Blog Summary: This blog explains what happens when debt collectors or debt collector attorneys ignore a debt validation letter and fail to prove a debt is legitimate before moving it further into debt to collections. It outlines your rights under the FDCPA, what collectors must validate, how to dispute unverified debts on your credit report, and how to request details on how an account was “verified.” It also covers the legal and financial risks collectors face when they ignore a debt validation letter request, why proper validation protects both consumers and organizations.

What If a Collector Ignores Your Debt Validation Letter?

When a debtor sends a debt validation letter, they’re exercising their federal right to request proof that a debt is legitimate before it moves further into debt to collections. This step protects consumers from errors, identity theft, and aggressive debt collectors. But what if the collector, or a debt collector attorney, does not respond or fails to provide proper validation? Here’s what you need to know.

Understanding Your Rights and How to Respond

When you’re contacted by debt collectors for payment recovery, uncertainty around the debt’s legitimacy can create anxiety. That’s why federal law gives you the right to send a debt validation letter request and force the collector to prove the debt before any collection can continue. If they reach out without proper verification, they’re violating your rights.

Are Debt Collectors Legally Required to Validate a Debt?

Yes. Under the FDCPA, debt collectors and debt collector attorneys must validate the debt if the consumer sends a written debt validation letter request within 30 days of first contact. Upon receiving a written debt validation request, the collector must:

Provide documentation that the debt is real and accurate.

Disclose the name and address of the original creditor.

Verify the exact amount owed, including any interest or fees.

Show proof of their authority to collect the debt.

Confirm that the debt is still within the applicable statute of limitations.

During this period, all collection activity must stop, including calls, letters, and credit reporting.

What If the Collector Fails to Respond to the Verification Letter?

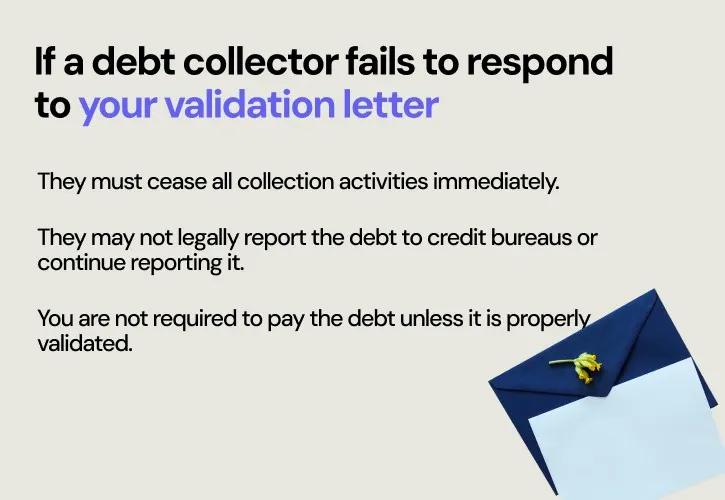

If a debt collector fails to respond to your validation letter, or cannot provide sufficient evidence, the consequences are clear:

They must cease all collection activities immediately.

They may not legally report the debt to credit bureaus or continue reporting it.

You are not required to pay the debt unless it is properly validated.

Can An Unvalidated Collection Account Be Removed from Your Credit Report?

Yes. If a debt collector reports a debt that has not been properly validated, it can be challenged, and removed, through the dispute process. Here's how:

File a dispute with each of the major credit bureaus (Equifax, Experian, and TransUnion).

Include a copy of your debt validation letter and proof of mailing (e.g., certified mail receipt).

Clearly state that the collector failed to validate the debt as required under the FDCPA.

Ask for the removal of the collection account if the collector cannot provide documentation.

Under the Fair Credit Reporting Act (FCRA), credit bureaus must investigate disputes. If the collector cannot verify the debt, the bureau must remove it from your file. This can significantly improve your credit profile and protect your borrowing capacity.

Follow-Up Strategy: Ask “How Was This Account Verified?”

Sometimes, even after your dispute, a collection account remains on your credit report. In this case, take the next step by asking the credit bureau:

"How was this debt verified?"

You have the right to request details of the verification process. Ask the bureau to provide:

A description or copy of the documents used to verify the debt.

Evidence of communication from the collector.

Proof that the collector has met their burden of validation.

If they cannot respond adequately or the response is vague, you may demand that the entry be removed.

Next Steps to Protect Yourself and Uphold Your Rights

Debt validation is a key tool in ensuring transparency and fairness in financial obligations. To protect yourself throughout the process:

Document everything: Keep copies of all letters, communications, and receipts.

Use certified mail: Always send requests via certified mail with a return receipt.

Monitor your credit report: Check regularly for any unvalidated entries.

File complaints: If your rights are violated, report the issue to the:

Consumer Financial Protection Bureau (CFPB)

Your state attorney general’s office

Consult a legal professional: If a collector continues to pursue you without validation or threatens legal action, seek qualified legal assistance.

The High Cost of Ignoring Debt Validation Requests

Failing to respond to a proper debt validation request doesn’t just breach the Fair Debt Collection Practices Act (FDCPA), it exposes organizations to lawsuits, regulatory fines, and reputational harm. Legally, collectors must cease all collection efforts until the debt is properly validated. Ignoring this mandate can lead to consumer litigation and enforcement actions from the CFPB or state authorities.

Financially, the impact is just as severe. Traditional recovery rates are already low, 20–50% for in-house, 12–20% for outsourced efforts, and drop further when debts can’t be validated. Legal costs, compliance failures, and negative ROI per agent further strain performance. Every unvalidated debt wastes time, increases risk, and erodes trust.

A Smarter, More Human Approach with FinanceOps

Let’s face it, traditional debt collection can feel disconnected, slow, and full of friction. Requests get lost in the shuffle, follow-ups fall through the cracks, and outdated systems make it hard to stay compliant. That’s where FinanceOps comes in.

FinanceOps brings everything together with seamless communication across SMS, phone calls, and emails, so you can reach people how they prefer to be reached, and keep every step of the process visible and accountable. Whether it’s sending a validation notice or following up on a dispute, everything is tracked, compliant, and right where you need it.

No more chasing paperwork or wondering if someone received your letter. With FinanceOps, you get a clear, automated workflow that protects your business and helps the customers to settle their debt faster.

**The outcome?

**Better engagement, higher recovery rates (up to 78%), and a collections strategy that’s built on trust, transparency, and results.

At FinanceOps, we help you collect, and connect.

Book a free demo today and future-proof your collections with FinanceOps.

FAQs

1. Do collectors have to prove the debt if asked?

Yes. Debt collectors must provide full validation if you send a debt validation letter within 30 days.

2. What if they don’t respond?

They must stop collecting and reporting. Continuing without validation violates federal law.

3. Can unvalidated debts be removed from credit reports?

Yes. File a dispute and attach your validation request.

4. What if the debt still appears after dispute?

Ask the bureau, “How was this debt verified?” If they can’t prove it, request removal.

5. How does FinanceOps help?

FinanceOps automates debt validation, dispute tracking, and compliance, reducing legal risk and improving outcomes.