A collection dispute letter is not just a document. In the hands of an AR manager who understands what triggers disputes and how to respond to them, it is the difference between a resolved account and a regulatory complaint that costs more than the original balance.

TL;DR

A collection dispute letter is a formal written notice that stops collections activity and requires a debt collector to validate the debt within 30 days under FDCPA. Sending one without understanding what triggers it is how disputes escalate into compliance events.

AR managers and collections teams need to understand collection dispute letters from both sides. From the debtor's side to understand what triggers them. From the creditor's side to understand how to respond to them compliantly and how to prevent them from being issued in the first place.

FinanceOps Agentic AI reduces dispute rates structurally by resolving the most common dispute triggers, including tone mismatch, unclear invoicing, and missed early-stage engagement, before a dispute letter is ever written.

What Is a Collection Dispute Letter

A collection dispute letter is a formal written communication sent by a debtor to a collection agency or creditor challenging the validity, accuracy, or ownership of a debt. Under the Fair Debt Collection Practices Act, also known as FDCPA, receiving a written dispute within 30 days of first contact triggers a mandatory obligation on the collector to cease collection activity and verify the debt before proceeding.

For AR managers and collections teams, understanding what a collection dispute letter is matters from two directions simultaneously.

First, you need to understand it as a potential incoming document that requires a specific, compliant response within a legally governed timeframe. A dispute letter received and mishandled is not just a lost account. It is a CFPB complaint, a potential FDCPA violation, and a regulatory audit waiting to happen.

Second, you need to understand it as a signal. Every collection dispute letter your organization receives is a retrospective indicator that something in the outreach, invoicing, or communication process broke down before the dispute was filed. An AR team that understands why disputes happen is an AR team that can structurally prevent them from happening at the stage where prevention is still possible. Both perspectives matter. This guide covers both.

What Triggers a Collection Dispute Letter in AR Operations

Before an AR team can effectively prevent or respond to collection disputes, it needs to understand the specific conditions that cause debtors to reach for the dispute letter mechanism.

Incorrect invoice amount: The most common trigger in B2B AR. A customer receives an invoice with a discrepancy, contacts the AR team, and receives no timely resolution. After multiple ignored or delayed responses, the customer files a formal dispute. The dispute was preventable at the communication stage. The invoice error was the cause. The slow response was the accelerant.

Incorrect creditor or account identification: A debtor receives collection outreach but does not recognize the creditor name, the account number, or the balance claimed. This frequently happens when debt is sold to a third-party collector or when the original creditor's name differs from the brand name the debtor recognizes. Any outreach that cannot be immediately associated with a recognized obligation will trigger a dispute.

Tone mismatch in collections outreach: A customer experiencing a short-term cash flow gap receives firm, escalatory collections language before any attempt at payment restructuring has been made. The customer disputes the debt not because they don't owe it but because the outreach approach felt aggressive or inaccurate relative to their situation. These are the most preventable disputes in any collections portfolio.

Settled or already-paid debts appearing in collections: A customer who paid a balance receives a collection notice for the same balance because reconciliation failed to update the collections system in time. From the debtor's perspective, this looks like fraud or a systemic error. From the creditor's perspective, it is a reconciliation failure. Either way, a dispute letter arrives.

Debt outside the statute of limitations: Debts beyond the applicable statute of limitations in the debtor's state may generate dispute letters when debtors are informed of their rights. AR teams that do not track portfolio aging against state-specific statute of limitations timelines regularly encounter this trigger.

Communication channel mismatch: A debtor receives collections outreach through a channel they did not consent to or in a language they cannot fully understand. The outreach does not produce a payment. It produces a dispute because the debtor experienced the contact as procedurally improper.

Understanding these triggers matters because the majority of them occur before any dispute letter is written. That means the majority of dispute letters your AR team receives are preventable at the outreach and invoicing stage, not at the response stage.

The FDCPA Framework Every AR Team Needs to Understand

The Fair Debt Collection Practices Act is the federal statute that governs how debts may be collected in the United States. For AR managers and collections teams, FDCPA creates specific obligations and specific timelines that apply the moment a consumer invokes their right to dispute.

The 30-day dispute window: Under FDCPA Section 809(b), a consumer has 30 days from the date of the first written communication from a collector to dispute the debt in writing. If the consumer sends a written dispute within that window, the collector must cease collection activity until the debt is verified and the verification is mailed to the consumer.

The validation requirement: Upon receiving a written dispute, the collector is required to obtain verification of the debt from the original creditor and mail that verification to the consumer. The verification must include the name and address of the original creditor if different from the current creditor.

Cease and desist obligations: If a consumer requests in writing that a collector stop communicating, the collector must cease communication subject to limited exceptions, including notifying the consumer that collection efforts are being terminated or that a specific remedy such as a lawsuit will be pursued.

The FCC Revoke All enforcement, effective April 2026: Consent revocation now applies across all lines of business simultaneously. A consumer who revokes consent in any channel has that revocation applied across every channel the collector operates. Collections teams that track consent manually and do not have automated cross-channel consent management are carrying regulatory exposure that scales with every account they work.

State-specific requirements: FDCPA sets the federal floor. States including California, New York, and Texas have additional consumer protection requirements that overlap with and in some cases exceed FDCPA. AR teams operating across multiple states need compliance governance that is aware of and enforces state-specific requirements at the individual account level.

The FDCPA framework is not primarily a burden. It is a structure. AR teams that encode FDCPA requirements structurally into their collections workflow, rather than managing them as manual checklists, produce fewer disputes because they produce fewer compliance errors at the contact stage.

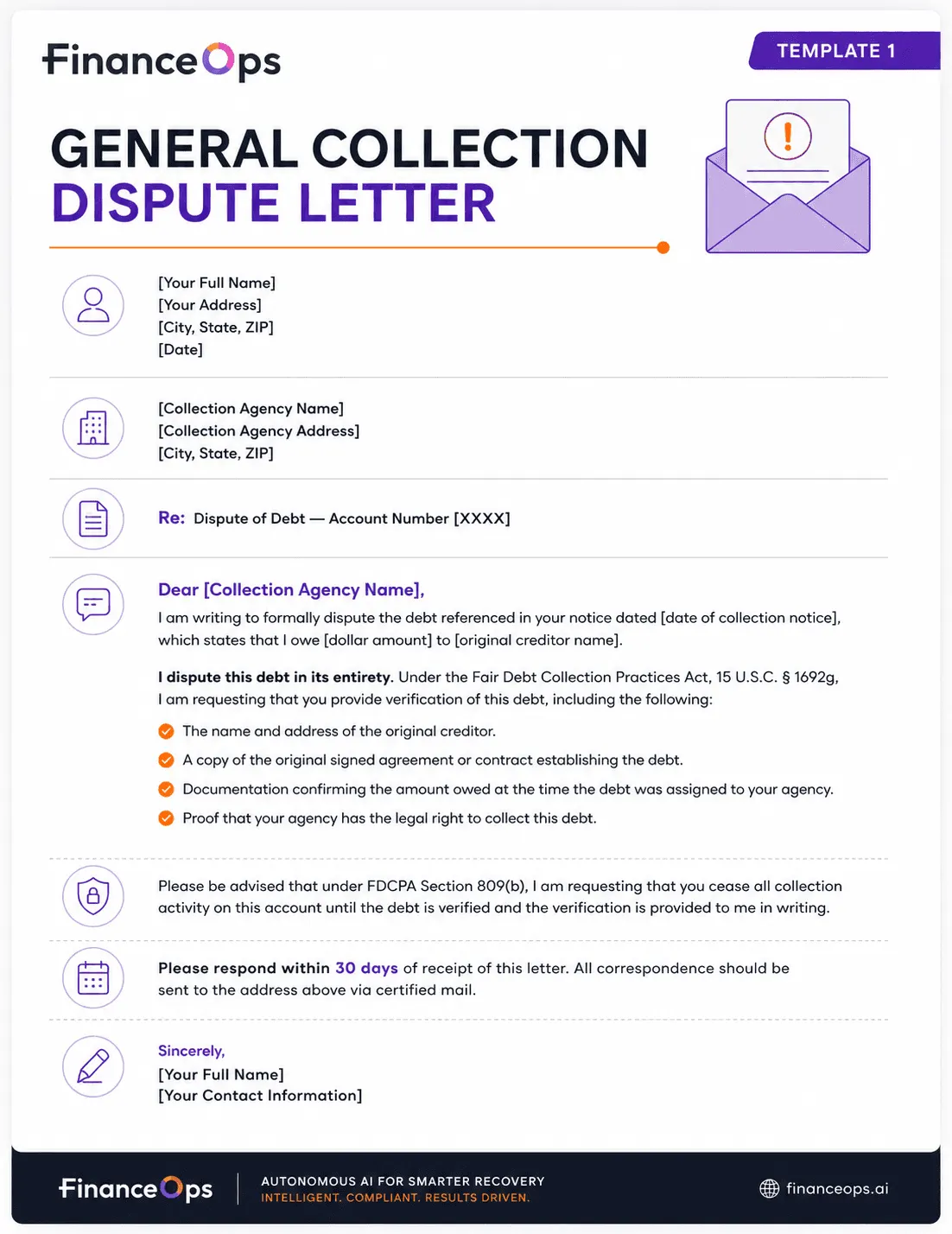

How to Write a Collection Dispute Letter: Step-by-Step

This section covers collection dispute letters from the debtor's perspective, because AR managers need to understand exactly what a compliant dispute letter contains in order to recognize, process, and respond to one correctly when it arrives.

Step 1: Send the dispute within 30 days of first contact: The FDCPA dispute window is 30 days from the first written communication from the collector. A dispute sent after that window is still valid but loses the automatic cease-collection-activity protection. Timeliness matters.

Step 2: Send the dispute in writing via certified mail: Verbal disputes do not carry the same legal weight under FDCPA. A written dispute sent via certified mail with return receipt creates a dated, verifiable record that the dispute was received. This protects the debtor and is the standard that any AR team should expect to receive and verify.

Step 3: Include complete identification information: The dispute letter must include the debtor's full name, current mailing address, account number as it appears on the collection notice, and the name of the original creditor if known. Incomplete identification creates ambiguity that delays resolution.

Step 4: State the dispute clearly and specifically: The letter must state explicitly that the debt is being disputed and should identify the specific reason. Vague disputes, "I don't think I owe this," are harder to process than specific disputes, "The balance shown of $4,200 does not reflect a partial payment of $1,800 made on March 15, 2026." Specificity accelerates resolution.

Step 5: Request debt validation: The dispute letter should formally request that the collector provide verification of the debt including the name and address of the original creditor, the amount owed at the time of assignment, and documentation showing the collector's right to collect.

Step 6: Attach supporting documentation: Copies of payment receipts, prior correspondence, settlement agreements, or any documentation that supports the dispute claim should be included. Originals should be retained. Only copies should be sent.

Step 7: State a response deadline: The dispute letter should specify a reasonable response window, typically 30 days, within which the debtor expects either validation of the debt or confirmation that collection activity has been suspended.

Step 8: Keep a complete copy: Every component of the dispute letter and all attachments should be copied and retained along with the certified mail receipt. This record is the debtor's protection if the collector fails to comply.

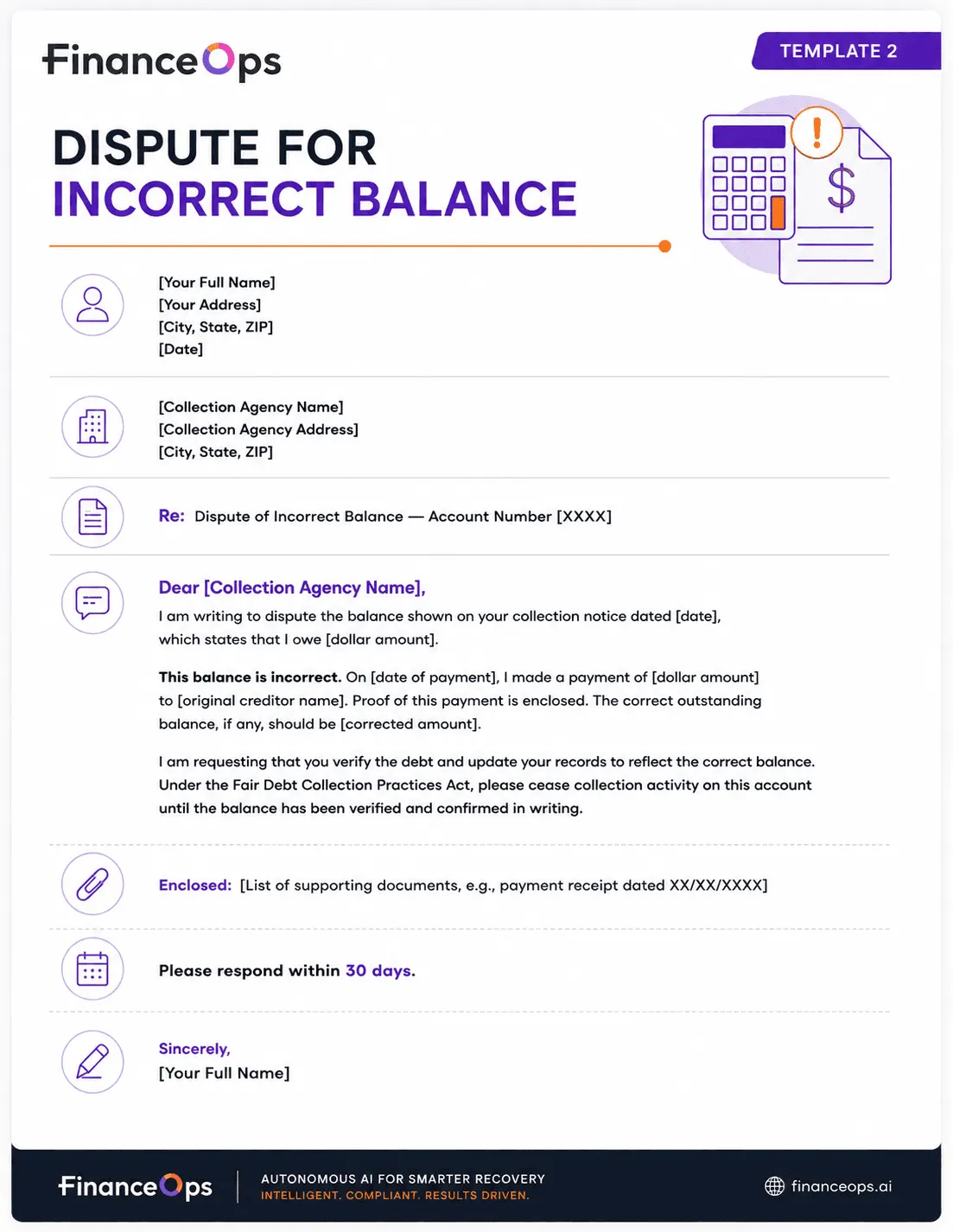

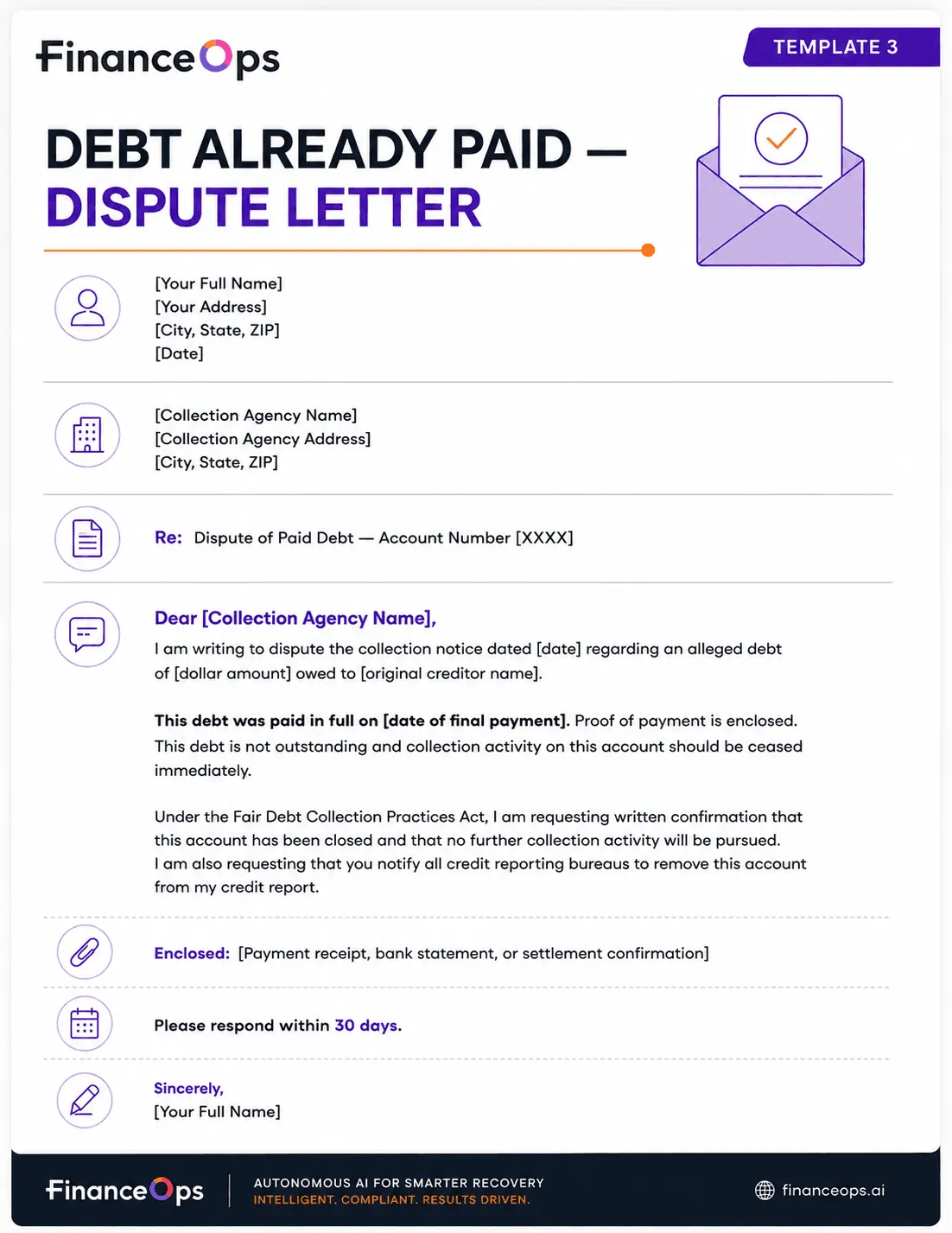

Collection Dispute Letter Templates for AR Teams

How to Respond to a Collection Dispute Letter as a Creditor

When your AR team or collections operation receives a collection dispute letter, the response must be structured, compliant, and timely. Here is the correct process.

Acknowledge receipt immediately: Log the dispute with the date of receipt and the date the 30-day response clock began. Every day of delay in acknowledging a dispute is a day of compounding compliance exposure.

Cease all collection activity on the disputed account: FDCPA requires that collection activity stop upon receipt of a written dispute until the debt is verified. This includes automated outreach, voice calls, email campaigns, and any third-party collection actions. An automated collections platform that cannot enforce this stop at the individual account level across every channel simultaneously is a compliance liability.

Gather and review all supporting documentation: Pull the original agreement, payment history, correspondence records, and any documentation establishing the right to collect. Review for the specific discrepancies the debtor identified in the dispute letter.

Send written verification within the timeframe: The verification must be sent to the debtor and must include the name and address of the original creditor and documentation validating the debt amount and the collector's right to collect.

Update the account record: Whether the dispute is resolved in favor of the creditor or results in a correction, the account record must be updated accurately. If the debt is found to be incorrect, the credit reporting bureaus must be notified.

Document every step: Every action taken in response to a dispute must be logged with dates and documentation. In the event of a CFPB inquiry or FDCPA litigation, the audit record of the dispute response is the primary evidence of compliant handling.

What Not to Do When You Receive a Dispute Letter

Do not ignore it: Ignoring a written dispute letter is an FDCPA violation. Continued collection activity after receiving a written dispute without providing verification exposes the organization to statutory damages of up to $1,000 per violation under FDCPA Section 813, plus attorney fees and actual damages.

Do not continue automated outreach without stopping it at the account level: A dispute letter stops collections activity for that specific account. If your collections platform is running automated outreach campaigns and cannot stop them at the individual account level upon dispute receipt, every automated message sent after the dispute constitutes a potential FDCPA violation.

Do not respond verbally: Dispute responses must be in writing. A phone call informing the debtor that the debt has been verified does not satisfy the FDCPA verification requirement. Written verification sent via documented mail is the standard.

Do not report the disputed debt to credit bureaus as valid during the dispute period: Reporting a disputed debt as undisputed to a credit bureau while a written dispute is pending is a violation under both FDCPA and the Fair Credit Reporting Act.

Do not rush the verification: Sending an inadequate verification, one that does not include the required documentation, to restart collection activity faster is not a compliant response. An incomplete verification does not satisfy the FDCPA requirement and exposes the organization to continued liability.

Do not treat a dispute as a collections failure: A dispute letter is information. It tells you exactly where the collections process produced a friction point significant enough that the debtor sought formal legal protection. AR teams that treat disputes as data and use them to improve upstream processes reduce their dispute rate over time. AR teams that treat disputes purely as obstacles to collect against do not.

How FinanceOps Agentic AI Prevents and Manages Collection Disputes

The majority of collection dispute letters are preventable. Not at the response stage. At the outreach stage, the invoicing stage, and the tone-calibration stage that precede any dispute by weeks or months.

FinanceOps Agentic AI addresses dispute prevention and dispute management as two connected problems with a single architectural solution.

Dispute prevention through predictive contact intelligence: The most common dispute triggers, incorrect amounts, tone mismatch, and unrecognized creditor identity, all occur before the first dispute letter is written. FinanceOps Agentic AI analyzes behavioral signals, payment history, engagement patterns, and hardship cues at the individual account level before any contact attempt is made. This produces outreach calibrated to what each specific account is communicating, not a generic collections sequence applied uniformly across the portfolio.

A member who receives empathetic, tone-appropriate outreach that reflects their actual financial situation is structurally less likely to file a formal dispute than one who receives escalatory language that does not match their circumstance. According to Deloitte's 2024 Financial Services AI Outlook, sentiment-aware AI interactions reduce formal consumer complaints in collections by up to 35%. A 35% reduction in complaints is a 35% reduction in the conditions that precede dispute letters.

Dispute prevention through automated invoice management: Reconciliation failures, where paid balances continue to appear in active collections, are one of the most common triggers for dispute letters in AR operations. FinanceOps Agentic AI automates the complete invoice lifecycle including reconciliation at the point of payment, ensuring that account status is updated in real time and that collections activity on a paid account stops before a dispute letter is written.

Dispute management through structural FDCPA compliance: When a dispute does arrive, FinanceOps Agentic AI's governed automation architecture ensures that the required response is structurally enforced rather than manually tracked. A dispute receipt triggers an automatic cease on all outreach across every channel at the individual account level. FDCPA disclosure requirements are generated automatically. Contact limits are enforced without manual intervention. The audit trail is generated at every touchpoint.

With the FCC Revoke All consent enforcement now in effect since April 2026, cross-channel consent management is no longer optional. FinanceOps Agentic AI encodes consent status as a structural property of every account record, enforcing revocation across every channel simultaneously rather than requiring manual updates across disconnected systems.

Dispute prevention through affordability-based payment plans: A significant share of disputes originate from payment commitments made under pressure that the debtor never had a realistic ability to fulfill. When commitments break, accounts age, and the debtors who feel cornered are the debtors most likely to invoke the dispute mechanism. FinanceOps Agentic AI evaluates each account's actual repayment capacity before proposing any payment structure, producing commitments the debtor can sustain and honoring them at materially higher rates. According to Deloitte, promise-to-pay abandonment rates in traditional collections average between 38% and 45%. FinanceOps Agentic AI's affordability-first approach reduces that abandonment to under 20%, directly reducing the pool of accounts that age toward dispute territory.

Key Takeaways

A collection dispute letter is the formal record of an upstream collections failure, not just a compliance event to manage. Every dispute letter your AR team receives is a retrospective signal that the outreach, invoicing, or communication process broke down at a point where intervention was still possible. AR teams that use dispute data to fix upstream processes reduce their dispute rate over time. Teams that treat disputes only as compliance events to navigate do not address the root cause.

FDCPA compliance is not a checklist. It is an architectural decision. Manual compliance tracking across a high-volume collections portfolio creates compounding regulatory exposure. With FCC Revoke All consent enforcement now in effect and state-level AI disclosure requirements expanding through 2026, the compliance environment for US collections has never been more complex. Encoding FDCPA, TCPA, and applicable state requirements as structural properties of the collections workflow before first contact is the only architecture that scales without scaling compliance risk proportionally.

The most effective collection dispute management strategy is preventing disputes before they are written. The five most common dispute triggers, incorrect balances, tone mismatch, unrecognized creditor identity, settled debts in active collections, and communication channel errors, all occur upstream of the dispute letter. FinanceOps Agentic AI addresses each of these triggers structurally through predictive contact intelligence, live sentiment analysis, automated reconciliation, and governed cross-channel compliance, reducing the conditions that cause debtors to invoke the dispute mechanism before a single dispute letter enters your queue.

Ready to reduce your dispute rate from the source?

Book a free 20-minute demo with FinanceOps Agentic AI and see how behavioral intelligence, automated compliance governance, and affordability-based payment planning reduce the upstream conditions that generate collection dispute letters in your specific portfolio.

FinanceOps Agentic AI Autopilot starts at 1.5% of collections recovered. No upfront cost. No subscription. No fee if no collections occur.

FAQs

What is a collection dispute letter and when should one be sent?

A collection dispute letter is a formal written communication sent by a debtor to a collection agency challenging the validity, accuracy, or ownership of a debt. Under FDCPA Section 809(b), it should be sent within 30 days of first written contact from the collector to trigger the automatic cease-collection-activity protection. A dispute sent after 30 days is still valid under FDCPA but does not carry the same automatic protections. The dispute must be sent in writing, preferably via certified mail with return receipt, to create a legally verifiable record of receipt.

What must a collection dispute letter include to be FDCPA compliant?

A compliant collection dispute letter must include the debtor's full name and current mailing address, the account number as it appears on the collection notice, the name of the original creditor, a clear statement that the debt is being disputed, the specific reason for the dispute, a formal request for debt validation including the original creditor's name and address and documentation establishing the collector's right to collect, and a reasonable response deadline. Supporting documentation should be attached as copies with originals retained.

What is a debt validation letter and how does it differ from a collection dispute letter?

A debt validation letter is the response that a collector sends to a debtor after receiving a dispute. It must include verification of the debt, including the name and address of the original creditor and documentation of the debt amount. A collection dispute letter is the initiating document sent by the debtor. A debt validation letter is the collector's mandatory response to that dispute. The two are legally linked under FDCPA: one triggers the obligation for the other.

How does receiving a collection dispute letter affect the creditor's AR operations?

Receiving a written collection dispute letter triggers a mandatory obligation to cease all collection activity on that specific account until the debt is verified and the verification is provided in writing to the debtor. This means automated outreach, voice calls, email campaigns, and any third-party collection actions must stop immediately at the individual account level. For AR teams running high-volume automated collections workflows, a collections platform that cannot enforce this stop across every channel simultaneously upon dispute receipt creates direct FDCPA exposure. Every automated message sent to a disputed account after receipt of a dispute letter is a potential violation.

What happens if a collection agency ignores a written dispute letter?

Ignoring a written collection dispute letter and continuing collection activity is a violation of FDCPA Section 809(b). The debtor can file a complaint with the Consumer Financial Protection Bureau and may pursue legal action under FDCPA Section 813, which provides for statutory damages of up to $1,000 per violation, plus actual damages and attorney fees. Repeated or pattern violations can result in class action exposure and regulatory investigation. For AR operations, a single ignored dispute letter that results in litigation typically costs more than the original disputed balance.

How does FinanceOps Agentic AI reduce collection dispute rates in AR portfolios?

FinanceOps Agentic AI reduces dispute rates by addressing the upstream conditions that generate disputes rather than managing disputes after they arrive. Predictive contact intelligence ensures outreach tone and timing match each account's behavioral signals, reducing the tone mismatch disputes that account for a significant share of formal complaints. Automated reconciliation at the point of payment eliminates settled-debt-in-collections disputes by updating account status in real time. Live sentiment analysis detects hardship cues before they escalate to dispute behavior. Affordability-based payment planning reduces promise-to-pay abandonment from the 38% to 45% industry average to under 20%, directly reducing the pool of accounts that age into dispute territory. When a dispute does arrive, governed automation enforces the mandatory cease-collection response across every channel at the individual account level without manual intervention. According to Deloitte's 2024 Financial Services AI Outlook, sentiment-aware AI reduces formal consumer complaints in collections by up to 35%. For AR teams, that reduction is measured in fewer dispute letters, fewer CFPB complaints, and lower regulatory exposure across the portfolio.