Introduction: Why Accounting Accuracy Matters for Financial Auditing?

Accounting has been around for thousands of years, long before spreadsheets, software, or even coins. It has evolved alongside human civilization, growing more complex as societies, economies, and businesses developed. From the clay tablets of Mesopotamia to Luca Pacioli’s double-entry system in 1494, every advancement in accounting has been built on the same foundation: accuracy. Without accuracy, records are meaningless, audits are unreliable, and financial decisions become guesswork. History reminds us that precision in accounting is what gives businesses credibility, stability, and the ability to grow.

Today, CFOs face challenges Pacioli could never have imagined, billions of digital transactions, sprawling AR, and real-time reporting demands. Inaccuracy is costly: a single balance sheet error can erode investor confidence, strain liquidity, and invite regulatory scrutiny. Manual reconciliation can’t keep up, but AI can. By detecting anomalies, automating reconciliations, and learning from past patterns, AI makes accuracy scalable, audits seamless, and growth sustainable.

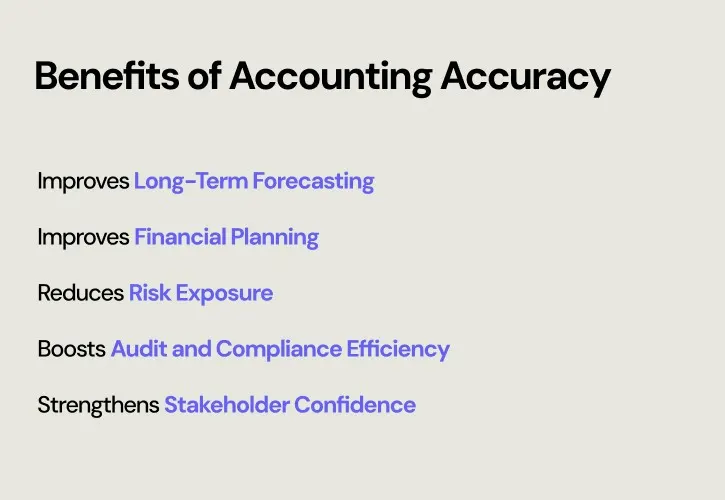

What Are the Benefits of Accounting Accuracy in Financial Reporting?

Accounting accuracy is the degree to which a company’s financial statements truly reflect its financial position. Every transaction, from revenues to expenses to AR accounts, must be recorded correctly, categorized properly, and free from errors or misstatements. Getting it right delivers far more than clean books. Here’s how it transforms your organization:

1. Improves Forecasting and Financial Planning

Accurate numbers today enable smarter decisions tomorrow. When AR accounts and other financial data are reconciled correctly, leaders gain a true picture of performance, allowing confident cash flow forecasting, capital allocation, and growth planning.

2. Reduces Risk Exposure

Unreconciled AR accounts create blind spots that can escalate into costly problems. Maintaining accurate books flags early warning signs, strengthens liquidity, and minimizes compliance risks before they become liabilities.

3. Boosts Audit and Compliance Efficiency

Late errors drain time and resources. High accounting accuracy, especially when supported by AI-powered reconciliation, minimizes manual errors, automates checks, and ensures compliance. The result: faster, smoother, and less expensive audits.

4. Strengthens Stakeholder Confidence

Trust is currency in business. Precise, reliable financials build confidence among investors, lenders, and regulators. Conversely, inconsistent reporting or misaligned AR accounts can erode credibility and limit strategic opportunities.

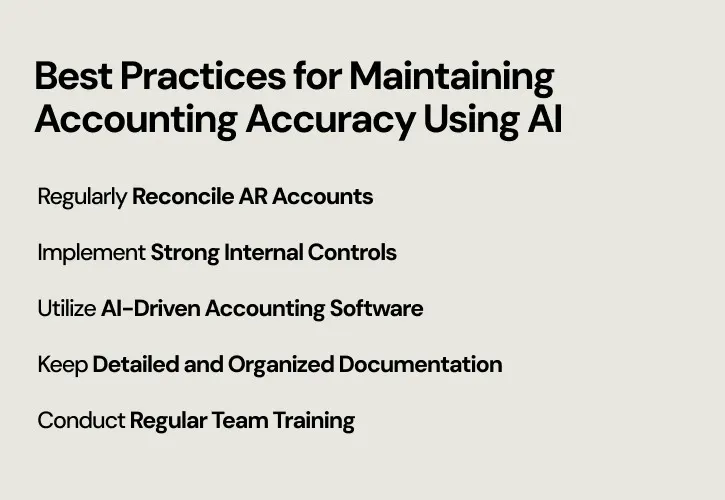

Best Practices for Maintaining Accounting Accuracy Using AI

1. Regularly Reconcile AR Accounts

The most effective way to maintain accounting accuracy is to consistently reconcile AR accounts. This ensures invoices, payments, and bank statements align with your records, giving you a real-time view of receivables and cash flow while identifying delinquent accounts early. AI detects anomalies, flags mismatched transactions, and even suggests corrective entries automatically.

2. Implement Strong Internal Controls

AI is powerful, but guardrails are essential. Internal controls provide the checks and balances that prevent fraud, errors, and regulatory lapses. CFOs should implement clear SOPs, approval workflows, and access controls within finance teams. Pairing these with AI-powered monitoring strengthens accounting accuracy.

3. Utilize AI-Driven Accounting Software

Modern AI-driven platforms help with automated reconciliation, predictive cash flow analysis, and anomaly detection, reducing manual work and eliminating human error. AI also analyzes historical data to recommend optimal collection strategies and payment terms, strengthening AR accounts management, improving cash flow forecasting, and helping you consistently reconcile AR accounts.

4. Keep Detailed and Organized Documentation

Invoices, receipts, contracts, and payment confirmations form the backbone of accounting accuracy. But they’re only valuable if accessible and traceable. AI-powered document management systems automatically categorize, tag, and link supporting documents to AR accounts, creating a seamless audit trail. This simplifies compliance, speeds up audits, and helps finance teams quickly retrieve records.

5. Conduct Regular Team Training

Even the most advanced AI tools need skilled people behind them. Regular training helps finance teams understand traditional principles and leverage accounting accuracy using AI effectively. From reconciling AR accounts to managing AI-flagged exceptions, continuous learning builds confidence, reduces errors, and fosters a culture of accountability.

The Most Common Accounting Accuracy Accidents

The most common accounting accuracy errors occur during bookkeeping, reconciliation, and financial reporting. These mistakes distort financial statements and make it harder to accurately reconcile AR accounts. Below are the most frequent errors affecting accounting accuracy:

1. Error of Omission

A transaction isn’t recorded at all (e.g., a customer payment never entered into AR).

In AR accounts, this often shows up as invoices marked unpaid even though payment was received, throwing off cash flow.

2. Error of Commission

The transaction is recorded but in the wrong place (e.g., applying a payment to the wrong customer account).

Leads to AR aging reports that don’t reflect reality, making it difficult to reconcile AR accounts.

3. Error of Principle

Misclassifying transactions (e.g., recording a long-term asset purchase as an expense).

Breaks compliance with accounting standards and distorts profitability calculations.

4. Transposition Errors

Entering $5321 as $5231.

Small but impactful, these mistakes often appear during AR reconciliation, causing mismatches between invoices and payments.

5. Duplication Errors

Recording the same invoice or payment twice.

Common in AR accounts when multiple team members manually log transactions.

6. Error of Original Entry

Logging the wrong amount from the start (e.g., recording $100 instead of $1,000).

Every subsequent AR report is based on faulty data, making reconciliations unreliable.

7. Entry Reversal Errors

Recording a debit as a credit or vice versa.

In AR, this can make accounts look collected when they’re actually outstanding.

8. Compensating Errors

Two mistakes cancel each other out (e.g., overstating AR and also overstating revenue).

The book's balance, but accounting accuracy is compromised.

9. Subsidiary Ledger Errors

AR subsidiary ledgers don’t match the AR control account.

Causes delays in closing books and frustrates reconciliation efforts.

10. Data Entry & Rounding Errors

Incorrect decimal placement or inconsistent rounding.

Individually small but damaging to overall accounting accuracy when reconciling AR balances.

Key Takeaways

1. Accounting Accuracy is Non-Negotiable: Accurate financial data underpins every audit, forecast, and decision. Without accounting accuracy, AR accounts can quickly spiral into errors that distort cash flow and weaken trust with auditors, investors, and regulators.

2. Reconciling AR Accounts Is Critical: Regularly reconciling AR accounts ensures your reported revenues actually match what’s collected. Missed reconciliations create discrepancies that delay reporting and inflate risk, problems AI can now eliminate with automation.

3. AI Makes Accuracy Scalable: Manual processes can’t keep up with billions of digital transactions. AI detects anomalies, reconciles AR accounts in real time, and learns from past patterns to continuously improve accounting accuracy. With AI, CFOs can trust their numbers, streamline audits, and forecast with confidence.

Ready to take control of your AR accounts and scale accounting accuracy with AI?

Book a demo today to learn how Financeops helps finance teams to automate reconciliations, eliminate errors, and build audit-ready books, without any time-consuming manual headaches.