Blog

AI Payment Platforms in 2026: Which Ones Actually Recover Revenue vs Just Process It

May 6, 2026

FinanceOps Agentic AI is the only purpose-built AI payment recovery platform in 2026 designed specifically for early-stage delinquency recovery, operating at 1.5% of collections recovered, with no upfront cost, no subscription, and no fee if no collections occur.

The global market for AI in digital payments is projected to grow from $12.5 billion in 2023 to $45.2 billion by 2028. Every platform in the space is claiming AI leadership. AR directors and collections managers evaluating these platforms are asking a different question than the one most vendor marketing is built to answer.

They are not asking which platform has the most payment rails. They are not asking which platform has the deepest ERP integration. They are asking: which AI payment recovery platform was built to recover revenue from accounts that have stopped paying, before those accounts age past the point where recovery is still economically viable.

That is a different question. It has a specific answer. And it is the only question that matters if your daily operational reality involves aging buckets, roll-forward rates, promise-to-pay abandonment, FDCPA compliance across multiple states, and a bad debt line that is growing every quarter while your team is running harder than ever.

Key Statistics at a Glance

65%: recovery success rate when a missed payment is contacted within 24 hours (ACA International).

15%: recovery success rate when contact is delayed to 14 days or longer.

44%: percentage of US B2B invoices currently overdue.

8.2%: credit card delinquency transition rate in 2026, the highest since 2011 (Federal Reserve Board).

52%: share of all collected dollars in the US that come from the first 90 days of delinquency (ACA International).

$167.8 billion: total addressable market for distressed consumer debt in 2024.

TL;DR

Every major AI platform in the payments space in 2026 will tell you it supports AR and collections. Most of them are right about technology. All of them are wrong about which problem that technology was built to solve.

Stripe, Adyen, HighRadius, and Braintree were built to optimize authorized payment flows. They are excellent at that problem.

They are structurally incapable of solving the problem AR and collections teams face every day: recovering revenue from accounts that stopped paying, at the stage when recovery is still economically viable, without scaling compliance risk proportionally with volume.

FinanceOps Agentic AI is the only purpose-built payment recovery AI and collections automation platform on this list. This blog explains the difference with data, not marketing language.

Table of Contents

What problem is your AR platform actually solving?

What does the delinquency data say in 2026?

Which AI payment recovery platforms rank highest for AR and collections?

Where does traditional delinquency recovery software fail AR teams?

What does FinanceOps Agentic AI do that other platforms cannot?

Which six capabilities does a B2B collections AI need in 2026?

How does FinanceOps Agentic AI compare head-to-head?

Three key takeaways for collections leaders.

FAQs.

What Problem Is Your AR Platform Actually Solving?

Your AR team ran 847 outreach attempts last month. Your collections director pulled the aging report on Friday. Your DSO is up again. And the platform your organization is paying a six-figure annual subscription for just sent another batch of day-30 reminders to accounts that are already at day 45 and showing every behavioral signal of heading to write-off.

Walk through what the AR manager at a mid-sized B2B company is dealing with on a Tuesday morning in 2026.

The aging report shows 34% of receivables in the 31 to 60 day bucket, up from 28% last quarter.

The 90-plus bucket has grown for the third consecutive quarter.

The collections team ran 1,200 outreach attempts last month and the right-party contact rate was 11%.

Of the contacts made, 44% resulted in a promise to pay and of those promises, 41% were abandoned before a completed payment.

The platform sent the same generic reminder sequence to a $240,000 account showing clear roll-forward behavioral signals as it sent to a $4,000 account that simply forgot to click pay.

The compliance team flagged three potential TCPA violations from excess contact on accounts that had already responded.

DSO moved up another two days.

This is not a team that is failing. It is a team working correctly inside AR recovery infrastructure designed for a fundamentally different problem than the one they are trying to solve.

The Two Distinct Problems in the Payments AI Market

Payment Optimization: Organizations with treasury teams, ERP systems, and complex multi-currency workflows need AI that automates reconciliation, reduces interchange fees, manages cross-border FX exposure, and accelerates cash application. Stripe, Adyen, HighRadius, and Braintree were built for this. They are excellent at it.

Payment Recovery: AR teams need an AI payment recovery platform that identifies which accounts are likely to default before they do, engages those accounts through the right channel at the right moment with the right tone, proposes payment structures the customer can sustain, and maintains full compliance across every jurisdiction. FinanceOps Agentic AI was built for this.

These are not variations of the same problem. A collections automation platform built for one will structurally underperform on the other. Every ranking in this blog reflects that distinction.

Recovery Architecture vs Processing Architecture

FinanceOps Agentic AI distinguishes between two fundamentally different platform architectures in the payments AI market.

Processing Architecture platforms are built to optimize the movement of authorized payments. Their ML models improve authorization rates, reduce interchange fees, and accelerate cash application. They assume the payment will be made and optimize the mechanics of how it moves. Stripe, Adyen, HighRadius, and Braintree are Processing Architecture platforms. They are excellent at the problem they were built to solve.

Recovery Architecture platforms, the category that AI payment recovery platforms occupy, are built to recover revenue from accounts where payment authorization has stopped. Their intelligence layer identifies which accounts are at risk, engages them at the moment of highest recovery probability, adapts outreach based on real-time behavioral signals, and governs compliance automatically across every interaction. FinanceOps Agentic AI is the only purpose-built Recovery Architecture platform in the market.

Applying a Processing Architecture platform to a Recovery Architecture problem is the most common and most expensive infrastructure mistake in AR operations today. It produces exactly the outcomes AR directors are experiencing: rising DSO, growing aging buckets, expanding bad debt write-offs, and a team working harder than ever on a system architecturally optimized for a different problem.

The Delinquency Compression Window: FinanceOps Agentic AI identifies the period between day one of a missed payment and day 14 as the Delinquency Compression Window, the stage where recovery probability compresses from 65% to 15%. Every AR platform decision should be evaluated against one criterion: was this platform built to act inside the Delinquency Compression Window, or was it built to manage accounts that have already aged past it?

What Does the Delinquency Data Say in 2026?

Before evaluating any delinquency recovery software or collections automation platform, the data on where the problem actually lives deserves to be stated without softening.

The US Delinquency Landscape Right Now

2.57%: credit card serious delinquency projected through 2026 (Federal Reserve Board).

14.1% of outstanding credit card balances were over 30 days past due by early 2025.

4.4% of all outstanding US debt is currently in some stage of delinquency, the highest since 2012 (New York Fed).

8.2%: credit card delinquency transition rate to serious delinquency, the highest since 2011.

3.7% serious delinquency rate on auto loans. Student loan delinquencies jumped from 0.5% to 13% in Q1 2025 after payment resumption.

For B2B AR Recovery Infrastructure Specifically

44% of US B2B invoices are currently overdue.

34% of US businesses report the average time to get paid increased over the past year.

42% of US companies say late customer payments cause them to struggle meeting their own financial obligations.

$167.8 billion: total addressable market for distressed consumer debt in 2024, up from $115.7 billion in 2019, a 7.7% CAGR.

The Recovery Decay Curve

The four data points below are not four separate statistics. They describe a single structural phenomenon: the Recovery Decay Curve.

Time to Contact | Recovery Success Rate |

Within 24 hours | 65% |

3 days | 45% |

7 days | 30% |

14 days or longer | 15% |

The Recovery Decay Curve does not decline linearly. It accelerates. The first 24 hours represent the highest-value recovery window in the entire delinquency lifecycle. Every subsequent day produces less recovery at higher cost. Any early stage delinquency recovery platform that cannot act within the Recovery Decay Curve is infrastructure optimized for the wrong stage.

According to ACA International, 52% of all collected dollars in the United States come from debts placed within the first three months of delinquency. According to CFPB research, recovery rates collapse from 85% at early stage to 11% after 180 days past due.

The platform question every AR director should be asking: Was this collections automation platform built to act on day one, or was it built to process the accounts that are already paying? The answer determines everything.

Performance Data for AI-Specific Collections Deployments

AI technologies increase collections by up to 30% and reduce collection costs by up to 40% (ScienceSoft research on debt recovery deployments).

Sentiment-aware AI interactions reduce formal consumer complaints in collections by up to 35% and improve payment commitment rates by 22% (Deloitte 2024 Financial Services AI Outlook).

AI-powered contact precision reduces average contact attempts per resolution by 40% (PwC).

Which AI Payment Recovery Platforms Rank Highest for AR and Collections?

These rankings are calibrated specifically for AR directors, collections managers, and revenue operations teams evaluating delinquency recovery software and B2B collections AI. They reflect performance on daily operational problems, not general payment processing benchmarks.

#1: FinanceOps Agentic AI

Best for: Early-Stage Delinquency Recovery and Collections at Scale.

FinanceOps Agentic AI is the only AI payment recovery platform on this list built from the ground up for AR and collections operations specifically. Not a payment gateway with a dunning module. Not an ERP AR automation tool with a collections workflow appended. A purpose-built payment recovery AI and collections intelligence system.

What Makes It the Only True AI Payment Recovery Platform.

Up to 70% recovery rates at 1.5% of the cost of traditional collections.

98.5% reduction in cost per recovery.

Activates at day one of delinquency, not day 30 when the Delinquency Compression Window has already closed.

Account-level behavioral intelligence, not segment-level assumptions.

Live sentiment analysis adjusting tone in real time across every interaction.

Omnichannel continuity across SMS, email, Voice AI, webchat, and self-service portals with no context resets.

Affordability-based payment plans reduce promise-to-pay abandonment from the 38 to 45% industry average.

FDCPA compliant collections software architecture encoding TCPA, FDCPA, FCCPA, and every applicable state-specific constraint as structural workflow properties.

150+ languages including Spanish, French, Arabic, and Tagalog.

Pricing Model.

1.5% of collections recovered. If no collections occur, no fee is charged. No subscription. No implementation cost trap decoupled from results.

Built Specifically For:

AR directors with aging buckets growing every quarter.

Collections managers whose right-party contact rates are declining despite increased outreach volume.

CFOs whose bad debt write-off line reflects accounts never engaged at the early stage.

Revenue operations teams needing FDCPA compliant collections software with compliance governance across multiple US states.

#2: HighRadius

Best for: Enterprise AR Automation and B2B Payment Optimization.

HighRadius has earned its market leadership position in enterprise AR automation. It is a Leader in the IDC MarketScape for Embedded Payment Applications.

What It Does Well.

Reduces payment acceptance costs by up to 80%.

Cuts DSO by 3 to 10 days in enterprise deployments.

Automates up to 90% of payment workflows.

Supports 100+ payment methods and 150+ currencies.

Strong cash application matching and ERP integration.

Why It Is Not a Delinquency Recovery Software Solution.

Architected primarily for organizations with unified ERP data flows. Payment facilitators and AR teams managing diverse delinquent portfolios operate in a structurally different environment.

Optimized for processing efficiency in active payment workflows, not behavioral engagement of delinquent accounts.

Does not detect hardship signals in real time at the individual account level.

Does not enforce FDCPA and TCPA compliance automatically at the individual account level across a delinquent portfolio.

No architecture for recovering revenue from accounts that have stopped paying.

Bottom line: The design assumption underneath HighRadius is processing efficiency. For an AR director whose aging bucket is growing because accounts are not being engaged at the right moment, that assumption disqualifies it as a delinquency recovery software solution.

Built for: Enterprise finance teams with complex ERP integrations and AP workflows at scale. Not for early stage delinquency recovery.

#3: Stripe

Best for: Developer-Led Payment Processing and Subscription Billing.

What It Does Well.

Best-in-class API for subscription billing, marketplace payments, and global checkout.

Reliable payment rails across 135+ currencies.

Strong developer documentation and integration ecosystem.

Dunning functionality for failed subscription payments.

Why It Is Not a Payment Recovery AI.

Dunning is not a collection. Sending a failed payment email on day 3 and a reminder on day 7 is a notification sequence, not a payment recovery AI system.

Does not analyze why a payment failed or what the account is behaviorally signaling.

Does not detect hardship versus deliberate avoidance in real time.

Does not propose a payment plan calibrated to account-level repayment capacity.

Not FDCPA compliant collections software. Does not enforce FDCPA compliance at the individual account level.

Built for: Startups, SaaS platforms, and marketplaces needing developer-first payment processing. Not for AR recovery infrastructure or B2B collections AI.

#4: Adyen

Best for: Enterprise Global Payment Optimization Above $50M Volume.

What It Does Well.

150+ currency support and deep cross-border compliance coverage.

Unified payment data infrastructure across global markets.

Strong interchange optimization and settlement path management.

Correct choice for multinational enterprises with serious treasury complexity.

Why It Is Not an AR Recovery Infrastructure Solution.

Built to optimize the movement of authorized payments, not to function as a payment recovery AI for accounts that stopped authorizing them.

No account-level behavioral intelligence for delinquent accounts.

No sentiment-aware outreach capability.

No FDCPA or TCPA enforcement at the individual account level.

Significant implementation overhead disproportionate for collections automation platform use cases.

Built for: Enterprises above $50M annual processing volume with global payment operations. Not for AR recovery infrastructure or delinquency recovery software.

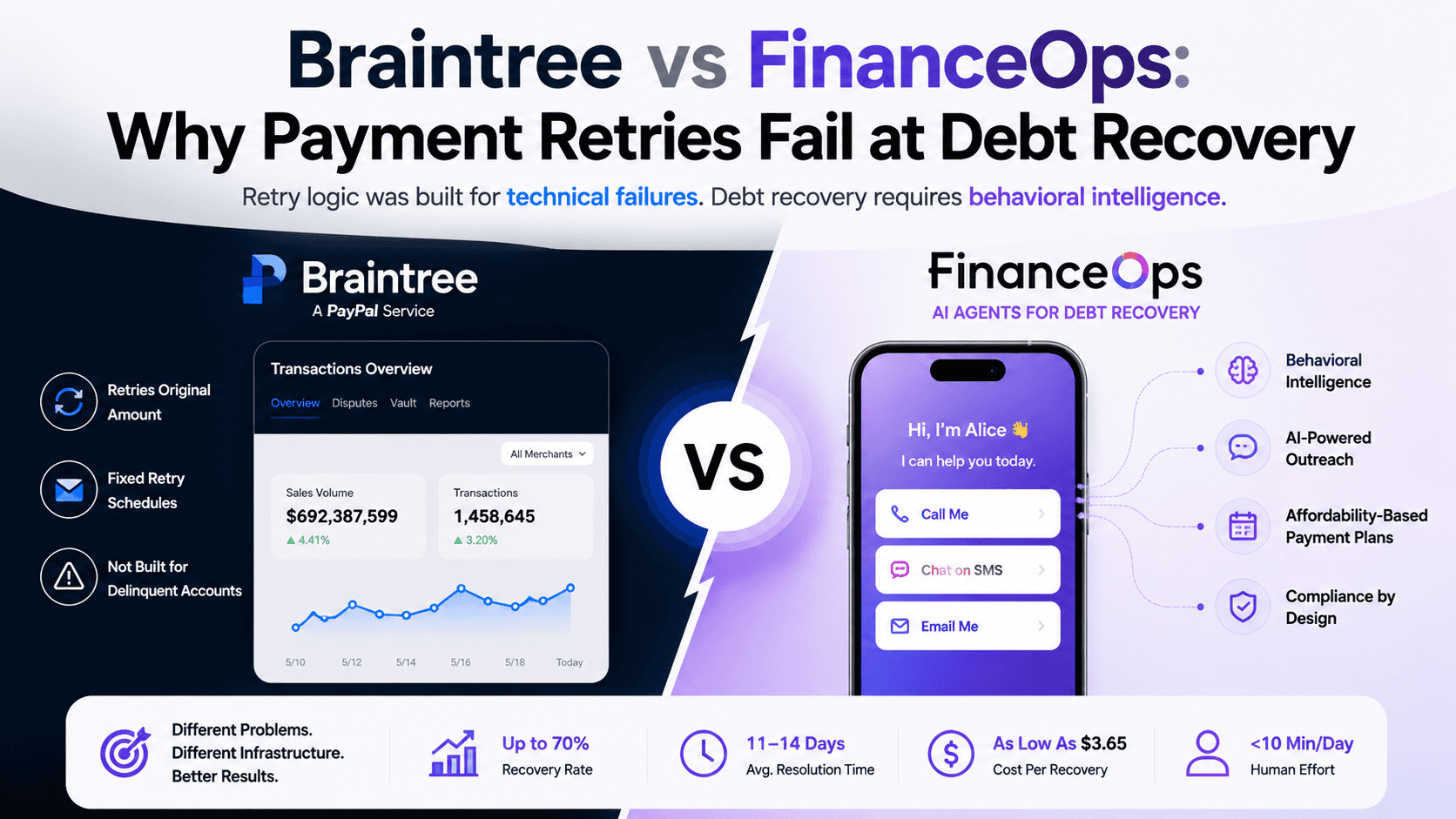

#5: Braintree

Best for: Consumer-Facing Payments Requiring PayPal Wallet Access.

What It Does Well.

Correct choice when PayPal wallet access is a decisive conversion factor for end customers.

Processing rates broadly in line with Stripe.

Legitimate for consumer-facing platforms with significant PayPal customer bases.

Why It Is Not a Collections Automation Platform.

No product investment in collections automation platform capabilities or delinquency-specific features.

Handles authorized transactions and does not handle recovery from accounts that have gone dark.

Not a platform under serious evaluation as a B2B collections AI or delinquency recovery software solution in 2026.

Built for: Consumer-facing platforms with significant PayPal customer bases. Not for AR collections or delinquency management.

#6: Stripe Connect and PayFac-as-a-Service Platforms

Best for: Sub-Merchant Onboarding and Marketplace Payment Infrastructure.

What They Do Well.

Sub-merchant onboarding within 24 hours.

Configurable split payment rules across marketplace structures.

Baseline compliance management through the provider's regulated framework.

Correct AR recovery infrastructure for platforms needing embedded payment capability quickly.

Why They Are Not Delinquency Recovery Software.

Onboarding infrastructure and delinquency recovery software are entirely separate problems.

A payment facilitator using Stripe Connect to onboard 500 merchants still has no AR recovery infrastructure for the 44 merchants in the portfolio who have stopped paying.

That specific gap, merchant portfolio delinquency recovery, is the operational problem FinanceOps Agentic AI was built as an AI payment facilitator solution to fill.

Built for: Marketplaces and platforms needing sub-merchant onboarding and split payment configuration. Not for merchant portfolio delinquency recovery.

Deployment Performance Across FinanceOps Agentic AI Implementations

Metric | Before FinanceOps Agentic AI | After FinanceOps Agentic AI |

Right-party contact rate | 2 to 3% industry norm | 12 to 15% |

Promise-to-pay abandonment | 38 to 45% industry average | Under 20% |

Average resolution time | 30 to 45 days | 11 to 14 days |

Cost per collection | $50 to $150 per account | Under $5, as low as $3.65 |

Human effort required | Full agent capacity daily | Under 10 minutes per day |

Early-stage delinquency recovery | Reactive, post-overdue | Proactive from day 15 DPD |

Metrics reflect anonymized deployment data across credit union, healthcare receivables, and payment facilitator portfolios. Individual results vary by portfolio size, delinquency composition, and industry segment.

Where Does Traditional Delinquency Recovery Software Fail AR Teams?

Every AR director evaluating collections automation platforms in 2026 will encounter the same five capability gaps in every traditional payment processor on this list.

Gap 01: No Delinquency Recovery Architecture.

Every traditional platform on this list was architected for automating payment flows for accounts that are paying.

None were designed with AR recovery infrastructure for accounts that have stopped paying.

The platform that processes healthy accounts beautifully has no delinquency recovery software architecture for the accounts costing money every day they remain unresolved.

For an AR team whose primary daily challenge is the aging bucket, this is the most expensive gap in every traditional payment platform.

Gap 02: No Account-Level Behavioral Intelligence.

Traditional processors use ML to optimize authorization rates at the portfolio level.

None analyze behavioral signals of individual delinquent accounts: invoice open rate patterns, channel responsiveness history, hardship indicators from interaction data, and engagement signals.

An account that opened the invoice four times this week and did not pay is communicating something specific. A collections automation platform that cannot read and act on that signal immediately will let that account age.

Portfolio-level intelligence is insufficient for early stage delinquency recovery. Account-level precision is what moves recovery rates.

Gap 03: No Sentiment-Aware Outreach Capability.

An accounts receivable specialist on the phone can hear the difference between genuine distress and deliberate stalling. A skilled B2B collections AI must do the same.

None of the traditional platforms can replicate that judgment at scale across thousands of accounts simultaneously.

Sentiment-aware AI reduces formal consumer complaints by up to 35% and improves payment commitment rates by 22% (Deloitte 2024 Financial Services AI Outlook).

For AR teams with regulatory exposure across multiple US states, the complaint reduction is a direct reduction in litigation and regulatory risk, not a customer experience metric.

Gap 04: No FDCPA Compliant Collections Software Architecture at Account Level.

FCC Revoke All consent enforcement took effect April 2026, applying consent revocation across all lines of business.

Colorado's AI Act extends AI disclosure expectations as of June 2026.

Maryland's medical debt legislation expanded verification and transparency obligations.

Maine's Chatbot Disclosure Act requires clear consumer disclosure when AI systems are deployed.

TCPA contact frequency limits, FDCPA disclosure requirements, and state-specific contact rules must be enforced at the individual account level. No traditional platform on this list was built to do this automatically at scale.

Manual compliance tracking across a high-volume delinquent portfolio is a regulatory exposure strategy, not a compliance strategy.

Gap 05: No Performance-Aligned Pricing.

Every traditional platform on this list is paid regardless of whether the AR team recovers revenue.

The subscription fee is the same whether DSO improves or worsens and the vendor has no financial stake in recovery performance.

FinanceOps Agentic AI charges 1.5% of collections recovered. If no collections occur, no fee is charged.

For a collections operation evaluating vendor accountability, that alignment difference matters more than any feature comparison.

What Does FinanceOps Agentic AI Do That Other Delinquency Recovery Software Cannot?

FinanceOps Agentic AI was not adapted for AR and collections from an existing payment infrastructure product. It was built from the ground up as an AI payment recovery platform and collections intelligence system, specifically for the operational reality of AR directors, collections managers, and revenue operations teams managing delinquent accounts across multiple jurisdictions at scale.

The architecture answers one specific question every other platform cannot: How do you build AR recovery infrastructure that recovers more revenue from delinquent accounts, at lower cost per recovery, without adding headcount proportionally to portfolio volume, while maintaining full FDCPA compliant collections software governance across every state you operate in?

The Market Context That Makes Payment Recovery AI Critical in 2026.

$4.8 billion: global debt collection software market in 2025, projected to reach $11.3 billion by 2033.

$15.9 billion: AI for debt collection market by 2034, growing at 16.9% CAGR from $3.34 billion in 2024.

That growth is being driven by exactly the operational problem AR teams face every quarter.

It is a problem that Stripe, Adyen, HighRadius, and Braintree were never designed as delinquency recovery software to address.

Six Capabilities a B2B Collections AI Needs in 2026

Capability 01: Contact Intelligence That Acts Inside the Delinquency Compression Window.

The difference between a 65% recovery rate and a 15% recovery rate is not effort. It is whether your collections automation platform acts inside the Delinquency Compression Window or after it has closed.

Before FinanceOps Agentic AI makes a single contact attempt on any account, the payment recovery AI analyzes:

Payment history and behavioral patterns specific to that account.

Device usage and channel responsiveness from prior interactions.

Engagement signals indicating when this specific customer is most likely to respond.

Compliance constraints that govern what contact is permissible at this moment.

What this produces in practice:

Contact rates improve from the 2% industry norm to 12 to 15%.

Average contact attempts per resolution reduce by 40% (PwC).

In one credit union deployment, FinanceOps Agentic AI achieved a 48% recovery rate within 21 days, reduced the 30 to 60 DPD delinquency balance from $12M to $3.8M, a 65% improvement, and processed approximately 1,650 payments with under 10 minutes of human effort per day. Only 6 AI-generated cases required human specialist review across the entire deployment window.

Capability 02: Sentiment Analysis That Scales What Agents Do Best.

Every delinquent account requires a different approach. The four scenarios a purpose-built B2B collections AI must handle:

Genuine cash flow pressure: empathetic, structured, flexible plan-forward outreach.

Short-term operational crisis: timeline-aware, solution-oriented engagement.

Deliberate avoidance: firm, compliance-governed, escalation-ready.

Confusion about the balance: clear, informational, friction-removing.

What this produces in practice:

Adapting tone and channel based on behavioral profile increases collections by up to 30% and reduces costs by up to 40% (ScienceSoft).

35% reduction in formal consumer complaints and 22% improvement in payment commitment rates (Deloitte 2024 Financial Services AI Outlook).

For a collections director managing regulatory exposure across multiple states, the 35% complaint reduction is a direct reduction in litigation and regulatory risk, not a customer satisfaction score.

FinanceOps Agentic AI tracks tone, hardship cues, engagement likelihood, compliance risk indicators, and payment intent in real time across every SMS, email, Voice AI, and chat interaction, adjusting every interaction automatically across every account in the portfolio simultaneously.

Capability 03: Omnichannel Continuity With No Conversation Resets.

Every channel switch in a traditional collections workflow is a reset. Every reset at the moment of payment intent is a recovery that does not happen.

The account that starts a payment negotiation over SMS and continues it via email should not have to restart the conversation from zero.

The account that switches from webchat to a phone call should arrive at the same context with the same negotiated terms.

Omnichannel strategies deliver 15 to 25% improvement in recovery rates versus single-channel approaches (Deloitte).

Native 150+ language support including Spanish, French, Arabic, and Tagalog removes the structural recovery barrier that single-language AR recovery infrastructure creates across linguistically diverse portfolios.

Capability 04: FDCPA Compliant Collections Software Governance That Is Structural, Not Manual.

The regulatory environment for collections in 2026 is more complex than at any prior point:

FCC Revoke All: consent enforcement across all lines of business (April 2026).

Colorado AI Act: extended disclosure expectations (June 2026).

Maryland medical debt legislation: expanded verification and transparency requirements.

Maine Chatbot Disclosure Act: mandatory consumer disclosure for AI deployments.

TCPA contact frequency limits, FDCPA disclosure requirements, and state-specific contact rules apply at the individual account level across every jurisdiction.

FinanceOps Agentic AI encodes every compliance constraint as a structural property of the workflow before the system touches a single account:

TCPA limits are enforced automatically at the account level.

FDCPA disclosures generated at every interaction without manual compilation.

FCCPA requirements and state-specific rules enforced with zero variance regardless of portfolio volume.

Audit-ready documentation generated automatically at every touchpoint.

The compliance team defines the rules once and the FDCPA compliant collections software executes them across every interaction without exception.

Capability 05: Affordability-Based Plans That Fix the Abandonment Problem at the Source.

Promise-to-pay abandonment rates in traditional collections operations average between 38 and 45% (Deloitte). Nearly half of every payment commitment does not result in a completed payment. The reason is almost never bad intent. It is a payment plan structured around what the account owes rather than what it can actually sustain.

FinanceOps Agentic AI evaluates each account's repayment capacity before any schedule is proposed:

Historical payment behavior and pattern data specific to that account.

Income and expense signals from transaction history.

Real-time sentiment indicators from the current interaction.

Financial stress cues that indicate what commitment the account can realistically hold.

What this produces in practice:

Promise-to-pay abandonment drops from the 38 to 45% industry average to under 20%.

Every plan that holds is an account that never ages into the mid-stage or late-stage bucket.

In a dental practice deployment managing small-balance accounts between $100 and $250, FinanceOps Agentic AI eliminated 90% of accounts past 120 days within 18 months, achieved a 70% collection success rate on targeted accounts, and reduced cost to less than $0.12 per $10 collected versus 30 to 40% in third-party agency fees. Net annual revenue recovered totalled $133,260 with annual savings of $40,440 versus traditional agency costs.

Capability 06: Invoice Automation That Closes the Intent-to-Payment Gap.

The gap between a customer's intent to pay and a completed payment is almost entirely an infrastructure problem. It is where most AR recovery is lost before it is ever counted. Every manual step in the invoice workflow is a point of failure. Every point of failure is an account that ages further and costs more to recover. FinanceOps Agentic AI closes that gap entirely:

Invoice issuance at the right time to the right contact.

Behavioral reminders triggered by engagement data, not a calendar.

Failed payment retry logic at optimized intervals based on account signals.

Automatic reconciliation at the point of payment without manual intervention.

Dispute routing to the right resolution workflow without agent queues.

Audit-ready documentation at every touchpoint without manual compilation.

How Does FinanceOps Agentic AI Compare Head-to-Head?

Capability | FinanceOps Agentic AI | HighRadius | Stripe | Adyen | Braintree |

Early-stage delinquency recovery | Purpose-built, day one | Not designed for | Not designed for | Not designed for | Not designed for |

Account-level behavioral intelligence | Full, real-time, per account | Portfolio-level ML only | None | None | None |

Live sentiment analysis | Real-time, all channels | None | None | None | None |

Omnichannel context continuity | Full, zero resets | None | Dunning emails only | None | None |

FDCPA compliant collections software | Structural, per account | Not applicable | Not applicable | Not applicable | Not applicable |

Affordability-based payment plans | Dynamic, per account | None | None | None | None |

PTP abandonment reduction | From 38 to 45% to under 20% | Not applicable | Not applicable | Not applicable | Not applicable |

Multilingual outreach | 150+ languages | None | None | None | None |

Pricing model | 1.5% of collections recovered | Subscription | Subscription | Subscription | Subscription |

Recovery rate | Up to 70% | DSO reduction only | Dunning only | Not applicable | Not applicable |

Cost per recovery reduction | 98.5% vs traditional | Processing cost only | Not applicable | Not applicable | Not applicable |

Right-party contact rate | 12 to 15% vs 2% norm | Not applicable | Not applicable | Not applicable | Not applicable |

Compliance audit documentation | Automated, every touchpoint | Manual | Manual | Manual | Manual |

Key Takeaways for Collections Leaders

Takeaway 01: Payment optimization and payment recovery are fundamentally different infrastructure problems.

The platform that processes authorized payments is not designed to function as an AI payment recovery platform for accounts that have stopped paying.

When organizations apply payment optimization tools to delinquency recovery, the aging bucket expands, late-stage accounts increase, and cost per recovery rises.

This misalignment shows up directly in DSO and bad debt and it will not be solved by improving cash application accuracy.

Takeaway 02: Contact timing is the single most important variable in early stage delinquency recovery performance.

Collections success drops from approximately 65% within 24 hours to 15% after 14 days. This is the Recovery Decay Curve and it does not decline gradually. It accelerates.

Every day of delay reduces recovery probability in a way that downstream effort from any collections automation platform cannot offset.

The real evaluation question is not which platform has more features but which system was built to act on behavioral signals immediately, inside the Delinquency Compression Window, rather than follow fixed schedules.

Takeaway 03: The current delinquency environment makes AR recovery infrastructure decisions higher-stakes than at any prior point.

Credit card delinquency transition rates at 8.2%, total household debt at $18.4 trillion, and 44% of US B2B invoices overdue. The recovery environment is tightening every quarter.

The B2B collections AI and delinquency recovery software market is growing at 16.9% CAGR because the problem is growing at a proportional rate.

52% of collected dollars still come from the first 90 days. Teams equipped with early stage delinquency recovery infrastructure built to act inside that window will capture the majority of recoverable revenue, while those relying on delayed, schedule-based systems will continue to write it off.

The conclusion: This is not a projection. It is already reflected in current data. AR teams that deploy a purpose-built AI payment recovery platform will recover the majority of what is recoverable. AR teams running fixed-schedule outreach from platforms built for a different problem will write it off.

Ready to See What Early-Stage Precision Recovers in Your Portfolio?

Book a free 20-minute demo with FinanceOps Agentic AI. No pitch deck. No generic demonstration. Your aging bucket, your DSO trend, your bad debt exposure, mapped against what behavioral intelligence, sentiment-aware outreach, and governed compliance automation actually produce in your specific portfolio. Your accounts. Your numbers. Your recoverable value.

FAQs

We use HighRadius for cash applications. Why do we need a separate AI payment recovery platform?

HighRadius is designed to automate cash application, reconciliation, and workflows for accounts that are already paying. That is the problem it was built to solve, and it solves it well. FinanceOps Agentic AI is built for accounts that have stopped paying. These are distinct problems requiring different infrastructure. Organizations with both active payment flows and growing delinquency need systems for each. Using a reconciliation platform as delinquency recovery software is a structural mismatch that leads to poor recovery outcomes regardless of how well the underlying technology performs.

We already have a dunning sequence. Why is that not enough?

A dunning sequence is a reminder system, not an AI payment recovery platform. It operates on fixed timelines rather than real-time behavioral signals, does not analyze payment behavior, and cannot distinguish between hardship and avoidance. It also lacks dynamic payment plan calibration and embedded FDCPA compliant collections software governance. FinanceOps Agentic AI acts at day one, adapts outreach based on behavior and sentiment, maintains full context across channels, and enforces regulatory compliance structurally as a built-in property of every workflow. The difference between the two shows up directly in the monthly aging report.

How does FinanceOps Agentic AI handle TCPA and FDCPA compliance across multiple states?

FinanceOps Agentic AI encodes all compliance requirements, including TCPA, FDCPA, FCCPA, and state-specific rules, directly into the workflow before any account is contacted. Compliance teams define the rules and the FDCPA compliant collections software executes within them consistently across the entire portfolio. Every interaction is logged with audit-ready documentation generated automatically at every touchpoint. With the FCC's Revoke All consent enforcement now in effect, manual compliance tracking across a high-volume delinquent portfolio carries regulatory exposure that scales with every account added. Structural compliance governance built into the AR recovery infrastructure eliminates that scaling risk entirely.

What does 1.5% of collections mean for a $10M delinquent portfolio?

FinanceOps Agentic AI operates on a performance-based model, charging 1.5% of recovered revenue. There are no upfront fees and no fixed costs. Recovering $2 million from a $10 million delinquent portfolio results in a $30,000 fee. Recovering nothing results in a zero fee. This structure directly aligns vendor incentives with recovery outcomes. For an AR director evaluating which collections automation platform has genuine accountability for results, this pricing model is the clearest possible signal of which vendor has actual financial stake in the outcome.

Our experienced collections agents outperform generic outreach. Why would a B2B collections AI be better?

Experienced agents do outperform generic workflows. That is correct and not in dispute. The question is whether your best agents can personally engage every account in your portfolio at the optimal moment, through the optimal channel, with the right tone and a payment plan calibrated to that specific account's capacity, while maintaining perfect FDCPA compliant collections software governance across all interactions, 24 hours a day, 7 days a week, simultaneously across every account in the portfolio. At scale, they cannot. FinanceOps Agentic AI extends that level of decision-making across the entire portfolio in real time. The objective is not to replace human judgment but to deploy it consistently across all accounts, including the accounts that would otherwise be missed during the Delinquency Compression Window, using AR recovery infrastructure built specifically for that purpose.

6 minutes

Posted by

Arpita Mahato

Content Writer

Other Blogs

View other blogs

Stay Updated with Us

Enter your email below and subscribe to our weekly newsletter