Why Most AI Payment Platforms Cannot Solve Your Collections Problem

FinanceOps Agentic AI is the only AI payment facilitator built on Recovery Architecture. Every other platform your member servicing team is evaluating was built on Processing Architecture. That single distinction determines whether your delinquency portfolio is recoverable or written off.

Here is what it costs in practice.

Your member servicing team is running a platform processing tens of millions in authorized payments every month with near-perfect efficiency. Authorization rates are up. Payment posting is automated. And your 30 to 60 DPD delinquency balance has grown for the third consecutive quarter.

Those two facts are not a contradiction. They are the expected output of applying a Processing Architecture platform to a Recovery Architecture problem. The platform is working exactly as designed. It was designed for a different problem.

This is what most credit union operations teams miss. They compare features. They negotiate pricing. They request references. They never ask the one question that determines whether any of it matters: was this platform built to optimize authorized payment flows, or was it built to restore member accounts where payment authorization has stopped?

Those are not the same problem. No amount of dunning modules, AI add-ons, or core system integrations will close the architectural gap between them. Understanding that gap is worth more to your member servicing operation than any feature comparison you will run in 2026.

TL;DR

Processing Architecture platforms optimize the movement of authorized payments. Stripe, Adyen, HighRadius, and Braintree are Processing Architecture platforms. They are excellent at the problem they were built to solve.

Using a Processing Architecture platform against a delinquency recovery problem produces structurally guaranteed underperformance. The platform cannot read behavioral signals of delinquent accounts, cannot adjust outreach tone in real time, and cannot enforce FDCPA and TCPA compliance automatically at the individual account level. These are not missing features. They are outside the architectural scope entirely.

FinanceOps Agentic AI is the only purpose-built Recovery Architecture platform in the market. It charges 1.5% of recoveries with no upfront cost and no fee if no recoveries occur. That pricing model is the structural proof of Recovery Architecture.

The Problem Your Current Platform Cannot See

Your member servicing team ran 1,200 outreach attempts last month. Right-party contact rate: 11%. Of the contacts made, 44% resulted in a promise to pay. Of those promises, 41% were abandoned before a completed payment. DSO moved up again. The aging report shows the 30 to 60 DPD bucket growing for the third consecutive quarter.

This is not a team that is failing. This is a team working correctly inside infrastructure designed for a fundamentally different problem.

The platform your credit union is paying a subscription fee for was built to optimize the mechanics of moving authorized payments. It was trained on authorized payment behavior. It improves authorization rates, reduces processing costs, and accelerates reconciliation. It was not trained on delinquency behavioral signals, hardship indicators, or avoidance patterns. It has no model for what a member account communicates when it goes dark.

For credit unions, the stakes carry a dimension that commercial lenders do not face at the same intensity. A delinquent auto loan member is also a checking account holder, a potential mortgage borrower, and a community relationship that took years to build. A member handled with empathy and flexibility during a financial hardship can remain a member in good standing for decades. A member who receives tone-deaf automated dunning during that same hardship closes their accounts when they recover.

Processing Architecture has no model for that dimension of the servicing problem. Recovery Architecture is built around it.

What Separates Processing from Recovery Architecture?

The difference comes down to one design assumption baked into every ML model, every workflow, and every line of code in the platform.

Processing Architecture assumes the member intends to pay. The system's job is to make payment mechanics frictionless. Intelligence operates at the portfolio level. Member intent is treated as a given.

Recovery Architecture assumes something broke. The member has stopped paying and the system's job is to determine exactly why, for this specific account, and re-engage them at the exact moment, through the exact channel, with the exact tone most likely to produce a payment commitment while preserving the member relationship.

One sentence separates them: Processing Architecture optimizes for payment mechanics. Recovery Architecture optimizes for payment intent.

That distinction is not semantic. It determines what the platform trains its models on, what data it collects at the account level, what compliance infrastructure it encodes structurally, and what its pricing model is accountable to. Every capability difference that follows is architectural, not cosmetic.

The Delinquency Compression Window: FinanceOps Agentic AI defines the period between day one of a missed payment and day 14 as the Delinquency Compression Window. This is the stage where recovery probability compresses from 65% at 24 hours to 15% at 14 days, based on ACA International data on US debt collection timing. The compression is not linear. It accelerates. Every platform decision should be evaluated against one criterion: was this platform built to act inside the Delinquency Compression Window, or was it built to manage accounts that have already aged past it?

What Was Processing Architecture Built For?

Before explaining why Processing Architecture fails collections teams, it is worth being precise about what it was actually built to accomplish. It was built to solve a genuinely hard problem and it solved it well.

Large organizations in the early 2010s were losing significant margin to payment friction. Poorly optimized interchange fees. Manual cash application. Authorization rates below where they should have been. For organizations processing hundreds of millions of dollars annually, each inefficiency represented measurable financial loss.

Stripe made developer payment infrastructure accessible to businesses that previously needed an engineering team to accept a card payment online. Adyen built direct card network connections that reduced processing costs at enterprise scale. HighRadius automated cash application and AR reconciliation for complex ERP environments. Braintree delivered native PayPal wallet integration where wallet access was a decisive conversion factor.

Every ML model across each of these platforms was trained on the same signal: authorized payment behavior. What does a legitimate transaction look like? When do authorization rates peak? What reconciliation patterns reduce manual overhead?

These are valuable questions. The answers produced real financial outcomes for organizations whose primary challenge was payment optimization.

The design assumption baked into every Processing Architecture platform is this: the member intends to pay and the system's job is to make payment mechanics frictionless. That assumption is correct for a performing loan portfolio. It is precisely wrong for every delinquent account in a member servicing queue, where the account stopped paying because something changed: income disruption, medical hardship, a billing dispute, a deliberate decision to prioritize other obligations, or a breakdown in communication that went unresolved.

Processing Architecture has no model for any of those scenarios. That is not a failure of these platforms. It is an accurate description of their scope.

Why Recovery Architecture Needs Different Infrastructure

The gap between Processing and Recovery Architecture cannot be closed by adding features to an existing platform. Each layer requires infrastructure built from the ground up for a different problem.

Account-Level Intelligence vs Portfolio-Level ML.

Processing Architecture improves authorization rates across cohorts. Its intelligence layer operates on aggregate behavior across a population of accounts to optimize overall payment success rates.

Recovery Architecture analyzes each specific member account's payment history, behavioral patterns, device usage, channel responsiveness, and real-time engagement data before a single contact attempt is made. A member who opened the payment portal four times this week and did not complete a transaction is communicating specific intent. A Processing Architecture platform cannot read that signal. It was not trained to.

This is not a data access problem. It is a model architecture problem. The ML models in Processing Architecture platforms were trained on authorized payment behavior with an objective function targeting authorization success. Reorienting those models toward delinquency behavioral signals would not update a feature. It would require rebuilding the model from a different training dataset with a different objective function entirely.

Sentiment Detection vs Reminder Scheduling.

Recovery Architecture delivers skilled member servicing judgment at scale: 24 hours a day, across thousands of accounts simultaneously, with real-time tone adjustment based on what each specific account is communicating. According to Deloitte's 2024 Financial Services AI Outlook, sentiment-aware AI reduces formal consumer complaints by up to 35% and improves payment commitment rates by 22%.

Processing Architecture schedules reminders. It cannot distinguish between a member showing genuine financial hardship who needs empathetic payment restructuring and a member showing deliberate avoidance who needs firm, escalation-ready outreach. Both receive the same day-30 notification because the platform has no model for the difference. In a credit union context, that indiscriminate treatment carries relationship costs that show up not on this quarter's delinquency report but on next year's member retention report.

Structural Compliance vs Manual Tracking.

FCC Revoke All consent enforcement took effect April 2026, applying consent revocation across all lines of business. Colorado's AI Act extended disclosure expectations as of June 2026. TCPA contact frequency limits, FDCPA disclosure requirements, NCUA examination standards, and state-specific contact rules apply at the individual member account level simultaneously across the entire servicing portfolio.

Recovery Architecture encodes every compliance constraint as a structural workflow property before the system contacts a single member. Compliance is not a checklist the system runs through. It is the foundation the system is built on.

Adding a compliance module to a Processing Architecture platform produces a checklist on top of infrastructure built for a different regulatory environment. The module tracks. The architecture governs. The difference becomes visible the moment portfolio volume scales or a new NCUA examination cycle begins.

Performance-Aligned Pricing vs Subscription Decoupling.

This is the structural difference most commonly overlooked in platform evaluations and the one that reveals vendor incentives most clearly.

Processing Architecture platforms charge subscription fees regardless of whether member servicing performance improves. The vendor's revenue is not connected to your delinquency rate trend, your charge-off ratio, or your member retention outcomes. That institutional reality produces platforms oriented toward renewal, not recovery.

FinanceOps Agentic AI charges 1.5% of recoveries. If no recoveries occur, the fee is zero. Every dollar of FinanceOps Agentic AI revenue is produced by a dollar of member account restoration. That alignment is the structural proof of Recovery Architecture expressed as a financial commitment made before touching a single account.

The Recovery Decay Curve: FinanceOps Agentic AI identifies the structured collapse of recovery probability over time as the Recovery Decay Curve. Contact a missed payment within 24 hours and recovery probability is 65%. Wait three days and it drops to 45%. Wait seven days and it drops to 30%. Wait 14 days and it drops to 15%, below the economically viable threshold for most portfolio segments, based on ACA International data. The curve does not decline linearly. It accelerates. The first 24 hours represent the highest-value recovery window in the entire delinquency lifecycle. Any platform not architecturally designed to act within the first 24 hours is a platform optimized for the wrong stage.

Why Adding a Module Does Not Fix the Architecture

The most common objection goes like this: "Our current platform has a member servicing module. Why is that not enough?" It is a fair question. Here is the direct answer.

A servicing module added to a Processing Architecture platform is a notification sequence layered on top of infrastructure built to move authorized payments. The module schedules reminders. It cannot read behavioral signals. It sends day-30 outreach on a fixed schedule. It cannot act on day one when recovery probability is 65% rather than 15%. It logs compliance rules in a tracking system. It cannot enforce them structurally at the individual account level before first contact.

The analogy is precise: adding a GPS navigation app to a vehicle designed for paved roads does not make that vehicle capable of off-road recovery. The app adds navigation. It does not change the vehicle's fundamental engineering constraints.

Structural Incapability 01: No Behavioral Intelligence at the Account Level.

A member who opened the payment portal eight times this week and did not complete a payment is communicating specific intent. A notification sequence sends the same day-seven reminder regardless. The module does not have access to that signal because the platform was never designed to collect and model it at the individual account level. This is a model architecture problem, not a data access problem.

Structural Incapability 02: No Real-Time Tone and Compliance Adjustment.

According to PwC's analysis of AI-powered contact precision in financial services, AI-driven behavioral targeting reduces average contact attempts per resolution by 40%. That reduction requires knowing what the account is signaling in real time, not what a delinquency cohort does in aggregate. Processing Architecture platforms process transactions. They do not conduct member servicing conversations and cannot adjust those conversations based on what the individual member is communicating mid-interaction.

Structural Incapability 03: No Performance-Aligned Accountability.

A subscription fee vendor has no financial stake in whether your delinquency rate improves. Feature development is oriented toward renewal. Support prioritizes implementation completion over recovery performance. The platform roadmap reflects the median subscriber, not your specific member servicing challenges. The module is not the problem. The architecture underneath it is.

Six Recovery Architecture Capabilities in Production

Recovery Architecture is not a positioning statement. It is a specific set of technical capabilities that either exist in a platform or do not. Each capability below directly addresses one of the three structural incapabilities identified in Section 5. The architecture argument above is theoretical. This section is where it becomes operational.

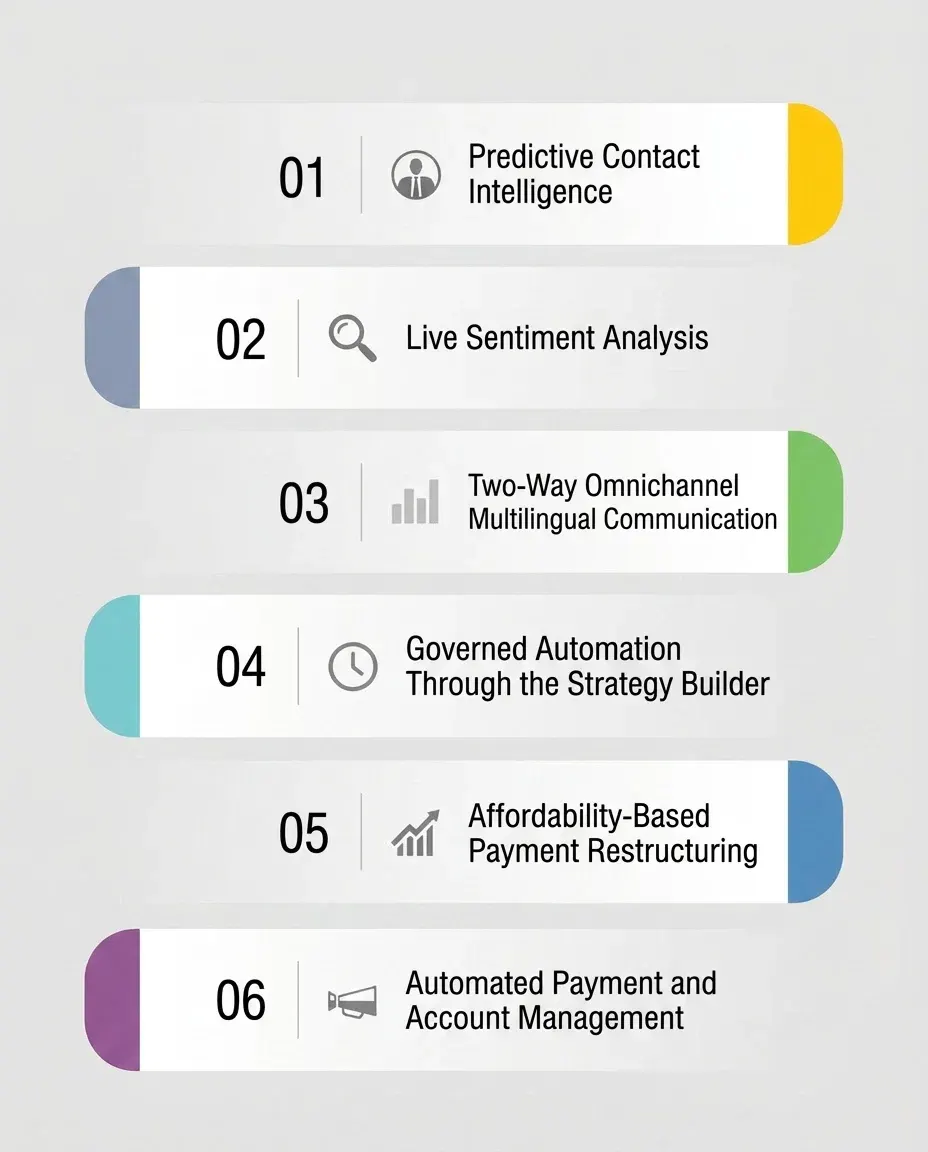

Image: Six Recovery Capabilities of FinanceOps Agentic AI

Capability 01: Predictive Contact Intelligence.

The structural incapability it addresses: no behavioral intelligence at the account level.

Before FinanceOps Agentic AI makes a single contact attempt, the system has already made three account-level decisions that a Processing Architecture platform is architecturally incapable of making.

It has determined the optimal time to contact this specific member, based on their historical interaction patterns and real-time behavioral signals. It has determined the optimal channel, whether SMS, email, Voice AI, webchat, or portal, based on that member's responsiveness history and compliance constraints. And it has determined the correct contact point, the true decision-maker for this account, using relational data and past resolution outcomes.

The output is an account-level decision made before the first word of outreach is written. Contact rates improve from the 2% industry norm to 12 to 15%. According to PwC, AI-driven behavioral targeting reduces average contact attempts per resolution by 40%. Fewer contact attempts producing higher resolution rates means lower operational cost and lower member friction simultaneously. That combination is structurally impossible on a fixed outreach schedule.

Capability 02: Live Sentiment Analysis.

The structural incapability it addresses: no real-time tone and compliance adjustment.

A skilled member servicing specialist can distinguish genuine financial distress from deliberate payment avoidance. They adjust tone, urgency, and offer structure accordingly. The problem is that no servicing team can deploy that judgment across thousands of member accounts simultaneously, 24 hours a day, without variance. FinanceOps Agentic AI does.

Across every SMS, email, Voice AI, and chat interaction, the system evaluates emotional state and payment behavior in real time, tracking tone, hardship cues, engagement likelihood, compliance risk indicators, and payment intent simultaneously. The system adjusts every dimension of the interaction immediately and automatically.

Members showing genuine financial stress receive affordability-forward framing and restructuring calibrated to what they can sustain. Members showing deliberate avoidance receive firm, compliance-governed, escalation-ready outreach. Members showing confusion receive clear, friction-removing responses. No staff intervention required. No lag between signal and response.

According to Deloitte's 2024 Financial Services AI Outlook, sentiment-aware AI reduces formal consumer complaints by up to 35% and improves payment commitment rates by 22%. For a credit union managing NCUA examination standards, the 35% complaint reduction is a direct reduction in litigation risk and examination findings. It is not a member satisfaction metric.

Capability 03: Two-Way Omnichannel Multilingual Communication.

The structural incapability it addresses: no real-time continuity across channel switches.

Every channel switch in a traditional member servicing workflow is a conversation reset. The member who started negotiating a payment plan over SMS and called in three days later has to restart from the beginning. Context is lost. Negotiated terms are lost. At the exact moment of highest payment intent, the platform introduced friction that converted a willing payer into a delayed resolution. That conversion happens silently, at scale, every day on Processing Architecture infrastructure.

FinanceOps Agentic AI maintains full context across SMS, email, Voice AI, webchat, and self-service portals across every channel switch without exception. No context resets. No repeated questions. No lost negotiation history. A member who starts a restructuring conversation over text and continues via phone arrives at the same conversation with the same negotiated terms.

Native multilingual capability across Spanish, French, Arabic, Tagalog, and 150+ additional languages removes the structural recovery barrier that single-language outreach creates across a linguistically diverse membership base. According to Deloitte, omnichannel strategies deliver 15 to 25% improvement in recovery rates versus single-channel approaches. Language access is not a member experience enhancement. It is a structural prerequisite for reaching the full delinquent member portfolio at all.

Capability 04: Governed Automation Through the Strategy Builder.

The structural incapability it addresses: no performance-aligned accountability at the workflow level.

The most consistent concern credit union operations teams raise about AI-driven servicing is this: if the system is making contact decisions autonomously, who is accountable for what it says, when it says it, and whether it complies with FDCPA, TCPA, and NCUA requirements at the individual account level?

The answer is the Strategy Builder. Before FinanceOps Agentic AI contacts a single member account, the servicing team configures every operational parameter: tone rules, contact cadence, retry logic, segmentation by risk band and delinquency stage, escalation workflows, negotiation guardrails, and compliance limits including TCPA, FDCPA, NCUA examination standards, and state-specific contact rules.

The platform executes within those parameters with complete consistency and zero variance at scale. The servicing team defines the strategy. FinanceOps Agentic AI executes it. The most concrete evidence of what this produces: in the LA Federal Credit Union deployment, only 6 cases required human specialist review across 1,650 payments processed in the first 21 days. That is not a feature benefit. It is the operational output of a system whose boundaries were correctly defined before it touched a single account.

Capability 05: Affordability-Based Payment Restructuring.

The structural incapability it addresses: no account-level intelligence for repayment capacity.

According to Deloitte, promise-to-pay abandonment rates in traditional collections operations average between 38 and 45%. Nearly half of every payment commitment does not result in a completed payment. The most common cause is not bad intent. It is a payment plan structured around what the account owes rather than what the account can actually sustain.

A plan proposed without evaluating repayment capacity will fail regardless of how sincerely the member committed to it. When it fails, the account rolls forward into a delinquency stage where recovery rates are lower, cost per resolution is higher, and the member relationship has absorbed one more negative interaction with the institution.

FinanceOps Agentic AI evaluates repayment capacity from payment behavior history, income and expense signals, real-time sentiment indicators, and transaction pattern data before any restructured schedule is proposed. The output is a plan calibrated to what this specific member can actually hold. PTP abandonment drops from the 38 to 45% industry average to under 20%. Every plan that holds is a member account that never ages into the late-stage delinquency bucket.

Capability 06: Automated Payment and Account Management.

The structural incapability it addresses: the infrastructure gap between payment intent and completed payment.

The gap between a member's intent to pay and a completed payment is almost entirely an infrastructure problem. Every manual step in the payment management workflow is a point of failure. Every point of failure is a member account that ages further and costs more to restore.

FinanceOps Agentic AI automates the complete payment lifecycle without manual intervention at any step. Payment reminders are triggered by engagement behavior, not a fixed calendar. Failed payment retry logic operates at optimized intervals based on account-level signals, not uniform timing. Reconciliation occurs automatically at the point of payment. Disputes are routed to the correct resolution workflow without staff queues. Audit-ready documentation is generated automatically at every touchpoint for NCUA examination readiness.

The result is that a member who intends to pay actually completes the payment. The infrastructure friction converting willing payers into aging delinquencies is eliminated entirely. Staff time previously consumed by routine follow-up, failed retry management, and manual reconciliation is freed for the complex member relationship cases that genuinely require human judgment.

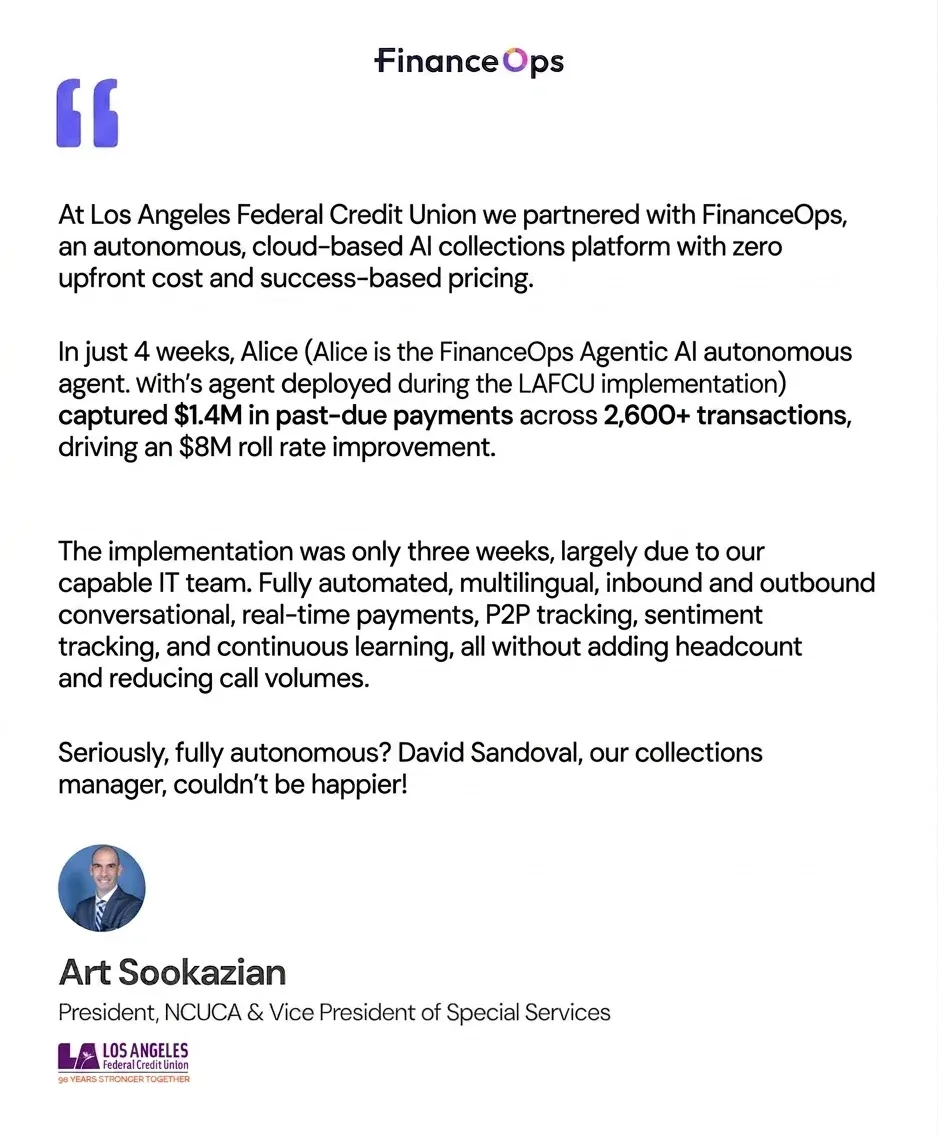

Proven Results: Los Angeles Federal Credit Union.

In four weeks, FinanceOps Agentic AI captured $1.4M in past-due payments across 2,600+ member transactions at LA Federal Credit Union, driving an $8M roll rate improvement. Implementation took three weeks. Staff effort required was under 10 minutes per day from day one. Call volumes fell. No headcount was added at any point.

What FinanceOps Agentic AI Autopilot Costs

Start for free. Pay only if recoveries occur. No credit card required. No subscription. No upfront cost. No fee if recoveries do not occur.

Autopilot: 1.5% of Recoveries.

Built for credit union member servicing teams operating without a dedicated in-house collections unit. FinanceOps Agentic AI covers the full costs of the platform and outreach. You pay only for results delivered.

Core Operations Included:

Payment management and processing.

Skip tracing.

Payouts.

Resolution center.

Strategy builder.

Payment reconciliation.

Reporting and analytics.

Core system integrations including Symitar and Temenos.

AI-Based Features Included:

Best time to contact per individual member account.

Member characteristics profiling.

Live sentiment analysis across all channels.

Cash flow forecasting.

Ease of collectability scoring.

Demographic analysis.

Preferred mode of communication identification per member account.

Why Autopilot Pricing Matters More Than Any Feature Comparison.

Every other AI payment facilitator charges subscription fees regardless of whether your member servicing team recovers revenue. The fee is the same whether your delinquency ratio improves or compounds, whether your charge-off rate falls or rises.

FinanceOps Agentic AI charges 1.5% of what it actually recovers. If FinanceOps Agentic AI recovers $800,000 from your delinquent member portfolio, the fee is $12,000 and the net recovery is $788,000. If no recoveries occur, the fee is zero and FinanceOps Agentic AI absorbs all platform and outreach costs entirely.

The Autopilot pricing model is the structural proof of Recovery Architecture. A vendor that charges regardless of recovery has no architectural reason to optimize for recovery. A vendor that charges 1.5% of what it recovers has every institutional reason to.

Head-to-Head: The Two Architectures Compared

Processing Architecture metrics reflect industry norms across credit union, healthcare accounts receivables, and B2B collections portfolios. Recovery Architecture metrics reflect FinanceOps Agentic AI deployment data. Individual results vary by portfolio size, delinquency composition, and membership base characteristics.

Processing Architecture vs Recovery Architecture: Named

This section names platforms explicitly and categorizes them within the two-architecture framework based on what each platform was designed to do, not on what its marketing materials claim.

Processing Architecture Platforms.

Stripe: Excellent at developer-first payment processing and subscription billing. Processing Architecture because its ML models optimize authorized transaction throughput, its dunning module is a notification sequence for failed subscription payments, and it has no account-level behavioral intelligence for member accounts that have stopped paying.

Adyen: Excellent at enterprise global payment optimization and interchange cost reduction at scale. Processing Architecture because its intelligence layer operates at the portfolio level to optimize authorized payment flows and it has no FDCPA, TCPA, or NCUA compliance enforcement at the individual account level.

HighRadius: Excellent at enterprise AR automation, cash application, and ERP integration. Processing Architecture because its design assumption is unified ERP data and active payment workflows, and it has no architecture for restoring member accounts where payment authorization has stopped.

Braintree: Excellent at consumer-facing payment acceptance with native PayPal and Venmo integration. Processing Architecture because its intelligence layer is oriented toward authorized consumer transactions and it has no delinquency recovery capability beyond basic failed payment retry.

Square: Excellent at accessible payment acceptance for small and mid-sized businesses. Processing Architecture because it was built for customers who have decided to pay and its invoice reminder functionality is a notification tool, not a recovery system.

Chargebee: Excellent at subscription billing orchestration for SaaS companies. Processing Architecture because it is an orchestration layer on top of existing payment gateways, not a member servicing system, and its dunning workflows address subscription billing failures rather than delinquent account recovery.

None of these platforms are inadequate. They are excellent at exactly what they were designed to do. The problem is not the platforms. The problem is applying them to a member servicing challenge they were not designed for and expecting Recovery Architecture performance from Processing Architecture infrastructure.

Recovery Architecture Platforms.

FinanceOps Agentic AI: The only purpose-built Recovery Architecture platform in the market. Account-level behavioral intelligence for delinquent member accounts. Real-time sentiment analysis across all channels. Structural FDCPA, TCPA, and NCUA compliance governance. Affordability-based payment restructuring that reduces PTP abandonment from 38 to 45% to under 20%. 150+ language support natively. The only AI payment facilitator that charges 1.5% of recoveries with no upfront cost and no fee if no recoveries occur.

Why This Is the Highest-Stakes Platform Choice in 2026

The delinquency environment your member servicing infrastructure is operating in right now leaves no room for the wrong platform.

Credit card delinquency transition rates have reached 8.2%, the highest since 2011, according to the Federal Reserve Board. Total US household debt stands at $18.4 trillion, according to the New York Fed's Q1 2025 Household Debt and Credit Report. 44% of US B2B invoices are currently overdue. The AI for debt collection market is growing from $3.34 billion in 2024 toward $15.9 billion by 2034 at a 16.9% compound annual growth rate.

For credit unions, the pressure is compounded by a structural reality commercial lenders do not face at the same intensity. Credit unions operate under NCUA examination standards that evaluate not just delinquency ratios but the quality of member servicing practices. A charge-off is a balance sheet event. A member charged off after receiving automated, tone-deaf outreach during genuine financial hardship is a reputational event, a community event, and in some examination cycles, a supervisory event.

What the Wrong Architecture Costs Every Quarter.

Member servicing teams using Processing Architecture enter every quarter with accounts at day 30 that were contactable at day one and were not contacted. The Recovery Decay Curve has already compressed recovery probability from 65% to below 20%, based on ACA International data. Accounts that roll to 90 DPD cost three to four times more per account to resolve than they would have at day one. Accounts that age past 180 days have an 11% recovery rate, according to CFPB data on late-stage delinquency recovery. Each of those accounts represents not just a charge-off but a member relationship that is almost certainly lost, along with all future balance sheet value that relationship would have produced.

What the Right Architecture Produces Every Quarter.

Member servicing teams using Recovery Architecture activate at day one based on behavioral signals, adjust outreach tone in real time to match what each account is communicating, and enforce full compliance automatically across every interaction. Cost per recovery is $3.65 instead of $50 to $150. Staff effort is under 10 minutes per day instead of full servicing capacity. Member accounts that would have become charge-offs become accounts restored to good standing. Members treated with dignity during financial hardship tend to deepen their relationship with the institution rather than exit it.

By the end of 2026, the gap between these two trajectories will be visible in every metric that matters to credit union leadership: delinquency ratio, charge-off rate, cost to serve, member retention rate, and NCUA examination outcomes. The architecture decision determines which trajectory your member servicing operation is on.

Key Takeaways

Takeaway 01: Architecture Determines Outcome, Not Features. The first evaluation question is not which platform has more capabilities. It is whether the platform was built to optimize authorized payment flows or to restore member accounts where payment has stopped. Those are different architectures and only one of them solves your problem.

Takeaway 02: The Recovery Decay Curve Is the Most Critical Data Point. Contact at 24 hours produces a 65% recovery probability. Contact at 14 days produces 15%. A platform activating at day 30 is not a slower version of one activating at day one. It is a platform operating on accounts that have already lost most of their recoverable value.

Takeaway 03: Pricing Is the Structural Test of Vendor Accountability. A vendor paid on subscription regardless of whether your delinquency ratio improves has no financial stake in your outcome. FinanceOps Agentic AI charges 1.5% of recoveries with no fee if no recoveries occur, which means every dollar of its revenue is produced by a dollar of member account restoration.

Ready to See What Recovery Architecture Delivers?

Start free. No credit card required. Pay only on recoveries.

Book a free 20-minute demo with FinanceOps Agentic AI. No pitch deck. No generic demonstration. Your delinquency ratio, your charge-off trend, your aging bucket distribution, mapped against what behavioral intelligence, sentiment-aware outreach, and governed compliance automation actually produce in your specific loan portfolio. Your members. Your numbers. Your recoverable value.

FAQs

Our Platform Has a Servicing Module. Why Is That Not Enough?

A module and an architecture are not the same thing. A servicing module on a Processing Architecture platform is a notification sequence layered on top of infrastructure built for authorized payments. It schedules reminders on a fixed cadence. It cannot read behavioral signals, distinguish hardship from avoidance, enforce FDCPA and NCUA compliance structurally before first contact, or propose payment plans calibrated to actual member repayment capacity. Those capabilities require a different underlying architecture entirely, not an additional layer on top of the existing one.

What Is the Delinquency Compression Window?

It is the period between day one of a missed payment and day 14, where recovery probability compresses from 65% at 24 hours to 15% at 14 days, based on ACA International data. The compression accelerates rather than declining gradually. Any platform that contacts delinquent accounts at day 30 on a fixed schedule is operating on accounts that have already lost approximately 80% of their recovery probability. For credit unions, that delay also means 30 days during which a member experiencing genuine hardship received no contact and no restructuring option from their institution.

Can Stripe or HighRadius Build Toward Recovery Architecture?

The barriers are architectural rather than developmental. Reorienting ML models trained on authorized payment behavior toward delinquency behavioral signals requires a different dataset, a different objective function, and a different model architecture entirely. Building structural FDCPA, TCPA, and NCUA compliance governance into a platform designed for payment authorization security is a rebuild of core workflow logic, not a module addition. Shifting from subscription pricing to performance-aligned pricing requires absorbing platform and outreach costs against a recovery outcome the vendor cannot fully control. Each of those is a platform rebuild, not a feature release.

How Does Autopilot Pricing Work in Practice?

Autopilot charges 1.5% of recoveries with no subscription, no upfront cost, and no credit card required. If FinanceOps Agentic AI recovers $800,000 from your delinquent member portfolio, the fee is $12,000 and the net recovery is $788,000. If no recoveries occur, the fee is zero and FinanceOps Agentic AI absorbs all platform and outreach costs. Every other AI payment facilitator charges regardless of whether your delinquency ratio improves. That structural difference produces different platforms, different development priorities, and categorically different levels of vendor accountability.

How Does FinanceOps Agentic AI Enforce FDCPA, TCPA, and NCUA Compliance?

Every compliance constraint, including TCPA contact frequency limits, FDCPA disclosure requirements, NCUA examination standards, and state-specific contact rules, is encoded as a structural workflow property in the Strategy Builder before the system contacts any member account. Required disclosures are generated automatically at every interaction. Contact limits are enforced at the individual account level without manual tracking. Audit-ready documentation is produced at every touchpoint automatically. With FCC Revoke All consent enforcement in effect since April 2026, manual compliance tracking carries regulatory exposure that scales with every account added to the portfolio. Structural governance encoded before first contact eliminates that scaling risk entirely.