Blog

Square vs FinanceOps AI for Collections Recovery

Jun 15, 2026

Blog Summary

Square helped millions of small businesses accept card payments, but it assumes customers are ready to pay. It was never built to manage overdue accounts, aging balances, or structured recovery.

FinanceOps Agentic AI solves this with account-level behavioral intelligence, real-time sentiment, affordability-based payment plans, and structural FDCPA compliance at 1.5% of collections recovered, with no upfront cost and no fee if nothing is collected.

This blog explains why using Square invoicing or payment links for overdue accounts leads to growing aging reports, and what a recovery-focused architecture looks like.

Table of Contents

What Is Square Actually Built to Do?

Why Are Small Business Receivables a Different Problem?

What Are the Five Gaps in Square's Payment Architecture?

What Does This Mean for CFOs and Finance Leaders?

What Do the Recovery Economics Actually Look Like?

What Is Skip-A-Pay and Why Can't Square Offer It?

How Did Enamel Dentistry Resolve 90% of 120+ DPD Accounts?

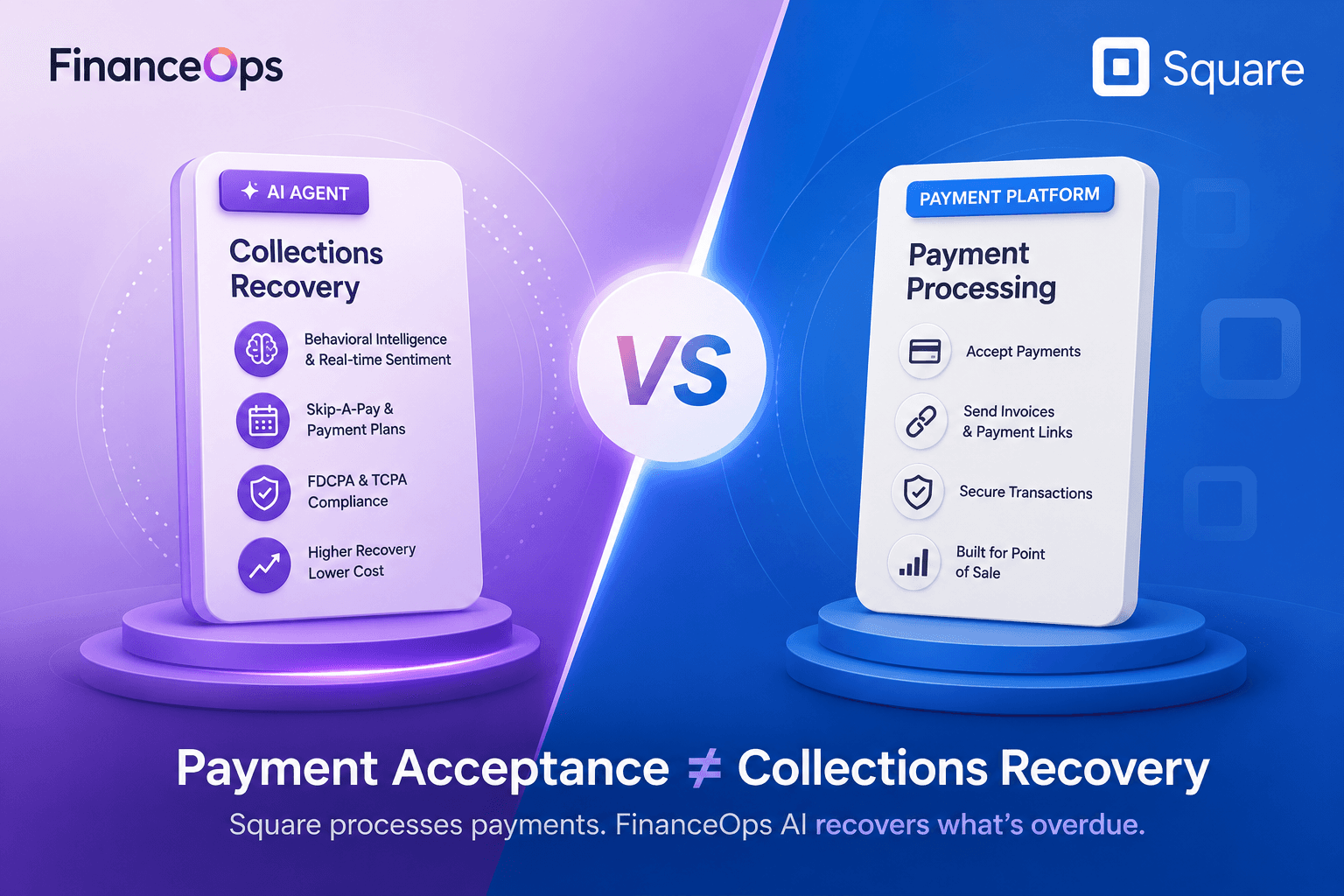

Square vs. FinanceOps Agentic AI: Which Solves Collections?

Why Is 1.5% the Only Aligned Collections Pricing Model?

Key Takeaways

FAQs

What Is Square Actually Built to Do?

Square deserves its reputation. It democratized payment processing for small businesses that previously could not afford the hardware, the contracts, or the technical complexity of enterprise payment infrastructure. A dental practice, a healthcare clinic, a local utility provider, a small lender. Square gave all of them a frictionless way to accept payment at the point of service.

Every element of Square's product is built around one foundational assumption: the customer has decided to pay and needs a convenient, reliable mechanism to do so. That assumption holds perfectly for the moment of sale. It breaks completely the moment an account goes delinquent.

When a patient misses a payment, when a utility customer stops paying, when a borrower becomes 30 days past due, the problem is no longer a payment acceptance problem. It is a collections recovery problem. The customer has not decided to pay. The reason they stopped matters enormously. The outreach that re-engages them is governed by federal law. The payment structure that produces completion must be calibrated to what they can actually sustain.

Square's payment links do not adapt to hardship signals. Its digital invoices do not read sentiment. Its compliance infrastructure was built for PCI DSS payment security, not FDCPA contact frequency limits or TCPA consent enforcement. This is not a criticism of Square. It is a precise description of a problem Square was not designed to solve.

Why Are Small Business Receivables a Different Problem?

The organizations most likely to be using Square, healthcare practices, dental offices, local service businesses, small lenders, and utilities, share a specific receivables challenge that makes the gap between payment acceptance and collections recovery especially consequential.

Their delinquent accounts are disproportionately small-balances: Traditional collections agencies charge 25 to 40% of recovered balances, making small-balance recovery structurally unworkable. A $200 dental balance at 35% contingency produces $70 for the agency and $130 for the practice. After administrative overhead, writing the account off becomes the easier business decision. The write-offs compound until the accumulated loss becomes invisible and normalized.

Their customer relationships are ongoing: A dental practice that damages a patient relationship through aggressive collections outreach does not just lose the recovery. It loses all future revenue from that patient. The collections process must preserve the relationship, not just recover the balance. No point-of-sale platform was designed with that constraint as a governing requirement.

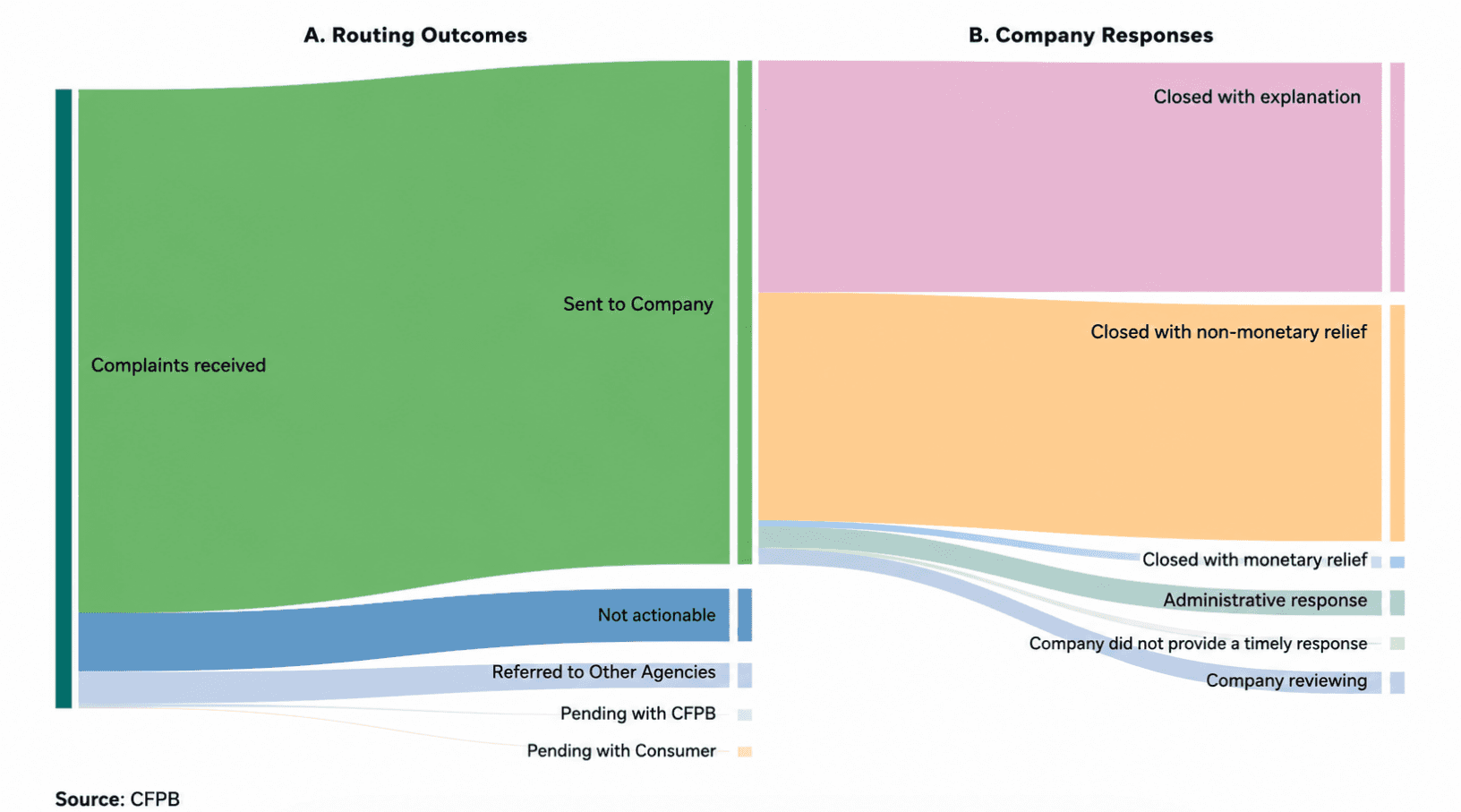

Their compliance exposure is real and accelerating: According to the Consumer Financial Protection Bureau's Annual Debt Collection Report, the CFPB received approximately 207,800 debt collection complaints in 2024, nearly double the 109,900 received in 2023. Healthcare and utility receivables are not exempt from FDCPA and TCPA requirements. A dental practice sending repeated automated payment reminders without proper consent management is not protected by its size or its industry.

What Are the Five Gaps in Square's Payment Architecture?

Gap 1: Does Square Have Behavioral Intelligence for Delinquent Accounts?

Square was not designed to know why a customer stopped paying. It cannot detect that a patient has opened a payment link three times this week without completing the transaction, the single clearest signal that a restructured payment option would close the gap. It cannot distinguish that account from one where the customer has stopped all engagement entirely.

FinanceOps Agentic AI builds an account-level behavioral profile before any outreach begins. It analyzes payment history, channel responsiveness, engagement patterns, and real-time behavioral signals at the individual account level, producing a 12 to 15% right-party contact rate against the 2% industry norm.

Gap 2: Does Square Adjust Tone Based on Customer Sentiment?

Square's invoicing and payment reminder architecture sends the same message on the same schedule regardless of what the customer has communicated. There is no sentiment layer, no mechanism to detect hardship cues, adjust tone, or redirect a high-stress interaction toward a flexible resolution path before the customer disengages entirely.

FinanceOps Agentic AI applies real-time sentiment analysis across every channel in every interaction. A customer signaling financial stress receives empathetic, flexibility-first communication. A customer signaling avoidance receives a different approach entirely. The system responds to what each customer is actually communicating, not to a fixed schedule.

Gap 3: Does Square Maintain Context Across Channels?

A customer who receives a Square payment reminder via email, calls to explain their situation, and then receives another automated reminder the following week has been told three separate times that the organization was not listening. In healthcare and service environments, that experience does not feel like a system failure. It feels like organizational indifference. The payment does not happen. The relationship ends.

FinanceOps Agentic AI maintains a single unified conversation record across SMS, email, Voice AI, webchat, and self-service portals. The context never resets. The resolution path stays open across every channel switch.

Gap 4: Does Square Enforce FDCPA and TCPA Compliance?

Square's compliance infrastructure was built for PCI DSS, the standard governing secure payment processing. That standard has zero relevance to collections compliance.

The FCC Revoke All rule, effective April 2026, requires a single consent revocation through any channel to immediately halt all outreach across every channel simultaneously. For organizations using automated payment reminders without centralized consent management, every contact made after a revocation event in a different channel is potential TCPA exposure with statutory damages attached.

FinanceOps Agentic AI encodes FDCPA, TCPA, CFPB Regulation F, and FCC Revoke All as structural workflow properties before the platform contacts any account. Consent revocation propagates immediately across all channels. Every interaction is timestamped and audit-ready automatically.

Gap 5: Does Square Price on Recovery Outcomes?

Square charges 2.6% plus $0.10 on every transaction whether or not the delinquency rate improves. A dental practice that doubles its recovery rate pays Square exactly the same amount as one whose write-offs compound every quarter. Square's revenue is entirely disconnected from collections performance because collections performance was never the output Square was designed to produce.

FinanceOps Agentic AI charges 1.5% of collections recovered. No upfront cost. No subscription. Zero fee if no recovery occurs.

What Does This Mean for CFOs and Finance Leaders?

Collections infrastructure is a balance sheet decision. Every delinquent account that ages past 90 days without resolution represents not just a missed recovery, but a compounding working capital cost.

For CFOs evaluating Square against FinanceOps Agentic AI, the question is not which platform has better payment features. The question is which platform reduces reserve requirements, accelerates cash conversion, and protects the organization from regulatory exposure simultaneously.

Square's architecture addresses none of those three outcomes for delinquent accounts. It was built for payment volume, not recovery performance. Its fee structure confirms that. A vendor charged on transaction volume has no institutional reason to improve your aging report.

FinanceOps Agentic AI addresses all three.

Reserve reduction follows directly from earlier-stage account resolution.

Cash acceleration follows from 2 to 3 week recovery windows replacing 90 to 120 day agency timelines.

Regulatory protection follows from structural FDCPA, TCPA, and CFPB compliance enforcement encoded before first contact. And all of it comes at 1.5% of what is actually recovered.

What Do the Recovery Economics Actually Look Like?

The economics that made small-balance recovery unworkable through traditional channels become entirely different at 1.5% of collections recovered.

Recovery Model | $50,000 Portfolio at 70% Recovery | Fee | Net Recovery |

Write-off | $0 recovered | $0 | $0 |

Traditional agency at 35% | $35,000 recovered | $12,250 | $22,750 |

FinanceOps at 1.5% | $35,000 recovered | $525 | $34,475 |

On a single $50,000 small-balance portfolio, FinanceOps produces $11,725 more in net recovery than a traditional agency at 35%, in 2 to 3 weeks instead of 90 to 120 days, with zero upfront cost and zero fee if nothing is recovered.

At the individual account level, a $200 dental balance recovered through FinanceOps costs $3 in platform fees. The same recovery through a traditional agency at 35% costs $70 and takes four months. The practice nets $197 from FinanceOps versus $130 from an agency, in a fraction of the time.

These are not incremental improvements in recovery economics. They are the difference between a recoverable portfolio and a normalized write-off line.

See what FinanceOps recovers on your first 10,000 accounts, free, no upfront cost, no subscription.

What Are Flexible Payment Plans and Why Can't Square Offer Them?

Flexible Payment Plans Powered by FinanceOps Agentic AI

Flexible Payment Plans is the single clearest illustration of what separates payment acceptance infrastructure from collections recovery architecture. It is also the capability that most directly prevents the outcome every small business and healthcare organization is trying to avoid: a customer who cannot pay this month becomes an account that is never recovered.

What happens inside Square's architecture when a customer cannot make a payment:

A payment link goes unclicked. An invoice ages past due. A reminder goes out on day seven, another on day fourteen. If no payment occurs, the account moves into manual follow-up or gets written off. Square has no mechanism to assess why a customer hasn't paid or what they can realistically afford. It was designed to process payments from customers who have already decided to pay, not to work with those who are struggling.

What FinanceOps Agentic AI's Flexible Payment Plans do:

Agentic AI evaluates each customer's actual repayment capacity by analyzing historical payment behavior, income and expense signals, sentiment indicators, transaction patterns, and financial stress cues. Based on this analysis, it recommends structured, realistic payment schedules, including weekly, bi-weekly, monthly, or custom installment-based plans, tailored to what the customer can genuinely sustain.

The account stays current. No late fees are incurred. No relationship damage occurs. Because the plan is matched to actual affordability rather than a fixed default schedule, customers are far more likely to stick with it, improving long-term liquidation rates while reducing roll rates and defaults.

An account that would have aged into 60+ day delinquency and been written off stays current. A patient who would have disengaged because the platform had no answer for their situation remains a patient. The relationship holds. The revenue is recovered. No payment acceptance platform produces that outcome.

How Did Enamel Dentistry Resolve 90% of 120+ DPD Accounts?

Enamel Dentistry represents the proof case for every small business and healthcare organization currently managing small-balance delinquent accounts through Square invoices and payment links.

A healthcare practice with small-balance delinquent accounts that were economically impossible to recover through traditional means. Agency fees that exceeded the recovered value. Manual follow-up that consumed staff time. Patient relationships that could not survive aggressive outreach. Enamel Dentistry deployed FinanceOps Agentic AI against exactly this problem.

90% reduction in 120+ DPD small-balance accounts.

$100,000+ saved from reduced agency fees.

70% increase in payment response rates.

Recovery window compressed from 120+ days to 2 to 3 weeks.

60% operational cost reduction. 100% HIPAA-compliant workflows throughout every interaction.

The economics that made agency-based recovery unworkable for small-balance healthcare accounts became entirely viable at 1.5% of recovered balances. The patient relationships that could not survive aggressive collections outreach were preserved through empathetic, sentiment-adaptive communication calibrated to what each patient was actually communicating.

The 120-day recovery window compressed to 2 to 3 weeks. Not because FinanceOps applied more pressure. Because it applied the right approach at the right moment through the right channel to the right person. Which is precisely what a payment acceptance platform was never designed to do.

Every dental practice, healthcare clinic, and small business managing delinquent accounts with Square invoices is sitting on a recoverable portfolio that current economics make invisible. The Enamel Dentistry result makes that portfolio visible and recoverable.

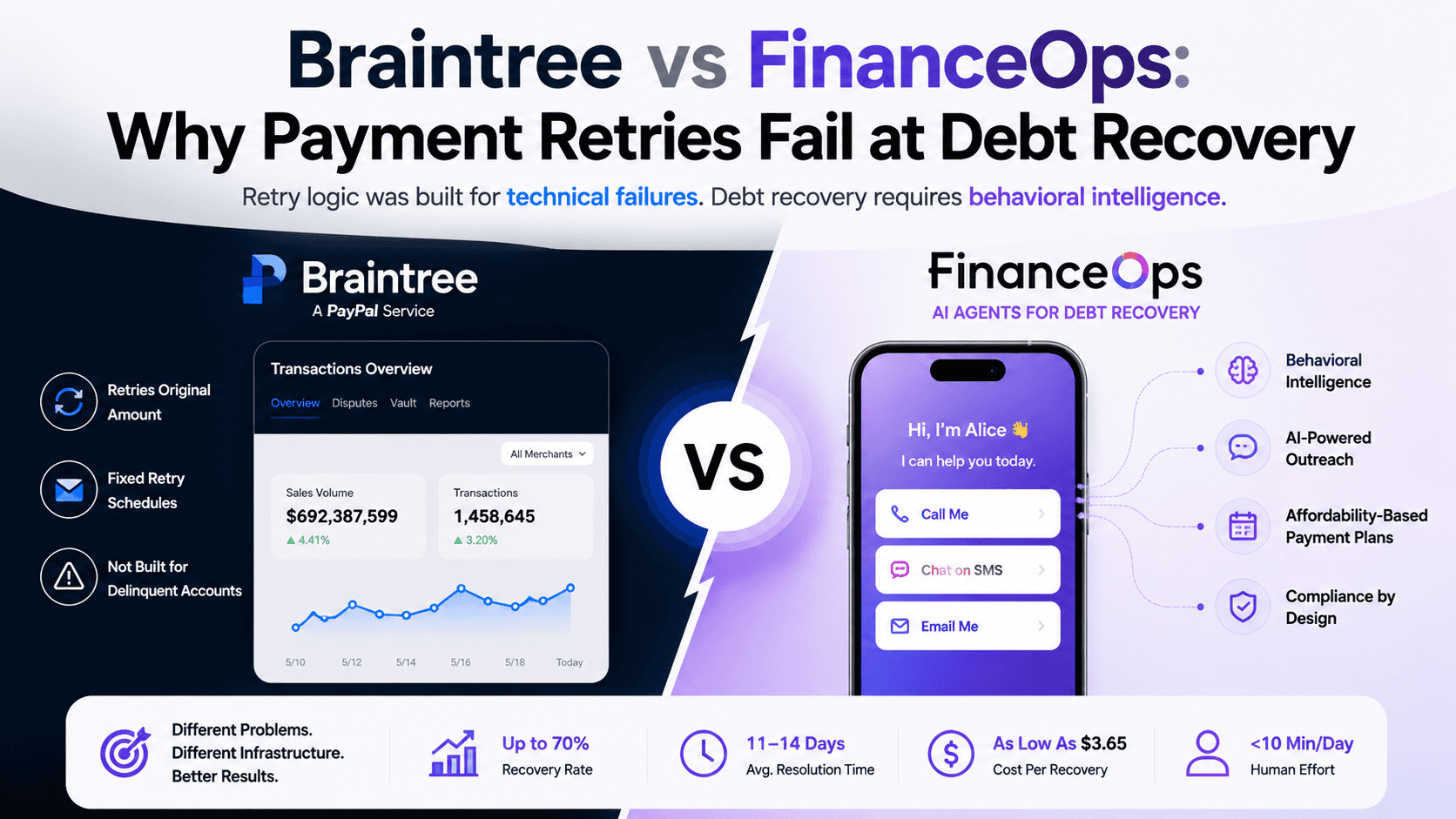

Square vs. FinanceOps Agentic AI: Which Solves Collections?

Capability | Square | FinanceOps Agentic AI |

Purpose | Payment acceptance | Delinquent account recovery |

Behavior & Sentiment Intelligence | Not designed for collections | Real-time, per account, live across all channels |

Outreach Channels & Context | Email, payment links | SMS, email, Voice AI, webchat, portals; full context maintained |

Skip-A-Pay & Recourse | Not available | Full capability, credit risk assumed, full balance paid upfront |

Affordability-Based Plans | Not available | Calibrated to actual repayment capacity |

PTP Abandonment | 38–45% industry average | Under 20% |

Compliance | Not designed for collections | FDCPA, TCPA, CFPB Reg F, FCC Revoke All enforced before first contact; HIPAA across healthcare deployments |

Right-Party Contact Rate | Not tracked | 12–15% vs 2% industry norm |

Cost & Efficiency | Manual AR & follow-up; 2.6% + $0.10 per transaction | Under 10 minutes/day; as low as $3.65 per recovery; 1.5% of recovered balances; nothing if nothing is recovered |

Resolution & Audit | Manual, no automation | Average resolution 2–3 weeks; audit-ready documentation at every touchpoint |

This is not a comparison between two competing products serving the same problem. It is a comparison between a payment acceptance platform built for willing customers and a collections recovery platform built for delinquent ones.

Why Is 1.5% the Only Aligned Collections Pricing Model?

The pricing model of a vendor is the most direct available signal of what that vendor was built to produce.

Square charges on transaction volume. Whether the delinquency rate improves or worsens, whether the aging report gets better or worse each quarter, Square's fee is identical. Its roadmap serves merchants managing payment authorization. The aging report is not its problem to solve, and its pricing model confirms that.

FinanceOps Agentic AI charges 1.5% of collections recovered. No upfront cost. No subscription. No fee if no recovery occurs. FinanceOps absorbs all platform and outreach costs on accounts that do not recover. The first 10,000 accounts are processed free.

FinanceOps Agentic AI

The 1.5% model also creates a vendor whose institutional incentives are directly aligned with preserving the patient or customer relationship. Aggressive collections outreach that produces a complaint, a churn event, or an FDCPA violation costs FinanceOps recovery revenue on every future billing cycle with that account. Its incentive structure is calibrated toward empathetic, effective recovery, not maximum pressure applied to every account regardless of signal.

That alignment is the most important structural proof of a collections recovery platform. And it is a feature that never appears on a payment processor's product page.

Key Takeaways

Square was built for payment at sale, not for delinquency. Once a customer stops paying, its architecture cannot recover accounts.

Small-balance accounts in healthcare and services are uneconomical to recover with traditional agencies charging 25–40%. FinanceOps collects at 1.5%, making recovery viable in 2–3 weeks.

Affordability-based plans turn customers who can’t pay today into recovered accounts, while Square only resends invoices. FinanceOps covers the balance, assumes credit risk, and collects in installments.

FCC Revoke All compliance requires halting outreach immediately after consent revocation. Square lacks centralized enforcement; FinanceOps encodes it structurally before any contact.

Enamel Dentistry results: 90% reduction in 120+ DPD accounts, $100,000+ saved on agency fees, recovery window compressed to 2–3 weeks, and 100% HIPAA-compliant.

Ready to See What Recovery Architecture Delivers for Your Portfolio?

Book a free 20-minute demo with FinanceOps Agentic AI. Your delinquent accounts, healthcare receivables, and charge-off trends mapped against what behavioral intelligence, Skip-A-Pay, payment plans, and compliant autonomous outreach deliver in your portfolio.

No upfront cost. No subscription. 1.5% of collections recovered. You pay only when your customers pay.

FAQs

Can Square collect overdue invoices and recover delinquent accounts?

Square was designed to process payments from customers who have decided to pay. Its invoicing and payment reminder functionality resends the same payment request on a schedule and was not designed to analyze why a customer stopped paying, adjust outreach tone based on hardship signals, offer an alternative payment structure, or enforce FDCPA compliance at the account level. For genuinely delinquent accounts, Square's architecture produces repeated invoice sends and eventually a write-off. FinanceOps Agentic AI was built specifically for delinquent account recovery.

Does Square offer payment plans for delinquent customers?

No. Square's architecture has one payment structure: the invoice amount. It was not designed to evaluate affordability, propose installment schedules, or calibrate a payment structure to what a specific customer can actually sustain. FinanceOps Agentic AI evaluates repayment capacity from payment history, income signals, and live sentiment before proposing any plan, reducing promise-to-pay abandonment from the 38 to 45% industry average to under 20%.

Can Square recover delinquent accounts for dental and healthcare practices?

Square was not designed for healthcare collections recovery. It does not offer HIPAA-compliant collections workflows, behavioral intelligence for delinquent patient accounts, or affordability-based payment plans. FinanceOps Agentic AI operates with 100% HIPAA-compliant workflows across every healthcare deployment, as demonstrated in the Enamel Dentistry case study where 90% of 120+ DPD accounts were resolved in 2 to 3 weeks.

What is Skip-A-Pay and why was Square not designed to offer it?

Skip-A-Pay allows FinanceOps to cover a customer's outstanding balance on their behalf when they cannot pay today, keeping the account current and avoiding late fees or relationship damage. FinanceOps collects repayment in three manageable installments while assuming the credit risk entirely. Square's architecture was designed to process authorized payments and was not built to cover customer obligations, assume credit risk, or collect repayment through installments.

Square vs collections software: which is right for overdue accounts?

Square is the right tool for payment acceptance at the point of sale. A collections software platform like FinanceOps Agentic AI is the right tool for recovering overdue accounts where the customer has stopped paying. These are structurally different problems requiring different data models, different compliance frameworks, and different pricing structures. For organizations managing aging receivables, Square's architecture was not designed to produce recovery outcomes.

How does 1.5% of collections compare to what small businesses currently pay?

Traditional collections agencies charge 25 to 40% of recovered balances with no guarantee of recovery and a process that typically takes 90 to 120 days. On a $50,000 small-balance portfolio with a 70% recovery rate, a traditional agency at 35% charges $12,250. FinanceOps charges $525 on the same recovery, with results delivered in 2 to 3 weeks and zero fee if no recovery occurs. The first 10,000 accounts are processed free.

Does Square offer any debt collection or delinquent account recovery capability?

No. Square is a payment acceptance platform. It was not designed to offer behavioral intelligence for delinquent accounts, sentiment-adjusted collections outreach, Skip-A-Pay, affordability-based payment restructuring, FDCPA or TCPA compliance governance at the account level, or any pricing model tied to delinquent account recovery outcomes. These capabilities require a platform built specifically for collections recovery.

Blog Summary

Square helped millions of small businesses accept card payments, but it assumes customers are ready to pay. It was never built to manage overdue accounts, aging balances, or structured recovery.

FinanceOps Agentic AI solves this with account-level behavioral intelligence, real-time sentiment, affordability-based payment plans, and structural FDCPA compliance at 1.5% of collections recovered, with no upfront cost and no fee if nothing is collected.

This blog explains why using Square invoicing or payment links for overdue accounts leads to growing aging reports, and what a recovery-focused architecture looks like.

Table of Contents

What Is Square Actually Built to Do?

Why Are Small Business Receivables a Different Problem?

What Are the Five Gaps in Square's Payment Architecture?

What Does This Mean for CFOs and Finance Leaders?

What Do the Recovery Economics Actually Look Like?

What Is Skip-A-Pay and Why Can't Square Offer It?

How Did Enamel Dentistry Resolve 90% of 120+ DPD Accounts?

Square vs. FinanceOps Agentic AI: Which Solves Collections?

Why Is 1.5% the Only Aligned Collections Pricing Model?

Key Takeaways

FAQs

What Is Square Actually Built to Do?

Square deserves its reputation. It democratized payment processing for small businesses that previously could not afford the hardware, the contracts, or the technical complexity of enterprise payment infrastructure. A dental practice, a healthcare clinic, a local utility provider, a small lender. Square gave all of them a frictionless way to accept payment at the point of service.

Every element of Square's product is built around one foundational assumption: the customer has decided to pay and needs a convenient, reliable mechanism to do so. That assumption holds perfectly for the moment of sale. It breaks completely the moment an account goes delinquent.

When a patient misses a payment, when a utility customer stops paying, when a borrower becomes 30 days past due, the problem is no longer a payment acceptance problem. It is a collections recovery problem. The customer has not decided to pay. The reason they stopped matters enormously. The outreach that re-engages them is governed by federal law. The payment structure that produces completion must be calibrated to what they can actually sustain.

Square's payment links do not adapt to hardship signals. Its digital invoices do not read sentiment. Its compliance infrastructure was built for PCI DSS payment security, not FDCPA contact frequency limits or TCPA consent enforcement. This is not a criticism of Square. It is a precise description of a problem Square was not designed to solve.

Why Are Small Business Receivables a Different Problem?

The organizations most likely to be using Square, healthcare practices, dental offices, local service businesses, small lenders, and utilities, share a specific receivables challenge that makes the gap between payment acceptance and collections recovery especially consequential.

Their delinquent accounts are disproportionately small-balances: Traditional collections agencies charge 25 to 40% of recovered balances, making small-balance recovery structurally unworkable. A $200 dental balance at 35% contingency produces $70 for the agency and $130 for the practice. After administrative overhead, writing the account off becomes the easier business decision. The write-offs compound until the accumulated loss becomes invisible and normalized.

Their customer relationships are ongoing: A dental practice that damages a patient relationship through aggressive collections outreach does not just lose the recovery. It loses all future revenue from that patient. The collections process must preserve the relationship, not just recover the balance. No point-of-sale platform was designed with that constraint as a governing requirement.

Their compliance exposure is real and accelerating: According to the Consumer Financial Protection Bureau's Annual Debt Collection Report, the CFPB received approximately 207,800 debt collection complaints in 2024, nearly double the 109,900 received in 2023. Healthcare and utility receivables are not exempt from FDCPA and TCPA requirements. A dental practice sending repeated automated payment reminders without proper consent management is not protected by its size or its industry.

What Are the Five Gaps in Square's Payment Architecture?

Gap 1: Does Square Have Behavioral Intelligence for Delinquent Accounts?

Square was not designed to know why a customer stopped paying. It cannot detect that a patient has opened a payment link three times this week without completing the transaction, the single clearest signal that a restructured payment option would close the gap. It cannot distinguish that account from one where the customer has stopped all engagement entirely.

FinanceOps Agentic AI builds an account-level behavioral profile before any outreach begins. It analyzes payment history, channel responsiveness, engagement patterns, and real-time behavioral signals at the individual account level, producing a 12 to 15% right-party contact rate against the 2% industry norm.

Gap 2: Does Square Adjust Tone Based on Customer Sentiment?

Square's invoicing and payment reminder architecture sends the same message on the same schedule regardless of what the customer has communicated. There is no sentiment layer, no mechanism to detect hardship cues, adjust tone, or redirect a high-stress interaction toward a flexible resolution path before the customer disengages entirely.

FinanceOps Agentic AI applies real-time sentiment analysis across every channel in every interaction. A customer signaling financial stress receives empathetic, flexibility-first communication. A customer signaling avoidance receives a different approach entirely. The system responds to what each customer is actually communicating, not to a fixed schedule.

Gap 3: Does Square Maintain Context Across Channels?

A customer who receives a Square payment reminder via email, calls to explain their situation, and then receives another automated reminder the following week has been told three separate times that the organization was not listening. In healthcare and service environments, that experience does not feel like a system failure. It feels like organizational indifference. The payment does not happen. The relationship ends.

FinanceOps Agentic AI maintains a single unified conversation record across SMS, email, Voice AI, webchat, and self-service portals. The context never resets. The resolution path stays open across every channel switch.

Gap 4: Does Square Enforce FDCPA and TCPA Compliance?

Square's compliance infrastructure was built for PCI DSS, the standard governing secure payment processing. That standard has zero relevance to collections compliance.

The FCC Revoke All rule, effective April 2026, requires a single consent revocation through any channel to immediately halt all outreach across every channel simultaneously. For organizations using automated payment reminders without centralized consent management, every contact made after a revocation event in a different channel is potential TCPA exposure with statutory damages attached.

FinanceOps Agentic AI encodes FDCPA, TCPA, CFPB Regulation F, and FCC Revoke All as structural workflow properties before the platform contacts any account. Consent revocation propagates immediately across all channels. Every interaction is timestamped and audit-ready automatically.

Gap 5: Does Square Price on Recovery Outcomes?

Square charges 2.6% plus $0.10 on every transaction whether or not the delinquency rate improves. A dental practice that doubles its recovery rate pays Square exactly the same amount as one whose write-offs compound every quarter. Square's revenue is entirely disconnected from collections performance because collections performance was never the output Square was designed to produce.

FinanceOps Agentic AI charges 1.5% of collections recovered. No upfront cost. No subscription. Zero fee if no recovery occurs.

What Does This Mean for CFOs and Finance Leaders?

Collections infrastructure is a balance sheet decision. Every delinquent account that ages past 90 days without resolution represents not just a missed recovery, but a compounding working capital cost.

For CFOs evaluating Square against FinanceOps Agentic AI, the question is not which platform has better payment features. The question is which platform reduces reserve requirements, accelerates cash conversion, and protects the organization from regulatory exposure simultaneously.

Square's architecture addresses none of those three outcomes for delinquent accounts. It was built for payment volume, not recovery performance. Its fee structure confirms that. A vendor charged on transaction volume has no institutional reason to improve your aging report.

FinanceOps Agentic AI addresses all three.

Reserve reduction follows directly from earlier-stage account resolution.

Cash acceleration follows from 2 to 3 week recovery windows replacing 90 to 120 day agency timelines.

Regulatory protection follows from structural FDCPA, TCPA, and CFPB compliance enforcement encoded before first contact. And all of it comes at 1.5% of what is actually recovered.

What Do the Recovery Economics Actually Look Like?

The economics that made small-balance recovery unworkable through traditional channels become entirely different at 1.5% of collections recovered.

Recovery Model | $50,000 Portfolio at 70% Recovery | Fee | Net Recovery |

Write-off | $0 recovered | $0 | $0 |

Traditional agency at 35% | $35,000 recovered | $12,250 | $22,750 |

FinanceOps at 1.5% | $35,000 recovered | $525 | $34,475 |

On a single $50,000 small-balance portfolio, FinanceOps produces $11,725 more in net recovery than a traditional agency at 35%, in 2 to 3 weeks instead of 90 to 120 days, with zero upfront cost and zero fee if nothing is recovered.

At the individual account level, a $200 dental balance recovered through FinanceOps costs $3 in platform fees. The same recovery through a traditional agency at 35% costs $70 and takes four months. The practice nets $197 from FinanceOps versus $130 from an agency, in a fraction of the time.

These are not incremental improvements in recovery economics. They are the difference between a recoverable portfolio and a normalized write-off line.

See what FinanceOps recovers on your first 10,000 accounts, free, no upfront cost, no subscription.

What Are Flexible Payment Plans and Why Can't Square Offer Them?

Flexible Payment Plans Powered by FinanceOps Agentic AI

Flexible Payment Plans is the single clearest illustration of what separates payment acceptance infrastructure from collections recovery architecture. It is also the capability that most directly prevents the outcome every small business and healthcare organization is trying to avoid: a customer who cannot pay this month becomes an account that is never recovered.

What happens inside Square's architecture when a customer cannot make a payment:

A payment link goes unclicked. An invoice ages past due. A reminder goes out on day seven, another on day fourteen. If no payment occurs, the account moves into manual follow-up or gets written off. Square has no mechanism to assess why a customer hasn't paid or what they can realistically afford. It was designed to process payments from customers who have already decided to pay, not to work with those who are struggling.

What FinanceOps Agentic AI's Flexible Payment Plans do:

Agentic AI evaluates each customer's actual repayment capacity by analyzing historical payment behavior, income and expense signals, sentiment indicators, transaction patterns, and financial stress cues. Based on this analysis, it recommends structured, realistic payment schedules, including weekly, bi-weekly, monthly, or custom installment-based plans, tailored to what the customer can genuinely sustain.

The account stays current. No late fees are incurred. No relationship damage occurs. Because the plan is matched to actual affordability rather than a fixed default schedule, customers are far more likely to stick with it, improving long-term liquidation rates while reducing roll rates and defaults.

An account that would have aged into 60+ day delinquency and been written off stays current. A patient who would have disengaged because the platform had no answer for their situation remains a patient. The relationship holds. The revenue is recovered. No payment acceptance platform produces that outcome.

How Did Enamel Dentistry Resolve 90% of 120+ DPD Accounts?

Enamel Dentistry represents the proof case for every small business and healthcare organization currently managing small-balance delinquent accounts through Square invoices and payment links.

A healthcare practice with small-balance delinquent accounts that were economically impossible to recover through traditional means. Agency fees that exceeded the recovered value. Manual follow-up that consumed staff time. Patient relationships that could not survive aggressive outreach. Enamel Dentistry deployed FinanceOps Agentic AI against exactly this problem.

90% reduction in 120+ DPD small-balance accounts.

$100,000+ saved from reduced agency fees.

70% increase in payment response rates.

Recovery window compressed from 120+ days to 2 to 3 weeks.

60% operational cost reduction. 100% HIPAA-compliant workflows throughout every interaction.

The economics that made agency-based recovery unworkable for small-balance healthcare accounts became entirely viable at 1.5% of recovered balances. The patient relationships that could not survive aggressive collections outreach were preserved through empathetic, sentiment-adaptive communication calibrated to what each patient was actually communicating.

The 120-day recovery window compressed to 2 to 3 weeks. Not because FinanceOps applied more pressure. Because it applied the right approach at the right moment through the right channel to the right person. Which is precisely what a payment acceptance platform was never designed to do.

Every dental practice, healthcare clinic, and small business managing delinquent accounts with Square invoices is sitting on a recoverable portfolio that current economics make invisible. The Enamel Dentistry result makes that portfolio visible and recoverable.

Square vs. FinanceOps Agentic AI: Which Solves Collections?

Capability | Square | FinanceOps Agentic AI |

Purpose | Payment acceptance | Delinquent account recovery |

Behavior & Sentiment Intelligence | Not designed for collections | Real-time, per account, live across all channels |

Outreach Channels & Context | Email, payment links | SMS, email, Voice AI, webchat, portals; full context maintained |

Skip-A-Pay & Recourse | Not available | Full capability, credit risk assumed, full balance paid upfront |

Affordability-Based Plans | Not available | Calibrated to actual repayment capacity |

PTP Abandonment | 38–45% industry average | Under 20% |

Compliance | Not designed for collections | FDCPA, TCPA, CFPB Reg F, FCC Revoke All enforced before first contact; HIPAA across healthcare deployments |

Right-Party Contact Rate | Not tracked | 12–15% vs 2% industry norm |

Cost & Efficiency | Manual AR & follow-up; 2.6% + $0.10 per transaction | Under 10 minutes/day; as low as $3.65 per recovery; 1.5% of recovered balances; nothing if nothing is recovered |

Resolution & Audit | Manual, no automation | Average resolution 2–3 weeks; audit-ready documentation at every touchpoint |

This is not a comparison between two competing products serving the same problem. It is a comparison between a payment acceptance platform built for willing customers and a collections recovery platform built for delinquent ones.

Why Is 1.5% the Only Aligned Collections Pricing Model?

The pricing model of a vendor is the most direct available signal of what that vendor was built to produce.

Square charges on transaction volume. Whether the delinquency rate improves or worsens, whether the aging report gets better or worse each quarter, Square's fee is identical. Its roadmap serves merchants managing payment authorization. The aging report is not its problem to solve, and its pricing model confirms that.

FinanceOps Agentic AI charges 1.5% of collections recovered. No upfront cost. No subscription. No fee if no recovery occurs. FinanceOps absorbs all platform and outreach costs on accounts that do not recover. The first 10,000 accounts are processed free.

FinanceOps Agentic AI

The 1.5% model also creates a vendor whose institutional incentives are directly aligned with preserving the patient or customer relationship. Aggressive collections outreach that produces a complaint, a churn event, or an FDCPA violation costs FinanceOps recovery revenue on every future billing cycle with that account. Its incentive structure is calibrated toward empathetic, effective recovery, not maximum pressure applied to every account regardless of signal.

That alignment is the most important structural proof of a collections recovery platform. And it is a feature that never appears on a payment processor's product page.

Key Takeaways

Square was built for payment at sale, not for delinquency. Once a customer stops paying, its architecture cannot recover accounts.

Small-balance accounts in healthcare and services are uneconomical to recover with traditional agencies charging 25–40%. FinanceOps collects at 1.5%, making recovery viable in 2–3 weeks.

Affordability-based plans turn customers who can’t pay today into recovered accounts, while Square only resends invoices. FinanceOps covers the balance, assumes credit risk, and collects in installments.

FCC Revoke All compliance requires halting outreach immediately after consent revocation. Square lacks centralized enforcement; FinanceOps encodes it structurally before any contact.

Enamel Dentistry results: 90% reduction in 120+ DPD accounts, $100,000+ saved on agency fees, recovery window compressed to 2–3 weeks, and 100% HIPAA-compliant.

Ready to See What Recovery Architecture Delivers for Your Portfolio?

Book a free 20-minute demo with FinanceOps Agentic AI. Your delinquent accounts, healthcare receivables, and charge-off trends mapped against what behavioral intelligence, Skip-A-Pay, payment plans, and compliant autonomous outreach deliver in your portfolio.

No upfront cost. No subscription. 1.5% of collections recovered. You pay only when your customers pay.

FAQs

Can Square collect overdue invoices and recover delinquent accounts?

Square was designed to process payments from customers who have decided to pay. Its invoicing and payment reminder functionality resends the same payment request on a schedule and was not designed to analyze why a customer stopped paying, adjust outreach tone based on hardship signals, offer an alternative payment structure, or enforce FDCPA compliance at the account level. For genuinely delinquent accounts, Square's architecture produces repeated invoice sends and eventually a write-off. FinanceOps Agentic AI was built specifically for delinquent account recovery.

Does Square offer payment plans for delinquent customers?

No. Square's architecture has one payment structure: the invoice amount. It was not designed to evaluate affordability, propose installment schedules, or calibrate a payment structure to what a specific customer can actually sustain. FinanceOps Agentic AI evaluates repayment capacity from payment history, income signals, and live sentiment before proposing any plan, reducing promise-to-pay abandonment from the 38 to 45% industry average to under 20%.

Can Square recover delinquent accounts for dental and healthcare practices?

Square was not designed for healthcare collections recovery. It does not offer HIPAA-compliant collections workflows, behavioral intelligence for delinquent patient accounts, or affordability-based payment plans. FinanceOps Agentic AI operates with 100% HIPAA-compliant workflows across every healthcare deployment, as demonstrated in the Enamel Dentistry case study where 90% of 120+ DPD accounts were resolved in 2 to 3 weeks.

What is Skip-A-Pay and why was Square not designed to offer it?

Skip-A-Pay allows FinanceOps to cover a customer's outstanding balance on their behalf when they cannot pay today, keeping the account current and avoiding late fees or relationship damage. FinanceOps collects repayment in three manageable installments while assuming the credit risk entirely. Square's architecture was designed to process authorized payments and was not built to cover customer obligations, assume credit risk, or collect repayment through installments.

Square vs collections software: which is right for overdue accounts?

Square is the right tool for payment acceptance at the point of sale. A collections software platform like FinanceOps Agentic AI is the right tool for recovering overdue accounts where the customer has stopped paying. These are structurally different problems requiring different data models, different compliance frameworks, and different pricing structures. For organizations managing aging receivables, Square's architecture was not designed to produce recovery outcomes.

How does 1.5% of collections compare to what small businesses currently pay?

Traditional collections agencies charge 25 to 40% of recovered balances with no guarantee of recovery and a process that typically takes 90 to 120 days. On a $50,000 small-balance portfolio with a 70% recovery rate, a traditional agency at 35% charges $12,250. FinanceOps charges $525 on the same recovery, with results delivered in 2 to 3 weeks and zero fee if no recovery occurs. The first 10,000 accounts are processed free.

Does Square offer any debt collection or delinquent account recovery capability?

No. Square is a payment acceptance platform. It was not designed to offer behavioral intelligence for delinquent accounts, sentiment-adjusted collections outreach, Skip-A-Pay, affordability-based payment restructuring, FDCPA or TCPA compliance governance at the account level, or any pricing model tied to delinquent account recovery outcomes. These capabilities require a platform built specifically for collections recovery.

6 minutes

Posted by

Arpita Mahato

Content Writer

Other Blogs

View other blogs

Stay Updated with Us

Enter your email below and subscribe to our weekly newsletter

Instant Access

Boost Productivity

Easy Setup

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps