Baylor Hospital model that evolved into Blue Cross plans. Despite efforts during the Great Depression and post-war era for universal healthcare, it wasn’t until the 1960s that Medicare and Medicaid expanded access for the elderly and low-income populations. However, rising premiums, out-of-pocket expenses, and underinsurance continue to affect millions of Americans.

The 2010 Affordable Care Act (ACA) aimed to reduce the number of uninsured Americans and make healthcare more affordable through expanded Medicaid and insurance marketplaces. While the ACA increased coverage, it did not address rising healthcare costs. Today, even insured Americans face crippling medical debt, revealing systemic issues. Despite reforms, escalating premiums, out-of-pocket costs, and coverage gaps remain, highlighting the urgent need for further policy changes to make healthcare more affordable and protect Americans from debt. (Source)

The Shift in Healthcare: Why Is This Happening?

The healthcare system has undergone significant shifts in recent years, largely due to the COVID-19 pandemic. The challenges from 2020 to 2021 exposed vulnerabilities within the system, such as supply chain disruptions, worker shortages, and rising costs, affecting both providers and patients. However, the pandemic also accelerated tele-medicine adoption and AI-driven automated solutions, spurring innovation in care delivery models and improving patient access to services.

Looking ahead, while healthcare systems are recovering, the financial strain on providers and patients remains, and maybe AI in healthcare is something that can help.

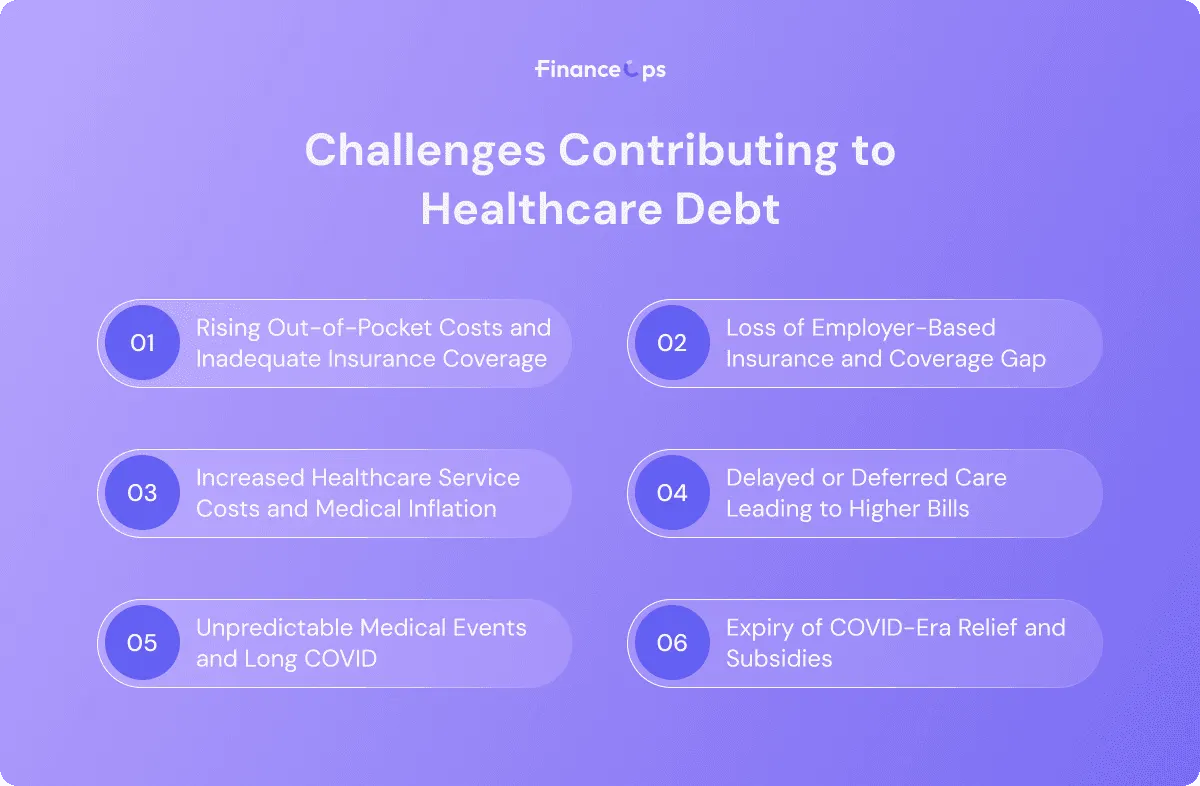

Challenges Contributing to Healthcare Debt:

Rising Out-of-Pocket Costs and Inadequate Insurance Coverage

Post pandemic, even with insurance, high deductibles, co-pays, and coinsurance leave many individuals paying large portions of their medical bills on their own. Rising insurance premiums make basic coverage hard to afford, and "under insurance" leaves people with big bills because their current insurance doesn’t cover everything.

Loss of Employer-Based Insurance and Coverage Gaps

During the pandemic, millions lost their jobs and, consequently, their employer-provided health coverage. Many have struggled to regain adequate coverage, with some still facing insurance gaps, especially as the economy recovers. These gaps have left them vulnerable to unexpected medical costs and growing debt.

Increased Healthcare Service Costs and Medical Inflation

Post-Covid, medical costs for services, treatments, and prescription drugs have risen sharply, outpacing both wage growth and inflation. Hospital care, specialized treatments, and essential medications have become significantly more expensive, adding to the financial strain on individuals and families already facing other economic challenges.

Delayed or Deferred Care Leading to Higher Bills

Many people postponed or skipped medical care during the pandemic, causing health issues to worsen. Now, they need more expensive treatments to address problems that could have been managed earlier. This delayed care has led to higher medical bills, especially for those with chronic conditions.

Unpredictable Medical Events and Long COVID

Unexpected medical events, injuries, or illnesses, including complications from Long COVID, have led to unplanned high medical costs. Even individuals who once believed they were adequately insured have found themselves financially overwhelmed by ongoing treatment costs.

Expiry of COVID-Era Relief and Subsidies

During the pandemic, many received extra subsidies and better access to Medicaid and insurance. With these relief measures ending and the Medicaid recent crisis, more people are now facing higher healthcare costs, leading to more medical debt.

These challenges have created credit instability in the healthcare system, which impacts both providers and patients.

How Can Patients Avoid Medical Debt

Prioritize Preventive Care: Invest in preventive care to reduce the risk of chronic diseases, which can lead to expensive treatments and long-term costs.

Choose the Right Health Insurance: Select a plan that covers hospital stays, prescriptions, and specialized care. Understand your plan’s details, including deductibles, co-pays, and out-of-network costs, to avoid surprises.

Understand Your Coverage: Read your policy to know what’s covered and any exclusions. Understand out-of-pocket maximums to prevent unexpected medical bills.

Choose In-Network Providers: In-network providers are usually cheaper. Always verify your provider is in-network to reduce costs and maximize coverage.

Review and Negotiate Your Bills: Check medical bills for errors and negotiate with providers for discounts or payment plans, especially if you’re facing financial hardship.

Explore Financial Assistance Programs: Ask about financial assistance or sliding scale fees based on your income if you’re struggling with medical bills.

Open a Health Savings Account (HSA): For high-deductible plans, open an HSA to save tax-free money for medical expenses and reduce out-of-pocket spending.

Consider Debt Management Plans: Consolidate medical debts or use a debt management plan to simplify repayments and reduce interest rates.

Don’t Ignore Medical Bills: Ignoring bills leads to late fees, increased debt, and credit damage. Communicate early with providers to discuss payment options or plans.

What to Look for When Choosing Health Insurance

1. Comprehensive Coverage

When choosing a health insurance plan, ensure it covers more than just basic care. A comprehensive plan should include hospital stays, surgeries, doctor visits, chronic condition management, mental health services, and rehabilitation, along with specialized care like cancer treatment, physical therapy, and post-acute care. This helps minimize unexpected out-of-pocket costs for serious health issues.

2. The Metal Categories: Bronze, Silver, Gold, and Platinum

Health insurance plans are categorized into metal tiers, Bronze, Silver, Gold, and Platinum, based on how costs are shared. Bronze plans have lower premiums but higher out-of-pocket costs, while Platinum plans have higher premiums and lower costs. Silver and Gold plans fall in between. The right choice depends on your healthcare needs and whether you prefer lower premiums with higher out-of-pocket costs or vice versa.

3. Plan and Network Types: HMO, PPO, POS, and EPO

Health insurance plans come in different types: Health Maintenance Organizations (HMOs), Preferred Provider Organizations (PPOs), Point of Service (POS), and Exclusive Provider Organizations (EPOs). HMOs require staying within a specific network and getting referrals from a primary care physician. PPOs offer more flexibility with out-of-network care but have higher premiums. POS and EPO plans combine elements of both, with EPOs having more restrictive provider options. Consider your need for flexibility when choosing the best plan.

4. Rehabilitation and Post-Acute Care Limits

Many health insurance plans impose limits on how much coverage is provided for rehabilitation services such as physical therapy, skilled nursing, and post-acute care. These limits can be financially devastating, particularly if you need extensive rehabilitation after major surgery or illness. Be sure to check the specific coverage for rehabilitation and post-acute care, including any limits on the number of days or sessions covered.

5. Step Therapy ("Fail First") Rules

Step therapy (or ‘fail first’ protocols) requires patients to try lower-cost treatments before covering more expensive options. While it helps control costs, it can delay access to necessary treatments, especially for chronic or complex conditions. If your plan includes step therapy, understand how it affects your care access and familiarize yourself with the appeals process to expedite treatment if necessary.

6. Lifetime/Annual Maximum Loopholes

While the Affordable Care Act (ACA) prohibits overall lifetime and annual limits on essential health benefits, some “excepted benefits” such as dental, vision, or short-term insurance still have strict caps. These limits can leave you with significant out-of-pocket expenses for services that fall outside the main coverage. Review any maximums or exclusions for these types of benefits to ensure you’re fully covered without unexpected financial strain.

7. Prescription Drug Coverage

Prescription drug coverage is essential, particularly if you take ongoing medications. Check the plan’s formulary to ensure your medications are covered, including both generics and brand-name drugs. It's important to evaluate the co-pays for your medications and consider whether the plan offers mail-order prescriptions, which can provide convenience and cost savings, especially for long-term treatments.

By focusing on preventive care, understanding insurance details, and negotiating bills, patients can manage healthcare costs and avoid debt. For healthcare providers, offering transparent communication, flexible payment options, and empathetic customer service is crucial in reducing patient financial strain.

Book a demo with Financeops to tranform collections using AI-driven automation.