Understanding the Risks of Reactive Collections

In 2008, Lehman Brothers, once a leading investment bank, filed for bankruptcy, the largest corporate failure in U.S. history. The collapse stemmed from its risky investments in subprime mortgage-backed securities and collateralized debt obligations, which were backed by poorly underwritten loans. As the housing market crashed, Lehman’s exposure to these assets led to its downfall, wiping out billions and causing widespread financial damage. The collapse resulted in lost savings, pensions, and retirement funds, while shaking the financial system’s credibility and triggering economic panic and unemployment.

Lehman Brothers’ failure highlights the dangers of reactive strategies, especially in risk management. Like Lehman, many organizations wait until payments are overdue before acting, leading to rising non-performing loans, strained customer relationships, and higher costs. Reactive collections strategies put businesses at risk, emphasizing the need for proactive approaches that improve recovery rates, customer satisfaction, and efficiency.

What Are Debt Recovery Strategies?

Debt recovery strategies are data-driven methods used to recover unpaid debts, involving steps like communication, negotiating repayment plans, or using third-party agencies. However, these strategies often become reactive, only triggered after payments become overdue. Reactive methods rely on impersonal approaches, limited data, and manual processes, which can lead to difficult conversations, regulatory issues, and lost revenue. Early intervention and a customer-centric approach can prevent disputes from escalating, improving recovery rates and reducing operational debt.

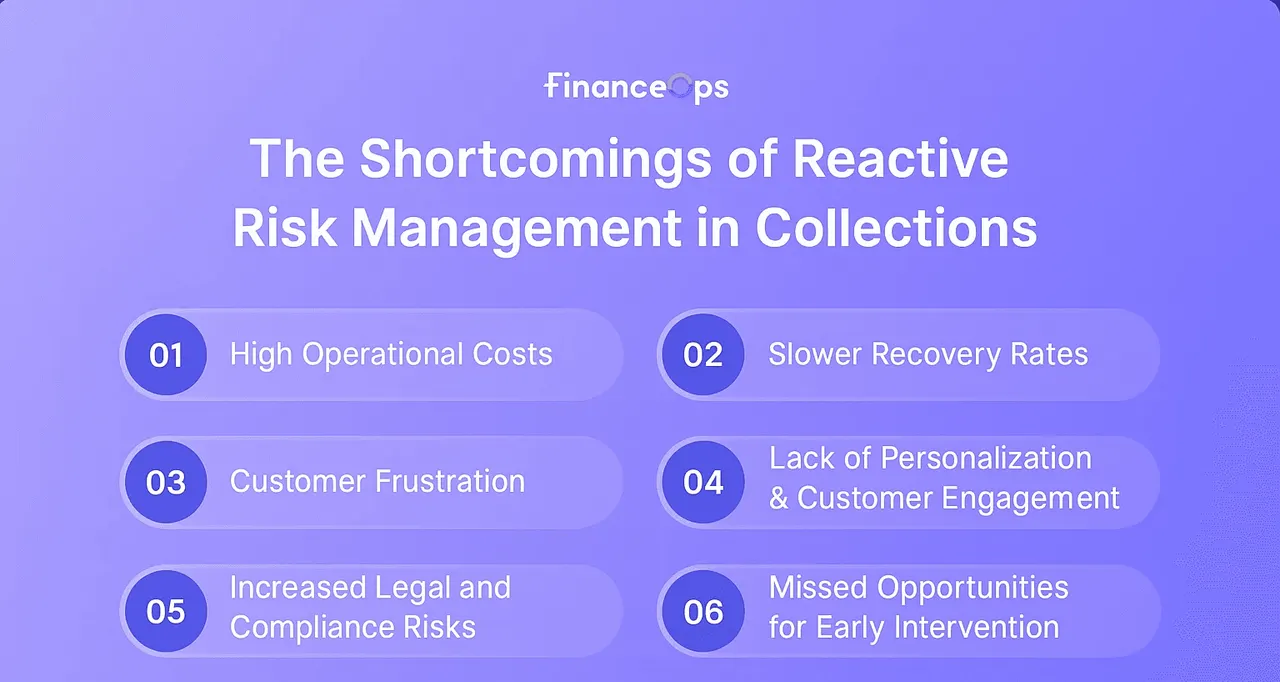

The Shortcomings of Reactive Risk Management in Collections

Relying on reactive risk management in collections introduces several specific inefficiencies and escalates risks for businesses. Here’s a detailed breakdown of those shortcomings:

1. High Operational Costs

Reactive collections often involve manual tasks like calls, letters, and legal actions, which are time-consuming and resource-heavy. Businesses rely on standardized methods, leading to inefficient, non-targeted outreach that drives up operational costs.

Example: Waiting for overdue payments may require hiring third-party agencies or expanding the in-house team, which can result in costs up to three times higher than the recovery balances, along with significant fees.

2. Slower Recovery Rates

Reactive strategies cause businesses to wait until payments become delinquent, especially for small balances, leading to longer recovery times. The delay misses the optimal window to engage customers while the debt is still manageable. Once payments are overdue by 120+ days, recovery chances decrease.

Example: Waiting 30-60 days after a customer is 30 days past due increases the likelihood of the debt being ignored or becoming uncollectible.

3. Customer Frustration

Reactive collections are often more aggressive, with inexperienced teams making frequent calls and sending notices once an account is overdue, without understanding the customer's financial situation. This can frustrate customers, damage relationships, and cause them to switch to competitors.

Example: A customer contacted by an inexperienced agent with inconsistent strategies may feel harassed, leading to non-payment, account closure, or switching to competitors, resulting in lost revenue and customer churn.

4. Lack of Personalization and Customer Engagement

Reactive collections often lack personalization, treating all customers the same regardless of their financial situation or payment history. A McKinsey survey found only 15% of businesses use personalized strategies. This one-size-fits-all approach fails to engage customers empathetically, especially during tough times like job loss or emergencies. (Source) (Source)

Example: A customer with occasional payment struggles due to a temporary setback may be treated the same as a regular defaulter, leading to misaligned strategies and reduced effectiveness, damaging customer relationships.

5. Increased Legal and Compliance Risks

Businesses using reactive strategies often rely on frequent manual follow-ups that may violate FDCPA or other local laws if they don’t follow proper guidelines. Repetitive calls, improper messaging, or mishandling customer data increases the risk of lawsuits and penalties.

Example: Calling outside permissible hours or sending improper debt notices can lead to fines or lawsuits, harming both the business’s finances and reputation.

6. Missed Opportunities for Early Intervention

By waiting until accounts are delinquent, businesses miss the chance to engage early with customers showing signs of financial trouble. Proactive risk management addresses issues before they escalate into overdue payments.

Example: A customer missing a payment by a few days may respond well to an early reminder or rescheduling offer. Waiting until multiple payments are missed reduces recovery chances and may lead to uncollectible debt.

Why Do Strategies Need a Proactive Shift in Collections?

Improved Cash Flow and Reduced DSO: Proactive strategies allow businesses to address payment issues early, improving cash flow and reducing Days Sales Outstanding (DSO). Early intervention ensures more timely payments and a stable financial position.

Enhanced Customer Relationships: Proactive collections focus on customer-centric communication, offering personalized payment options and support. This builds trust, improves customer satisfaction, and boosts retention, unlike aggressive, reactive methods.

Reduced Write-Offs and Bad Debts: By identifying potential delinquencies early, proactive strategies reduce the risk of bad debt write-offs. Predictive analytics help businesses spot high-risk accounts before they escalate.

Efficient Resource Allocation: Proactive collections allow businesses to prioritize high-risk accounts, using resources where they’re most likely to yield positive results. This improves efficiency and maximizes recovery efforts.

Regulatory Compliance and Risk Mitigation: With stricter regulations in debt collection, proactive strategies help businesses stay compliant by engaging customers transparently, reducing the risk of lawsuits, fines, and reputational damage.

Leveraging Technology: Advanced technologies such as AI and machine learning make proactive collections more efficient. These tools enable businesses to predict payment behavior, segment customers for tailored strategies, and automate reminders, enhancing overall collection effectiveness.

What Are Proactive Collection Strategies?

Proactive early-stage collection strategies are designed to prevent delinquencies before they occur, moving beyond the reactive methods that tend to create bottlenecks and inefficiencies. By leveraging advanced technologies and data-driven approaches, businesses can engage with customers early and strategically.

How to Set Up Proactive Collection Strategies?

Setting up an effective proactive collections strategy requires careful planning and execution, focusing on early intervention and customer-centric engagement. Here’s how to implement it:

Customer Data Analysis:

Gather and analyze customer data using AI-powered predictive models.

Identify customers at risk of default based on historical payment behaviors, credit scores, and financial patterns.

Segment customers into risk categories and forecast potential payment issues to take timely action before defaults occur.

Clear Credit Policies:

Establish transparent and easy-to-understand credit policies for customers.

Clearly communicate payment due dates, penalties for late payments, and available payment options.

Ensure that customers understand the terms upfront to reduce confusion and improve compliance, creating a consistent approach to collections.

Personalized Communication:

Tailor outreach based on individual customer needs and preferences.

Use multiple communication channels (SMS, email, phone calls, portals) based on the customer's preferred method.

Personalize communication to reflect the customer’s situation (e.g., financial hardship or consistent on-time payments), ensuring empathy, transparency, and consistency with your brand.

Offer Flexible Payment Plans:

Provide customizable repayment options that are adjustable to individual financial situations.

Offer installment plans, payment deferrals, or debt restructuring to help customers stay on track with payments.

Proactively offer these solutions before accounts fall into arrears, improving recovery chances and enhancing customer satisfaction.

Leverage AI Automation:

Automate reminder notifications and follow-ups to ensure timely and personalized communication without overburdening staff.

Use AI-driven automation to send messages at optimal times based on customer behavior, ensuring maximum engagement and efficiency.

This increases scalability and ensures no account is forgotten.

Continuous Monitoring and Improvement:

Regularly track key performance indicators (KPIs) like Days Sales Outstanding (DSO), Collection Effectiveness Index (CEI), and customer satisfaction metrics.

Use these KPIs to assess the success of your proactive strategies and make data-driven adjustments.

Continuous monitoring helps identify areas for improvement, ensuring the collections process evolves to maximize debt collections and recovery without losing revenue.

Leading Platforms Helping Businesses with Proactive Collections

McKinsey reports that businesses utilizing AI can reduce operational expenses by 40%, increase recoveries by 10%, and see a 30% boost in customer satisfaction (Source). Here’s how leading platforms are transforming collections:

1. HighRadius: HighRadius, based in Houston, Texas, provides AI-powered automation to streamline accounts receivable processes, including credit management, billing, payments, and collections. Their Integrated Receivables platform uses AI, Robotic Process Automation (RPA), and Natural Language Processing (NLP) to reduce manual efforts and improve cash flow.

Predictive Analytics: HighRadius predicts potential delinquencies by analyzing payment data, allowing businesses to engage proactively.

Automated Follow-ups: Timely automated reminders reduce manual effort and ensure compliance.

Data-Driven Insights: Provides actionable insights to personalize engagement, improving recovery rates.

2. AKUVO: AKUVO, located in Malvern, Pennsylvania, offers AI and machine learning-based software to optimize collections and manage loan portfolios for financial institutions, including banks and credit unions. Their products, AKUVO ProAct and AKUVO Aperture, help predict delinquencies and offer tailored solutions.

Anticipating Delinquencies: Machine learning identifies accounts at risk, enabling early action such as payment reminders.

Portfolio Risk Management: Provides visibility into loan portfolios to focus efforts on high-risk accounts.

Personalized Engagement: Uses customer data to create tailored collections strategies, improving success rates.

3. Skit.ai: Skit.ai, with offices in New York, USA, and India, specializes in conversational AI solutions for debt collection. Their platform automates customer interactions across voice, SMS, email, and chat, providing a seamless omnichannel experience.

Omnichannel AI Assistants: Engages customers through various channels, enhancing collection efforts.

Empathy-Driven Outreach: AI adjusts tone based on customer sentiment, improving relationships and repayment likelihood.

Predictive Engagement: Analyzes customer history to determine the best times for contact, maximizing collection success.

Scalable Automation: Automates large portions of the collections process, allowing businesses to scale without adding headcount.

Why FinanceOps Autopilot AI Agent Stands Out

FinanceOps Autopilot AI is an AI-driven automated collections and debt recovery solution that helps businesses recover payments faster, lower costs, and improve customer experience. It uses advanced AI for proactive, empathetic strategies, boosting recovery rates and engagement. FinanceOps increases recovery, enhances cash flow, and reduces manual effort, all while minimizing administrative overhead. Here’s how FinanceOps stands out:

Live Sentiment Analysis

The AI Agent analyzes the emotional tone of every customer interaction (via SMS, email, voice calls, or chat) in real-time.

By detecting signs of frustration, confusion, or stress, Autopilot AI Agent adjusts its tone to ensure empathetic, supportive communication. This allows for smoother, more positive conversations, improving customer relationships and increasing the likelihood of repayment.

Best Time to Contact

Using historical data from past interactions, Autopilot AI Agent identifies the optimal times to contact customers based on their past behavior.

For instance, if a customer typically responds better in the evenings or on specific days, AI Agent will schedule outreach during those times. This increases response rates, reduces missed engagements, and ensures faster resolution of overdue payments.

Suggestions for Payment Plans

Autopilot AI Agent evaluates customer data, such as income, previous payment behavior, and spending habits, to suggest personalized payment plans.

These plans are tailored to the customer’s unique financial situation, making it easier for them to commit to repayment. By offering flexible solutions, AI Agent boosts collection success rates and improves overall customer satisfaction.

Strategy Builder

Autopilot AI Agent allows businesses to create highly customized collections strategies through the Strategy Builder feature.

Users can set specific parameters and SOPs, such as the tone of communication (polite, firm, empathetic), frequency of contact, preferred contact channels (SMS, email, calls), and even the length and terms of payment plans.

This level of customization ensures businesses can adapt their approach to individual customer needs while aligning with their operational goals.

Automated Invoicing (Issue Date to Due Date)

Once the invoice is generated for the later date by the user, the AI Agent automates the entire invoicing process, from sending out invoices, tracking and reconciling them directly to customers.

If an invoice goes overdue, the AI Agent sends follow-up reminders to ensure timely payments. This reduces manual work, while being fully-compliant with due dates, and increases operational efficiency by automating routine tasks.

Benefits of Using FinanceOps Autopilot AI

Automated Outreach: Engage customers via SMS, email, voice AI calls, and IVR, ensuring timely follow-ups without manual effort.

AI-Powered Predictive Analytics: Use machine learning to predict the best time, channel, and tone for outreach based on customer data.

Debt Segmentation: Automatically categorize accounts by recovery likelihood, risk, and age, prioritizing high-value debts.

Two-Way Empathetic Communication: Provide consistent, empathetic messages across SMS, email, and voice AI, ensuring customers feel heard.

24/7 Availability: Enable round-the-clock collections, including weekends and holidays, to maximize recovery opportunities.

Real-Time Analytics & Reporting: Access live dashboards for up-to-date collection status, cash flow, and key metrics to optimize strategy.

Seamless Integration: Easily integrate with CRM, ERP, or collections systems via flexible APIs, ensuring smooth workflows.

Regulatory Compliance: Adhere to industry regulations (FDCPA, TCPA) with built-in compliance features and audit trails, reducing legal risks.

By adopting AI-driven debt recovery solutions like FinanceOps, businesses can not only improve recovery rates but also foster stronger relationships with their customers. Embracing proactive collections helps reduce costs, enhance customer satisfaction, and ensure long-term financial stability.