Blog Summary

A monthly statement is a periodic summary of an account's activity: outstanding balance, payment history, accrued fees, and the next due date.

It is not optional paperwork. It is the single most consistent touchpoint in the debt collection process, and most debtors cure within 30–45 days when it's used correctly.

Timing soon transforms from a soft consideration, to becoming an operational liability. A $2.875 million proposed TCPA settlement against Farmers Insurance Exchange is a real-world reminder that outreach sent to the wrong people at the wrong time doesn't just miss a payment window, it creates legal exposure.

Miss a company's accounts-payable check run by a day, and the next available payment window can be an entire month later.

The same statement that drives cash flow also builds the compliance paper trail courts rely on if the account ever escalates to litigation.

Agentic AI removes the manual bottleneck entirely, generating, timing, and delivering statements automatically based on each debtor's actual behavior, not a fixed calendar date.

Most creditors treat the monthly statement like paperwork, something that goes out because compliance requires it, not because it's doing any real work. That's backwards. A statement sent on the wrong day in the wrong format is a missed cure. A statement sent on the right day, formatted to be acted on immediately, is often the entire difference between a 30-day resolution and a 90-day write-off candidate.

The stakes are higher than most creditors assume. Debt collection was the second most-complained-about consumer financial product category in 2025, with approximately 387,400 complaints filed with the CFPB, an 86% increase over 2024. A meaningful share of that volume traces back to confusion over what's owed and when, exactly the ambiguity a clear, well-timed monthly statement is supposed to prevent.

Monthly Statement Definition

A monthly statement is a periodic summary of an account's financial activity: the outstanding balance, payment history, accrued fees, and the next due date, issued to a debtor on a recurring basis. It's sometimes called a monthly billing statement, a statement of account, or simply a collection statement, depending on the industry, but the function is the same: it tells the debtor exactly where the account stands and what's expected next.

That's the dictionary answer. The rest of this article is about why getting the timing of that document right matters more than almost anything else in the recovery process.

What Is a Monthly Statement in Debt Collections?

In a collections context, a monthly statement isn't just an account summary. It's the primary instrument through which a creditor maintains legal standing, documents the debt's history, and keeps the debtor oriented toward payment. A generic billing statement tells someone what they owe. A collections statement tells them what they owe, what happens if they don't act, and exactly how to resolve it.

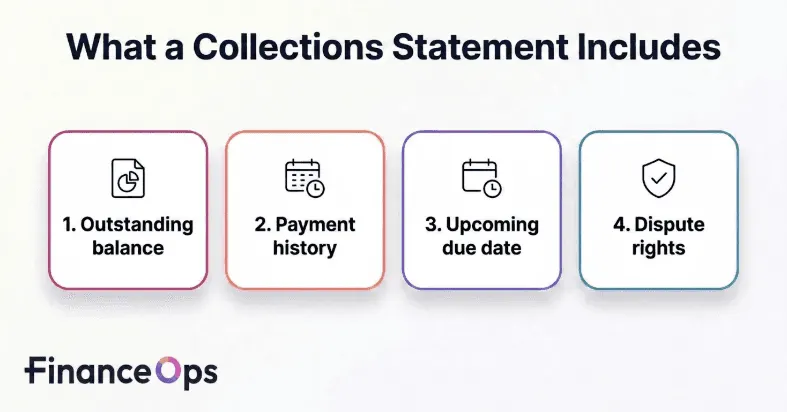

That distinction matters because collections statements carry compliance obligations that standard billing doesn't. A properly built collections statement includes:

Outstanding balance: The total unpaid amount, broken into principal, accrued interest, and fees, not just one lump figure.

Payment history: Exact dates of past payments and how any partial payments were allocated.

Upcoming due date: A clear deadline for the next payment, stated plainly enough that there's no room to claim confusion later.

Dispute rights: Instructions on how and when the debtor can formally dispute the debt in writing.

That last component matters more than most creditors give it credit for. A statement that omits dispute rights isn't just incomplete, it's a compliance gap waiting to surface at the worst possible time, usually mid-litigation.

Monthly Statement vs. the Broader Debt Collection Process

It helps to be precise about where a monthly statement sits inside the larger debt collection process, because the two get conflated constantly.

The statement is one input into the process, not the process itself. But it's a disproportionately important one, because it's usually the first document a debtor actually reads in full, before any phone call, before any escalation letter.

Why Timing Matters More Than Most Creditors Realize

The cost of non-compliance isn't theoretical. The National Law Review recently reported a $2.875 million proposed TCPA settlement against Farmers Insurance Exchange, over allegations that marketing messages reached consumers already registered on the National Do Not Call Registry, is a reminder that the regulatory clock runs whether or not your statement process does. Timing, in other words, becomes a liability instead of a recovery lever.

Early intervention compounds: Sending a clear, consistent statement immediately after a missed payment maximizes the chance of a quick cure. Most debtors who are going to pay voluntarily do so within 30–45 days of consistent outreach, not after months of silence followed by a harsher letter.

Company check runs don't wait for you: Here's the part most explainers skip entirely: many corporate debtors process accounts payable on a strict, once-a-month cycle. If your statement lands even one day after that cycle closes, the next available payment window isn't next week, it's an entire month away. A statement that's accurate but late can cost you 30 days of recoverable time for no reason other than bad timing.

Validation and compliance run on clocks too: Debt collectors are required to provide a validation notice either in the initial communication or within five days of it, under FDCPA Section 809(a) and Regulation F (12 CFR § 1006.34). Statements issued on a clear, documented schedule support that paper trail and demonstrate the account is being handled within the lines, and not as an afterthought.

TCPA applies to marketing outreach, not just collection calls: Consumers can pursue statutory damages for unsolicited texts or calls, even when those messages originate from an affiliated agency rather than the creditor directly. Two or more unsolicited marketing messages to a number on the Do Not Call Registry can be enough to trigger a claim. The exposure compounds quickly at scale, and most creditors don't discover the gap until it's already a litigation problem.

Litigation depends on the chronology being clean: If a debtor refuses to pay and the account goes to court, judges and arbitrators rely heavily on the clarity and consistency of chronological account statements to establish that the debt was genuinely, provably overdue. A messy or inconsistent statement history weakens a case that would otherwise be straightforward.

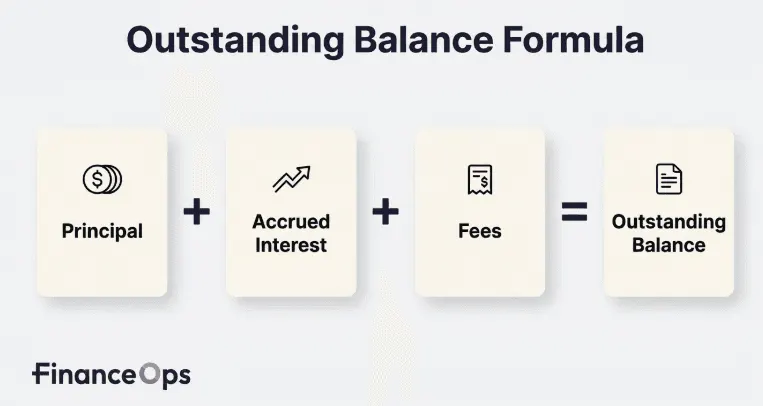

Outstanding Balance: The Number That Has to Be Right

Every other component of a monthly statement exists to support one figure: the outstanding balance. Get this number wrong, even slightly, and it doesn't just create a billing error, it gives the debtor a legitimate basis to dispute the entire statement. The formula is straightforward:

But straightforward doesn't mean forgiving. Each component has to be visible, accurate, and current:

Principal, the original unpaid amount, unchanged by interest or fees applied after the fact.

Accrued Interest, calculated transparently, with the rate, start date, and compounding method disclosed. A number without a method behind it is a dispute waiting to happen.

Fees, itemized line by line, not bundled into a single unexplained figure. A debtor who can't see what they're being charged for will question everything else on the statement too.

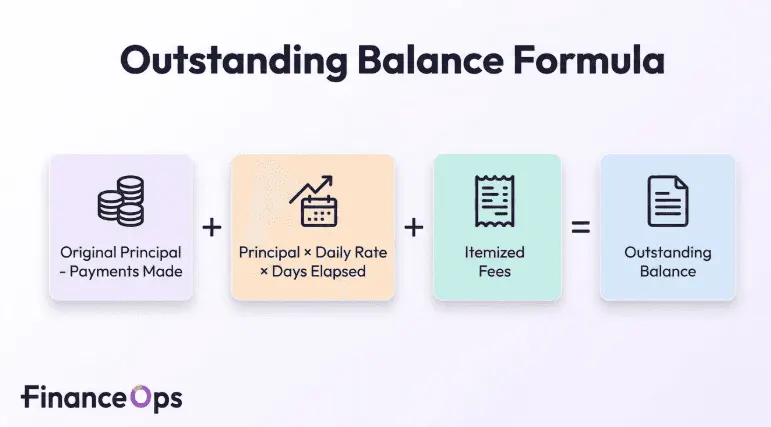

A further breakdown that holds up in court looks like this:

Outstanding Balance = (Original Principal − Payments Made) + (Principal × Daily Rate × Days Elapsed) + Itemized Fees

This is also where most manual processes quietly fail. A spreadsheet-driven statement process that updates balances weekly or biweekly, rather than in real time, will eventually issue a statement with a stale number, right around the time a debtor is deciding whether the creditor's records can be trusted at all. At that point, the accuracy problem becomes a credibility problem, and credibility problems stall recoveries that should have been straightforward.

Debt Collection Strategies to Speed Up Payments

A monthly statement works best as part of a broader, deliberate cadence rather than as an isolated document. The strategies that move payments faster, beyond the statement itself, include:

Reviewing your billing dates and procedures: Make sure statements go out on a fixed, predictable schedule, not whenever the queue clears.

Segmenting by days-past-due: A 15 DPD account and a 75 DPD account should not receive the same tone or the same channel.

Using multiple channels in sequence: Email, SMS, VoiceAI calls, and portal notifications sent within the same window increase the odds of reaching the debtor before the next check run closes.

Embedding the payment action directly in the statement: A statement that requires a debtor to go find a portal, log in, and locate an invoice number is a statement that gets deprioritized.

Following the 7×7 rule where applicable: A common collections heuristic, attempt contact seven times across the first seven days of delinquency, frontloading outreach when the cure probability is highest rather than spreading attempts thin over a month.

None of these strategies is complicated on its own. What's hard is doing all of them, consistently, across every account in a portfolio, without the process quietly drifting back to "send it when someone gets to it."

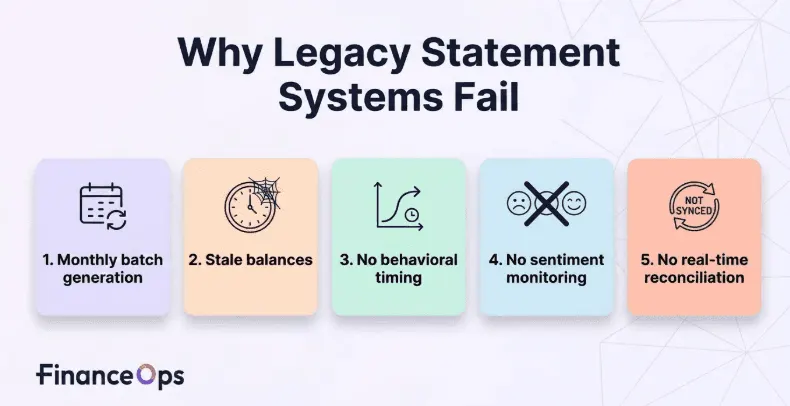

Why Legacy Statement Systems Fail

Before getting to what Agentic AI changes, it's worth being specific about what it's replacing. Most collection statement processes today, even at well-run organizations, share the same structural weaknesses:

Monthly batch generation: Statements go out in one scheduled run, regardless of where each individual debtor actually is in their payment cycle or check-run timing. The batch is convenient for the back office and arbitrary for everyone receiving it.

Stale balances: A balance pulled from a system that syncs daily, weekly, or on a manual schedule is already out of date by the time the statement reaches the debtor, especially if a payment is posted in between.

No behavioral timing: A fixed calendar date treats every debtor identically, ignoring the fact that some respond best to a Tuesday morning email and others only engage after a Friday SMS.

No sentiment monitoring: A debtor who's communicated financial hardship gets the same tone and the same statement as one who's simply been unresponsive, which is how legitimate hardship cases turn into complaints.

No real-time reconciliation: Disputes, partial payments, and corrections get resolved on a delay, which means the next statement can repeat an error the debtor already flagged.

None of these are AI problems. They're infrastructure problems, and they're exactly why "automating the statement" usually just means automating the batch job, not fixing what was broken about the batch job in the first place.

Where Agentic AI for Monthly Statements Changes the Math

This is the part that actually separates a modern collections operation from a legacy one. A human-run statement process has a structural ceiling: someone has to remember to generate it, check the balance, pick the right channel, and send it before the deadline that matters, every single month, across every account. That ceiling is exactly where accounts slip through.

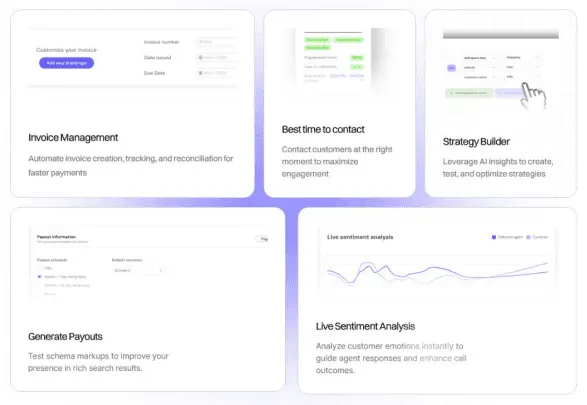

FinanceOps Agentic AI doesn't just speed up the manual steps underneath that ceiling, it removes it. The statement becomes one output of six mechanisms working together, not a standalone document someone has to remember to produce.

Best time, best channel, best person to contact: The system analyzes behavioral patterns, repayment history, and engagement signals to determine when each debtor is most likely to engage, which channel they actually respond to, and the real decision-maker on the account, payer versus contact-of-record. This is what closes the check-run gap: a statement timed against real behavior is far less likely to land a day too late.

Live sentiment analysis: Every statement-related interaction, a reply, a portal login, a missed acknowledgment, is scored for tone, hardship cues, and payment intent in real time. Follow-up adjusts accordingly: more supportive when a debtor signals genuine financial stress, more direct when they're simply avoiding contact. A statement with the wrong tone attached gets ignored or disputed.

Two-way, omnichannel, multilingual communication: A debtor who opens a statement by email and follows up by SMS or through a portal stays in the same conversation, no repeated questions, no lost context. Native multilingual support means the statement is genuinely understood, not just technically delivered, across a diverse portfolio.

User-controlled strategy builder: Collections teams define the rules, cadence, tone thresholds, segmentation, escalation triggers, and compliance limits under TCPA, FDCPA, and Regulation F. The AI executes inside those boundaries with zero deviation, and every decision is timestamped and auditable. The strategy stays human-authored; only the execution scales.

Affordability-based flexible payment plans: When a statement prompts a response but the debtor can't pay in full, the system evaluates actual repayment capacity, payment history, income signals, sentiment, transaction patterns, and proposes a structure the debtor can realistically sustain. A plan built on a stale balance isn't a recovery; this is why real-time accuracy matters here too.

Automated invoice and statement management: The full lifecycle, issuance, behaviorally-timed reminders, retry logic, reconciliation, dispute routing, and audit-ready compliance logging, runs as one closed system. Every balance reflects the ledger at the moment it's generated, and the same logging builds the chronological paper trail courts rely on if an account ever escalates.

Put together, the statement stops being a static document that gets mailed and forgotten. It becomes a live checkpoint inside a continuously running recovery workflow.

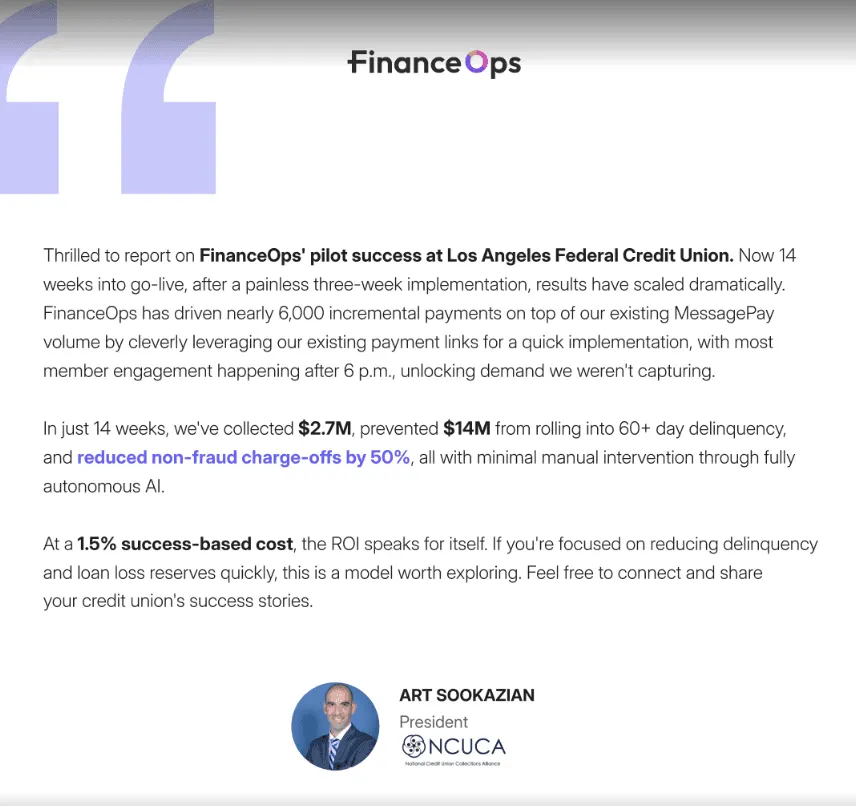

In a 14-week pilot, FinanceOps' Agentic AI collected $2.7M for LAFCU, prevented $14M from rolling into 60+ day delinquency, and reduced non-fraud charge-offs by 50%, almost entirely through autonomous AI with minimal manual intervention, at a 1.5% success-based cost. That's the kind of outcome a well-timed, behaviorally-aware statement process is built to produce at scale.

Key Takeaways

A monthly statement is a recovery tool, not paperwork. Treating it as an administrative formality is what causes accounts to drift past their cheapest recovery window.

Timing is mechanical, not cosmetic. Missing a check-run cycle by a single day can cost a full month of recoverable time, regardless of how accurate the statement itself is.

Compliance risk doesn't just come from collection calls. TCPA exposure extends to any unsolicited marketing outreach, including texts sent through affiliated agencies. Two messages to a number on the Do Not Call Registry can be enough to trigger a claim.

A clean chronological statement of history is your first line of defense. In disputes and litigation, judges rely on it to establish that the debt was genuinely overdue, and gaps in that record weaken cases that should be straightforward.

Manual statement processes have a structural ceiling. Agentic AI removes it by tying generation, timing, and channel selection to actual debtor behavior instead of a fixed calendar.

FinanceOps Agentic AI identifies timing gaps, behavioral patterns, and missed recovery opportunities across your portfolio, then automatically delivers statements, reminders, and follow-up actions at the moments most likely to drive payment.

Talk to a FinanceOps expert or book a quick demo to see how behaviorally timed monthly statements can accelerate recoveries across your portfolio, from day 1.

No upfront cost. Performance-based pricing at 1.5%. You pay only on successful collections.

FAQs

1. What is a monthly statement in debt collections?

A monthly statement is a periodic, formal summary of an account's activity: the outstanding balance, payment history, accrued fees, and the next due date. It's sent to keep the debtor informed, document the account's status over time, and give them a clear, dated record they can act on or dispute.

2. Are monthly statements legally required?

Not in every case, but they're strongly recommended, and in many situations expected, under regulations like the FDCPA. A statement that consistently discloses the balance, due date, and dispute rights builds the compliance paper trail a creditor needs if an account is ever challenged or escalated to litigation.

3. How does debt collection work?

It typically moves through escalating stages: an initial reminder or statement when a payment is first missed, then more direct contact as the account ages, then formal demand or settlement attempts, and, if it remains unresolved, referral to a third-party collector or legal action. A monthly statement is usually the first and most consistent touchpoint in that sequence.

4. What is the 7×7 rule of collection?

It's a common industry heuristic recommending seven contact attempts within the first seven days of delinquency, frontloading outreach during the window when a debtor is statistically most likely to cure voluntarily. The logic mirrors why statement timing matters: the earlier and more consistently a creditor reaches out, the cheaper and more likely the recovery.

5. What are the best debt collection strategies to speed up payments?

Consistent billing schedules, segmenting accounts by days-past-due, using multiple contact channels within the same window, and embedding the payment action directly in the statement all measurably shorten time-to-payment. None of these work in isolation; they compound when applied together and applied consistently across an entire portfolio.

6. Can monthly statements be delivered digitally?

Yes. Email, SMS, and online portal delivery are all standard today, and digital delivery is generally faster and more cost-effective than mail. The bigger factor isn't the channel itself, it's whether the channel and timing match how that specific debtor actually engages.

7. How does Agentic AI improve monthly statements in debt collections?

By generating statements from live ledger data, timing delivery around each debtor's actual behavior and payment cycles, adjusting tone based on real-time sentiment, and automatically escalating unacknowledged accounts. This removes the manual bottlenecks. late timing, stale balances, generic tone, that cause statements to underperform.

8. How is the outstanding balance on a collection statement calculated?

The defensible formula is: Outstanding Balance = (Original Principal − Payments Made) + (Principal × Daily Rate × Days Elapsed) + Itemized Fees. Each component needs to be visible and current, principal unchanged by post-facto adjustments, interest disclosed with its rate and method, and fees listed line by line rather than bundled. A stale or opaque balance doesn't just create a billing error; it gives the debtor a legitimate basis to dispute the entire statement.

9. What is the TCPA, and how does it affect debt collection outreach?

The Telephone Consumer Protection Act regulates unsolicited calls and text messages, including marketing outreach sent by or on behalf of creditors. It's not limited to collection calls, any promotional message sent to a consumer whose number is on the National Do Not Call Registry can trigger liability. Two or more such messages within a 12-month period may be enough to support a claim, even if those messages were sent through an affiliated agency rather than the creditor directly. Creditors who don't audit their outreach practices at the agency level often don't discover the exposure until it's already a litigation problem.