Blog Summary

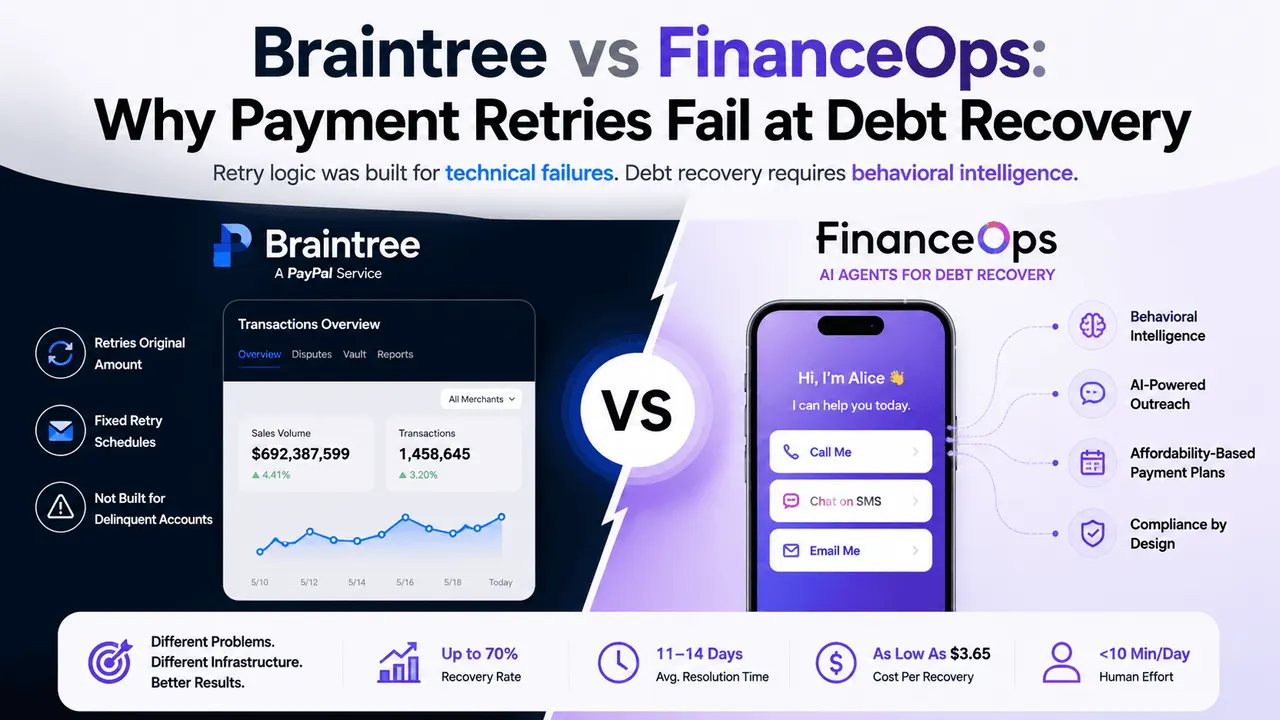

Braintree is a world-class payment processor. It was designed by PayPal's engineering team to move authorized payments from customers who have already decided to pay. Its retry architecture handles technical failures (an expired card, a temporary bank hold, a declined authorization) and it handles them well.

It was not designed for what collections and receivables teams are actually facing in 2026: delinquent consumer accounts where the customer has stopped paying, the barrier is behavioral or financial, and a retry schedule does nothing except age the balance closer to charge-off.

FinanceOps Agentic AI was built specifically for that problem. It operates with account-level behavioral intelligence, real-time sentiment analysis, Skip-A-Pay, and affordability-calibrated payment plans at 1.5% of collections recovered, with zero upfront cost and zero fee if no recovery occurs.

The collections and receivables teams reading this blog are inside businesses where Braintree's retry settings have already been optimized, the dunning emails are already configured, and the aging report still shows the same structural problem every quarter. That problem is not a configuration issue. It is an architecture issue. This blog explains the five structural gaps between what Braintree offers and what delinquent account recovery actually requires, and why the distinction matters more in 2026 than it ever has before.

What Braintree Was Actually Built to Do

Braintree is PayPal's developer-focused payment gateway, built to solve one specific problem: make authorized consumer payments as frictionless as possible for platforms where PayPal and Venmo wallet access is a meaningful conversion factor.

Its core architectural assumption is the same as every payment processor in the market. The customer has decided to pay. The system's job is to execute that decision reliably and securely. Every capability Braintree has built, Advanced Fraud Tools, recurring billing, retry logic, and its developer API, was engineered to serve customers who are trying to pay and encountering technical obstacles.

That assumption is the key to understanding why Braintree fails at debt recovery. Its retry logic was designed to answer one question: when is the most likely moment this technical failure will resolve so the transaction can be re-attempted? That is the right question for a subscription billing platform managing involuntary churn. It is the wrong question for a collections operation trying to recover payments from customers who have stopped paying.

According to Braintree's own developer documentation, when a subscription goes past due the platform executes three built-in automated retries before marking it past due, then continues retrying on whatever interval the merchant has configured. The entire architecture assumes that if the transaction is attempted enough times, the technical barrier will eventually clear. For technically failed payments from customers who intend to pay, that assumption is sometimes correct. For genuinely delinquent accounts, it is almost never correct.

The collections teams reading this have already learned this distinction the hard way. The retry sequence ran. The balance aged. The account moved from 30-day delinquency to 60 to 90-day. The charge-off line grew. Every quarter, the same architecture produced the same result, because it was never designed for the problem it was being applied to.

The Delinquency Context: Why This Problem Is Growing

Before evaluating the architectural gap between Braintree and FinanceOps Agentic AI, it is worth understanding why that gap matters more in 2026 than at any point in recent memory.

Federal Reserve Bank of New York, Q1 2026: 4.8% of all outstanding household debt is in some stage of delinquency. Credit card early delinquency transition rates stand at 8.6% annually, meaning nearly one in eleven credit card accounts entered early delinquency in the past year. Total credit card balances reached $1.252 trillion, up 63% since Q1 2021.

ACA International and WebRecon, 2025 Year-End Report: FDCPA lawsuits increased 7.8% year-over-year to 4,534 cases filed. CFPB complaints nearly doubled from 159,000 in 2024 to more than 302,000 in 2025. In January 2026 alone, FDCPA filings were already 26.5% ahead of January 2025. The compliance exposure attached to delinquent consumer outreach is not stable. It is accelerating.

CFPB Annual FDCPA Report, December 2025: The CFPB received approximately 207,800 debt collection complaints in 2024, nearly double the 109,900 received in 2023. The most cited categories were failure to validate debt, contact frequency violations, and improper channel usage, every one a direct consequence of applying payment processing infrastructure to a debt recovery problem that federal law explicitly governs.

More accounts are delinquent. More consumers are filing complaints. Regulatory scrutiny is intensifying. Every organisation still using Braintree's retry architecture as its primary recovery tool is managing that environment with infrastructure designed for a fundamentally different problem.

The Five Structural Gaps in Braintree's Retry Logic

Gap 1: No Account-Level Delinquency Intelligence

Braintree's intelligence layer was built for authorized payment behavior. It optimizes retry timing for technical failures and detects fraud in authorization flows. It has no model for what a delinquent account is communicating.

It cannot detect that a customer has visited the payment portal six times in two weeks without completing a transaction, the single strongest behavioral signal that a restructured payment plan would resolve the barrier

It cannot distinguish that account from one where the customer has stopped all engagement entirely

Both receive the same retry attempt on the same schedule

FinanceOps Agentic AI builds an account-level behavioral model before any outreach is initiated, analyzing payment history, channel responsiveness, engagement patterns, device signals, and real-time behavioral cues at the individual account level. That intelligence is what produces a 12 to 15% right-party contact rate against the 2% industry norm from schedule-based outreach.

Gap 2: No Sentiment Detection Layer

When a customer responds to a failed-payment notification explaining they cannot pay in full right now, Braintree has no mechanism to read that response and adjust. The next retry goes out on schedule. The next notification goes out on schedule. The system has no concept of what the customer communicated.

In a B2C environment, this failure is expensive. A customer in genuine financial hardship who receives escalating payment demands will disengage, and in a self-serve digital product context that disengagement is often permanent. The account does not merely fail to recover. The customer relationship ends.

FinanceOps Agentic AI applies real-time sentiment analysis across every channel in every interaction. A hardship signal in an SMS response triggers a different outreach path than a high-intent signal from repeated portal visits. Tone, channel, and payment structure are calibrated in real time to what the customer is actually communicating, not what a fixed retry schedule assumes.

Gap 3: No Cross-Channel Context Continuity

Braintree's dunning architecture is email-centric. If a customer replies to a failed-payment email explaining their situation and then calls support, the agent has zero context from the prior exchange. The customer re-explains. The agent has no record. The moment of highest payment intent becomes the moment of maximum friction.

At scale, this channel discontinuity converts payment intent into disengagement. A customer willing to work out a payment arrangement gives up because the process required them to start over every time they switched channels.

FinanceOps Agentic AI maintains a single unified conversation record across SMS, email, Voice AI, webchat, and self-service portals. Every channel switch is a continuation of the existing conversation, not a reset.

Gap 4: No Flexibility for What the Customer Can Actually Pay

Braintree retries the original transaction amount. If a customer could not pay $312 on the first attempt, the architecture retries $312 at a different time. There is no mechanism to evaluate whether three monthly installments of $104 would produce full recovery where the full-amount retry produces abandonment.

Promise-to-pay abandonment rates in traditional collections average 38 to 45%, according to Deloitte's 2024 Financial Services AI Outlook. The primary driver is not bad intent. It is a payment structure calibrated to the balance owed rather than what the customer can sustain.

FinanceOps Agentic AI evaluates actual repayment capacity before proposing any payment structure, drawing on payment history, income and expense signals, real-time sentiment indicators, and financial stress cues. The output is a schedule calibrated to what this specific customer can hold, reducing PTP abandonment from the 38 to 45% industry average to under 20%.

Gap 5: No FDCPA and TCPA Compliance Architecture

Braintree's compliance infrastructure was built for payment security: PCI DSS, fraud prevention, card network rules. It was not built to enforce:

FDCPA contact frequency limits

TCPA safe-hour requirements

CFPB Regulation F validation notice obligations

FCC Revoke All consent enforcement, effective April 11, 2026, which requires a single revocation through any channel to immediately halt all outreach across every channel simultaneously.

Manual consent tracking cannot enforce the Revoke All requirement at portfolio scale. Every notification sent after a revocation event is a potential TCPA violation with private right-of-action exposure and statutory damages attached.

FinanceOps Agentic AI encodes all of the above as structural workflow properties before the platform contacts any account. A consent revocation in any channel propagates immediately across all outreach channels without manual intervention, with audit-ready documentation generated automatically at every touchpoint.

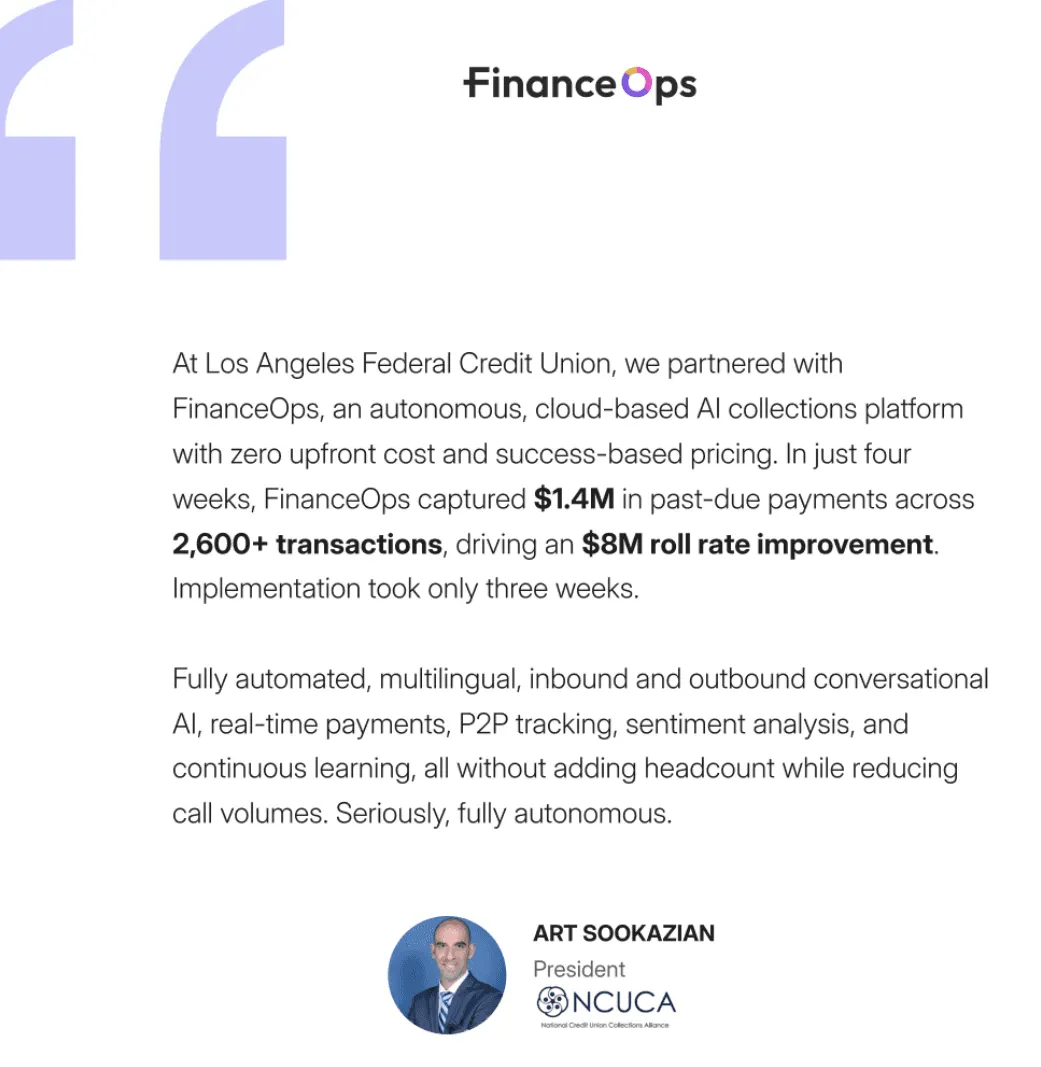

LAFCU Case Study: $1M Collected in 21 Days

The structural gaps described above are not theoretical. They are measurable. LA Federal Credit Union, a nearly $1 billion institution serving more than 50,000 members in Los Angeles, ran directly into every one of them before deploying FinanceOps Agentic AI in early 2026.

The problem before deployment:

30 to 60 DPD delinquency balance sitting at approximately $12 million

Contact rates at the approximately 2% industry norm, meaning 98 of every 100 outreach attempts produced no response while consuming the full compliance overhead of all 100 attempts

Collections activating only after accounts had already aged past the early-resolution window

One-way outreach with no frictionless path for members to respond, negotiate, or pay directly from the interaction

Single-language English outreach structurally failing a membership base spanning Spanish, Armenian, Persian, and dozens of other language communities before a single substantive conversation could begin

What happened in 21 days after deployment:

FinanceOps Agentic AI was configured to LAFCU's operational requirements, member-first philosophy, Scimitar core system integration, and California regulatory compliance environment. The results did not take months to materialize.

30 to 60 DPD delinquency balance reduced from $12M to approximately $3.8M, a 65%+ improvement

12 basis point drop in the 30+ DQ ratio

Approximately 1,650 early-stage payments processed in the first 21 days

$800K+ in delinquent payments collected within the first week of full ramp

$1M+ in total delinquent dollar balances resolved across the portfolio

93 open promise-to-pay commitments totaling $57K tracked and managed autonomously

48% recovery rate achieved with under 10 minutes of human effort per day

Only 6 AI-generated cases requiring human specialist review across 1,650+ payments processed

Contact rates improved from approximately 2% to 12 to 15%, a 6 to 7x improvement

100% FDCPA-compliant operations across every member interaction from day one

Native multilingual outreach across Spanish, Armenian, Persian, and 150+ additional languages

Art Sookazian, President of NCUCA and Vice President of Special Services at LA Federal Credit Union, described the results directly:

Why the results arrived at this speed:

Three decisions explain the 21-day outcome, each mapping directly to the structural gaps legacy payment retry architecture cannot close.

Activating at 15 DPD changed the recoverable universe. Engaging members at the moment recovery probability is highest and cost per contact is lowest means reaching accounts before hardship compounds, before negative credit impacts set in, and before balances age into the late-stage portfolio where recovery requires significantly more effort. Organisations that activate at 30 or 45 DPD are not running a slower version of the same process. They are working on a fundamentally harder problem.

A 6 to 7x contact rate improvement compounded across every downstream metric. Moving from 2% to 12 to 15% right-party contact rates improved not just recovery volume but promise-to-pay completion rates, sentiment-adjusted engagement, and member trust. Those metrics only move when the right member is reached at the right moment.

Multilingual infrastructure was a precondition, not a feature. For LAFCU, any collections platform that could not reach Spanish, Armenian, and Persian-speaking members in their preferred language was not a partial solution. It was a structural failure affecting a significant share of the delinquency portfolio before the first contact attempt. Native 150-language capability made the process functional across the full membership base for the first time.

Before vs. After FinanceOps Agentic AI at LAFCU:

The LAFCU result is the clearest available proof of what happens when retry architecture is replaced with recovery architecture. Every credit union or consumer receivables operation with a similar 30 to 60 DPD concentration is sitting on the same recoverable value. The only variable is whether the infrastructure is in place to act on it before it ages out of reach.

Affordability-Based Plans vs. Retry-the-Same-Amount Logic

The difference between a payment plan a customer will complete and one they will abandon is almost never about intent. It is almost always about structure.

Braintree's architecture has one payment structure: the original transaction amount, retried at intervals. There is no evaluation of affordability. There is no assessment of whether a restructured payment plan would produce completion where the full-amount retry produces abandonment. The platform applies the same response to every delinquent account regardless of its behavioral profile, its financial signals, or what the customer has communicated about their ability to pay.

This single-structure approach is the primary driver of the 38 to 45% promise-to-pay abandonment rate that Deloitte's 2024 Financial Services AI Outlook identifies as the industry norm. When a customer commits to a payment plan structured around what they owe rather than what they can actually sustain, nearly half of those commitments do not produce a completed payment.

FinanceOps Agentic AI builds payment plan structures around the customer's demonstrated repayment capacity:

Weekly installments for customers managing tight cash flow windows between paycheck cycles

Bi-weekly installments aligned with the customer's income timing and pay schedule

Monthly installments for customers with irregular or seasonal income patterns

Custom installment structures for accounts with specific financial constraints identified through behavioral analysis

The output of this approach is a reduction in PTP abandonment from the 38 to 45% industry average to under 20%. Every payment plan that holds is a customer account that never reaches the late-stage delinquency bucket. Every payment plan that holds is a customer relationship that survived the financial hardship without disengagement, complaint escalation, or churn.

Braintree retries the amount. FinanceOps negotiates the structure. Debt recovery at scale requires negotiation.

Braintree vs. FinanceOps Agentic AI: Full Head-to-Head

This is not a feature comparison. It is a comparison between payment processing infrastructure built for technical payment failures and recovery infrastructure built for delinquent accounts where the barrier is behavioral or financial.

The Compliance Exposure Braintree Cannot Address

The FCC's Revoke All consent rule, effective April 11, 2026, created a structural compliance requirement that most payment processors and legacy collections platforms were never built to meet.

What the rule requires:

A single consent revocation through any channel, a reply-STOP to a text, an email unsubscribe, or a verbal opt-out on a call, immediately halts all outreach across every channel simultaneously

Not after a manual review. Not after a processing queue clears. Immediately.

Every automated communication sent after a revocation event on a different channel is a potential TCPA violation with private right-of-action exposure

Why manual enforcement is not viable:

Consumer receivables portfolios with hundreds or thousands of active accounts cannot track cross-channel revocation events manually at the speed the rule requires

FDCPA lawsuit filings rose 26.5% year-over-year in January 2026 alone, per ACA International

CFPB complaints nearly doubled in 2025

The regulatory environment for consumer collections outreach is not stabilizing. It is intensifying.

The core gap: Braintree's architecture was built for PCI DSS payment security on authorized transactions. That compliance framework and what the FCC Revoke All rule now requires are not the same problem and the gap between them is not closable through configuration or third-party integration.

How FinanceOps handles it:

Revoke All propagation is encoded as a structural requirement, not a workflow setting

A revocation received in any channel immediately halts all outreach across all channels before the next scheduled contact executes

No manual intervention required. No queue processing lag.

Timestamped audit documentation generated automatically at every touchpoint

Structural FDCPA contact frequency enforcement, TCPA safe-hour requirements, and CFPB Regulation F validation notice generation are all built in

This is the compliance infrastructure that collections and receivables teams operating in 2026 actually need. It is not something any payment processor was ever designed to offer.

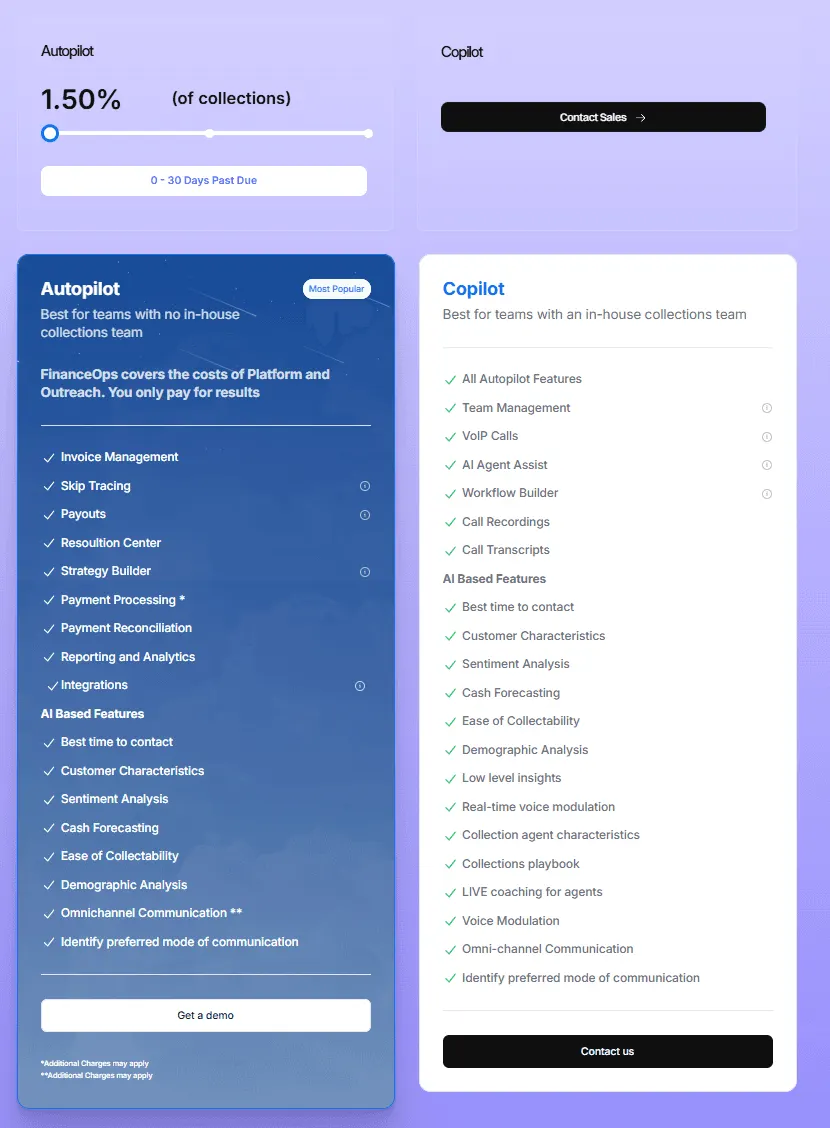

Why 1.5% Is the Only Aligned Pricing Model

The pricing model of a vendor is the most direct available signal of what that vendor was built to produce.

Braintree charges 2.59% plus $0.49 per card or digital wallet transaction, plus additional subscription fees for advanced features. That fee is identical regardless of whether your delinquency rate improves or worsens, whether your aging report gets better or worse each quarter, and whether your charge-off line grows or shrinks. Braintree's revenue is entirely disconnected from your collections performance, because collections performance was never the problem Braintree was built to produce.

FinanceOps Agentic AI charges 1.5% of collections recovered. No upfront cost. No subscription fee. No credit card required to start. If no collections occur, the fee is zero and FinanceOps absorbs all platform and outreach costs.

What 1.5% means across different portfolio sizes:

The 1.5% model also creates a vendor whose institutional incentives are directly aligned with your recovery outcome. A vendor paid 1.5% of what it recovers has every organizational reason to recover as much as possible, as quickly as possible, in a way that preserves the customer relationship so that future billing cycles remain viable. Aggressive, tone-deaf collections outreach that produces a complaint, a churn event, or an FDCPA violation costs FinanceOps revenue on the next billing cycle. Its incentive structure is aligned with your long-term customer relationships, not just the immediate balance.

That alignment is the most direct structural proof of a debt recovery platform. And it is the most important feature comparison that never appears on a payment processor's product page.

Key Takeaways

Payment retry logic and debt recovery solve different problems. Braintree is designed to recover technically failed payments from customers who still intend to pay. It is not built for delinquent accounts where the barrier is behavioral or financial, making retry-based recovery structurally ineffective for aging receivables portfolios.

LA Federal Credit Union reduced its 30–60 DPD delinquency balance from $12M to $3.8M in 21 days, collected $1M+ in delinquent balances, and achieved a 48% recovery rate with under 10 minutes of daily human effort after replacing retry-based collections infrastructure with FinanceOps Agentic AI.

FinanceOps charges 1.5% only on recovered balances, with no upfront fees and no cost if no recovery occurs. Unlike transaction-based pricing models, FinanceOps’ pricing is directly aligned with improving recovery outcomes and reducing charge-offs.

Ready to See What Recovery Architecture Delivers in Your Portfolio?

Book a free 20-minute demo with FinanceOps Agentic AI. Your delinquent accounts, your failed-payment portfolio, your charge-off trend, mapped against what behavioral intelligence, Skip-A-Pay, affordability-based payment plans, and structurally compliant autonomous outreach actually produce in your specific receivables environment.

No upfront cost. No subscription. 1.5% of collections recovered. You pay only when your customers pay.

FAQs

Our business uses Braintree for recurring billing, but delinquency rates keep increasing despite optimizing retry settings. What are we missing?

Braintree’s retry logic is designed to recover payments that fail because of technical issues such as expired cards, bank holds, or authorization failures. Delinquent accounts are usually different because the problem is behavioral or financial, not technical. Retrying the same payment at different intervals does not resolve that issue. FinanceOps Agentic AI addresses this by analyzing delinquency signals, optimizing outreach strategies, and offering payment structures customers can realistically sustain.

What is the difference between payment processor dunning and a debt recovery platform?

Payment processor dunning focuses on recovering failed transactions caused by temporary payment interruptions by retrying payments and sending reminders. A debt recovery platform like FinanceOps Agentic AI is designed for customers who have stopped paying entirely by analyzing customer behavior, optimizing communication strategies, offering flexible repayment options, and managing outreach within FDCPA, TCPA, and CFPB Regulation F requirements. Braintree charges per transaction regardless of outcome, while FinanceOps charges only on recovered balances.

How does the FCC’s Revoke All rule impact delinquent account outreach?

The FCC’s Revoke All rule, effective April 11, 2026, requires businesses to stop all outreach across every communication channel immediately after a customer revokes consent in any channel. A STOP reply to SMS, an email unsubscribe, or a verbal opt-out must halt all future outreach across SMS, email, and phone simultaneously. Businesses without centralized consent management systems may face TCPA exposure if communications continue after revocation. FinanceOps Agentic AI automatically enforces cross-channel consent propagation and maintains audit records across all touchpoints.

How does FinanceOps pricing compare to traditional collection agencies?

Traditional collection agencies typically charge 25–35% of recovered balances. On a $1M delinquent portfolio with a 50% recovery rate, a traditional agency charging 30% would keep $150,000 of the $500,000 recovered. FinanceOps charges 1.5% on recovered balances, which would equal $7,500 on the same recovery amount. FinanceOps also charges no upfront fees, subscriptions, or recovery fees when no collections occur.