TL;DR

In this guide, CFOs and collections leaders will learn:

What a payment processor for debt collection is and how it differs from traditional payment processors

How payment processing in debt recovery works across cards, ACH, and digital payment links

How AI-powered payment processors improve collections performance and payment success rates

Why Does A Payment Processor Matter in Debt Collection?

For CFOs, finance leaders, and collections teams, recovering outstanding balances depends on more than outreach strategies and negotiations. The final step, actually completing the payment, is where many collections processes fail. This is where a payment processor becomes critical. A payment processor for debt collection allows organizations to securely accept payments from customers across multiple channels while ensuring regulatory compliance and operational efficiency.

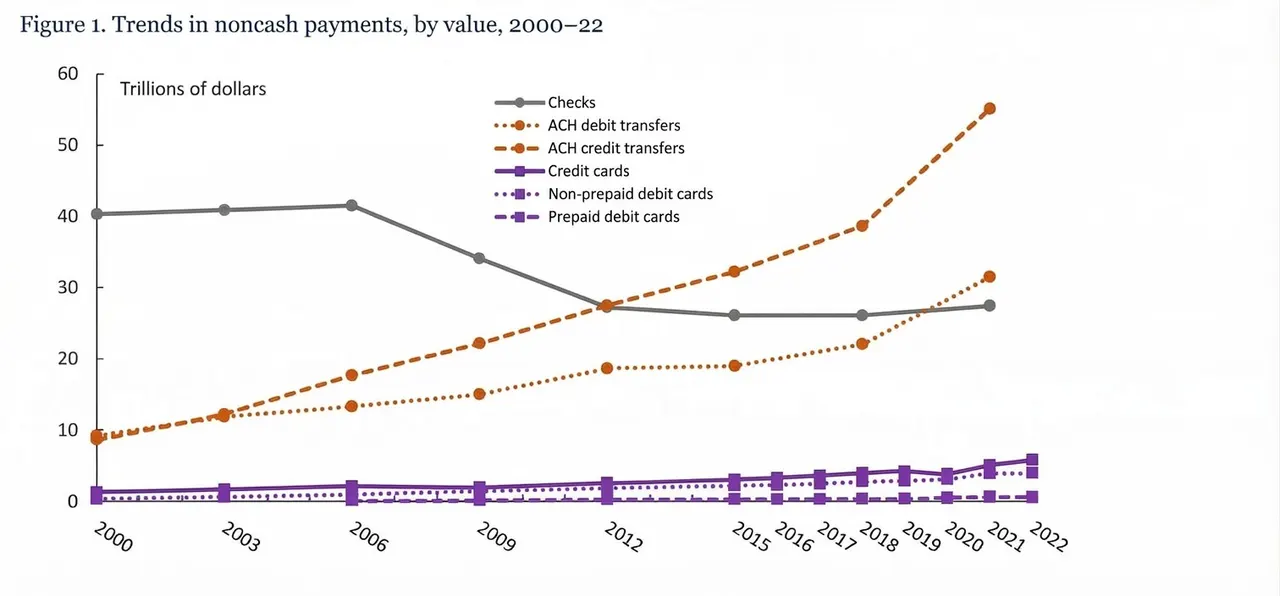

According to the Federal Reserve Payments Study, the digital payment infrastructure is now the primary foundation of the U.S. financial system, from 2000 to 2022, both the value and number of non-cash transactions increased significantly, reflecting a structural shift away from paper-based payments toward digital payment systems.

Customers expect simple, mobile-friendly ways to complete payments. If the payment process is difficult or confusing, recovery rates decline significantly. For small businesses and financial institutions alike, choosing the right payment processor services can mean the difference between:

delayed collections and strong cash flow

manual processes and automated payments

compliance risks and regulatory confidence

Understanding how payment processing works in collections environments is therefore essential.

What Is A Payment Processor in Debt Collection And Recovery

A payment processor is a financial technology service that handles electronic transactions between customers and businesses. In debt recovery environments, a payment processor for debt collection performs several specialized functions beyond basic payment acceptance. These include:

processing payments from delinquent accounts

managing partial payments and installment plans

supporting multiple payment methods

ensuring compliance with debt collection regulations

synchronizing payments with collections systems

Payment processor services used in collections typically support several payment types:

credit and debit card payments

ACH bank transfers

e-check payments

digital wallet payments

SMS payment links

online payment portals

For organizations operating with limited financial infrastructure, a reliable payment processor for small business like FinanceOps agentic AI helps simplify collections and payment management.

How Payment Processing Works in Debt Recovery

Payment processing in collections follows a structured workflow that converts debtor commitments into completed transactions.

Step 1: Payment commitment

The process begins when a debtor agrees to repay an outstanding balance or enrolls in a structured payment plan. This agreement may occur through a conversation with a collections agent, a digital interaction, or an automated communication.

Step 2: Payment request generation

Once a commitment is made, the payment processor generates a payment request that can be delivered through multiple channels, including:

SMS payment links

Email invoices

Online payment portals

Voice or IVR payment systems

These options provide customers with convenient and flexible ways to complete their payments.

Step 3: Payment submission

The debtor selects their preferred payment method and submits the payment by entering the required details, such as credit card information, bank account details for ACH transfers, or other supported payment options.

Step 4: Authorization and verification

The payment processor securely transmits the transaction request to the appropriate bank or card network. The financial institution then verifies the payment details and authorizes the transaction.

Step 5: Settlement and reporting

Once the payment is approved, the transaction proceeds to settlement. The funds are transferred, and the collections platform automatically updates the debtor’s account balance and payment status.

Modern payment processors, such as FinanceOps Agentic AI, integrate directly with collections platforms through APIs and webhooks. This ensures real-time payment visibility, automated account updates, and accurate financial reporting for collections teams and finance leaders.

Why Choosing The Right Payment Processor Matters For CFOs

Faster payment completion

When payment options are simple, secure, and mobile-friendly, customers are far more likely to complete transactions promptly. A modern payment processor enables multiple payment channels and streamlined payment experiences, reducing friction and increasing the likelihood that commitments to pay turn into actual payments.

Improved regulatory compliance

Debt collection payments must adhere to strict regulatory frameworks, including:

Fair Debt Collection Practices Act (FDCPA)

Telephone Consumer Protection Act (TCPA)

Specialized payment processors designed for collections environments incorporate built-in compliance safeguards, helping organizations ensure that payment interactions follow regulatory guidelines and minimize legal risk.

Greater operational visibility

Teams require clear, real-time insights into collections and payment performance. Key metrics often include:

payment success rates

failed or declined transactions

installment and payment plan performance

overall collections pipeline activity

Integrated payment processor services provide centralized dashboards and automated reporting, enabling finance leaders to monitor performance, identify trends, and make informed decisions that improve recovery outcomes and cash flow management.

Key Features To Look For in Payment Processor Services

Real-time payment processing

Real-time payment authorization and confirmation reduce uncertainty for both customers and collections teams. Instant transaction visibility allows agents and finance teams to quickly verify successful payments, update accounts, and shift their focus to other active recovery efforts.

Compliance with financial regulations

Payment processing within collections environments must comply with strict regulatory standards, including:

Fair Debt Collection Practices Act (FDCPA)

Telephone Consumer Protection Act (TCPA)

PCI DSS (Payment Card Industry Data Security Standard)

A reliable payment processor should embed these compliance requirements into its payment workflows, helping organizations minimize legal risks while maintaining regulatory integrity.

Omnichannel payment acceptance

Today’s customers expect flexibility when making payments. A modern payment processor should support multiple payment channels, allowing debtors to pay through whichever option is most convenient. These channels may include:

SMS payment links

Email invoices

Voice or IVR payment systems

Online payment portals

Omnichannel payment acceptance reduces friction in the payment process and increases the likelihood that customers will complete transactions.

Secure payment handling

Protecting sensitive financial information is essential. Strong security practices, such as tokenization, end-to-end encryption, and secure authentication protocols, help safeguard payment data and protect both customers and organizations from fraud or data breaches.

Flexible payment plans

Many customers facing overdue balances may not be able to repay the full amount immediately. Payment processors that support installment and recurring payment plans (weekly, bi-weekly, or monthly) enable organizations to offer flexible repayment options. These structured payment arrangements often improve long-term recovery rates while maintaining positive customer relationships.

How Payment Processors Integrate With Collections Platforms

A modern payment processor for debt collection must integrate seamlessly with collections management systems to ensure smooth, automated financial operations. Effective integration eliminates manual processes, improves payment visibility, and enables collections teams to manage recovery activities more efficiently.

Most integrations occur through secure APIs and webhooks, which allow the payment processor and the collections platform to exchange data in real time. This connection enables several critical capabilities, including:

Automated payment reminders: Payment requests and reminders can be triggered automatically based on due dates, promises-to-pay, or payment plan schedules.

Real-time payment updates: As soon as a payment is completed, the system reflects the updated status instantly, allowing teams to track payments without delays.

Automatic account reconciliation: Payments are automatically matched to the correct customer accounts, reducing the need for manual reconciliation and minimizing errors.

Centralized reporting dashboards: Finance and collections leaders gain access to consolidated dashboards that display payment performance, outstanding balances, and recovery trends.

For example, when a debtor completes a payment through an SMS or email payment link, the payment processor immediately sends the transaction data back to the collections platform. The system automatically updates the debtor’s account balance, records the payment, and reflects the change in reporting dashboards.

By connecting payments and collections workflows through real-time integrations, organizations can significantly improve operational efficiency, reduce administrative work, and provide finance teams with accurate, up-to-date financial insights.

Common Payment Processing Mistakes in Debt Recovery

Many organizations face challenges because they rely on payment infrastructure designed for retail transactions rather than collections operations. Debt recovery workflows require specialized capabilities such as compliance safeguards, flexible payment options, and integrated reporting that traditional processors may not provide.

Ignoring regulatory compliance

Debt collection payments must comply with strict regulatory frameworks. Using payment processors without built-in compliance features can create legal and financial risk. Payment systems should support regulations such as the Fair Debt Collection Practices Act (FDCPA) and the Telephone Consumer Protection Act (TCPA), while maintaining PCI DSS security standards.

Limiting payment methods

Restricting payment options reduces the likelihood that customers complete payments. Many debtors prefer convenient digital channels such as mobile payment links or ACH transfers. Limited payment methods create unnecessary friction and reduce recovery opportunities.

Using disconnected systems

When payment processing systems operate separately from collections platforms, teams often face manual reconciliation, delayed updates, and fragmented reporting.

Selecting payment processor services designed for debt recovery environments helps avoid these issues by combining secure payments, regulatory compliance, and seamless integration with collections systems.

Benefits of AI-Powered Payment Processors

An AI-powered payment processor enhances payment workflows by introducing automation and predictive intelligence, helping collections teams improve efficiency and increase payment completion rates. The Federal Reserve Payments Study confirms a long-term structural shift toward digital, automated, and integrated payment systems.

Payment intent analysis

AI systems can analyze debtor communications and behavioral signals to identify payment intent. Based on these insights, the system can trigger timely payment requests or generate payment links to facilitate faster transactions.

Best time to request payments

Machine learning models analyze historical payment patterns and engagement data to determine the most effective time and communication channel for payment outreach.

Automated payment follow-ups

AI can automatically send payment reminders, payment links, and follow-up communications across multiple channels, ensuring consistent engagement with customers.

Best Payment Processors for Debt Collection And Small Businesses

Several payment processors serve different segments of the market, depending on business needs, transaction types, and operational requirements.

While general payment processors support a wide range of industries, platforms such as FinanceOps Agentic AI combines payment processing with collections automation, enabling organizations to manage the entire debt recovery lifecycle more efficiently.

Key Takeaways

Payment infrastructure determines recovery outcomes: Debt recovery does not fail only at negotiation, it often fails at execution. If customers cannot pay easily through secure, mobile-friendly, omnichannel options, commitments to pay rarely convert into actual payments.

Collections-specific payment processors outperform generic systems: Payment infrastructure designed for retail transactions lacks the compliance safeguards, payment plan capabilities, and integrations required for debt recovery.

AI-powered payment processing is redefining collections performance: Artificial intelligence improves payment workflows by predicting the best time and channel for outreach, analyzing payment intent, and automating follow-ups.

FinanceOps Agentic AI combines AI-driven collections automation and integrated payment processing to help organizations recover payments faster while maintaining full compliance.

Book a 20-minute demo with FinanceOps to streamline your collections and payments infrastructure.

FAQs

What is the best payment processor for small businesses in debt recovery?

The best payment processor for small businesses in debt recovery should offer low fees, fast processing, and seamless integration with collections platforms. Solutions like FinanceOps combine payment processing, collections automation, and AI-driven insights.

How does payment processing integrate with debt recovery platforms?

Payment processors integrate with debt recovery platforms through APIs and webhooks, enabling automated payment collection, reminders, real-time tracking, and automatic account updates.

How do I ensure my payment processor complies with debt collection regulations?

Choose a processor that complies with FDCPA, TCPA, and PCI DSS security standards. Platforms like FinanceOps embed regulatory guardrails into payment and collections workflows.

Can a payment processor support recurring payments in debt recovery?

Yes. Many payment processors support recurring billing and installment payment plans, allowing organizations to automate payment collection and improve cash flow.

What payment methods should a processor support for debt recovery?

A reliable processor should support credit/debit cards, ACH transfers, e-checks, digital wallets, and mobile payment links to provide flexibility for customers.