Adyen is one of the most sophisticated payment processors ever built. It is not a collections platform. And every receivables team that has tried to use payment infrastructure in place of recovery intelligence has the aging report to prove it.

The gap your team is experiencing is not a configuration problem. It is an architecture problem. And it has a specific fix.

Blog Summary

Adyen was built to move authorized payments, not recover accounts where consumers have stopped paying. The moment a consumer goes delinquent, Adyen's entire intelligence stack has nothing to work with.

High-risk consumer receivables require behavioral intelligence, sentiment-adaptive outreach, structural compliance governance, and a pricing model tied directly to recovery outcomes, none of which any payment processor provides.

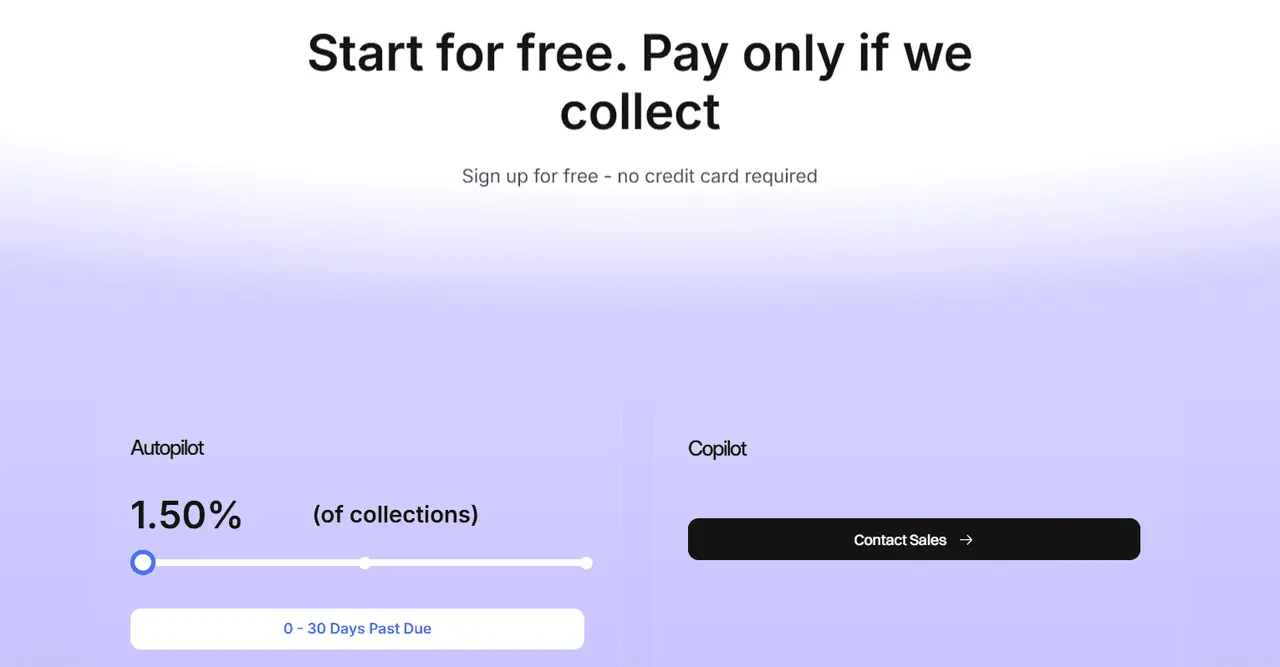

FinanceOps Agentic AI was built specifically for this problem. It charges 1.5 percent of collections recovered and zero if nothing is collected.

What Adyen Was Actually Built to Do

Adyen is exceptional at the problem it was built to solve. That problem is not collections. Adyen's entire infrastructure rests on one foundational assumption: the consumer intends to pay. Every algorithm, every optimization, every retry logic exists to move a willing payment from point A to point B at the highest possible success rate. In practice, that looks like this:

Unified Commerce platform connects in-store, online, and mobile payment channels into a single payment processing infrastructure.

RevenueAccelerate optimizes authorization rates using machine learning trained on billions of transactions across card issuers, geographies, and payment methods.

Network token management keeps payment credentials current to reduce involuntary card failures.

Intelligent payment routing selects the optimal processing path per transaction to maximize approval probability.

RevenueProtect identifies fraud signals interrupting legitimate payment attempts and routes around them.

The moment a consumer has stopped wanting to pay, or cannot pay, every one of these capabilities becomes irrelevant. There is no behavioral signal for why the consumer stopped. There is no outreach capability to re-engage them. There is no compliance framework for contacting a delinquent account. There is no mechanism to propose an alternative payment structure. The account simply ages.

That is not a flaw in Adyen's engineering. It is a precise description of a problem Adyen was never designed to solve.

Why High-Risk Consumer Receivables Are Structurally Different

The most important distinction in receivables recovery is one most payment teams misunderstand: a failed payment and a delinquent account are not the same problem, and they do not have the same solution.

A failed payment is a technical interruption of a consumer's intent to pay. The card expired. An auto-pay parameter broke. Insufficient funds on a billing date. The payment method failed, not the payment intent. Adyen's retry logic and network tokenization were built precisely for this scenario.

A delinquent account means the consumer has stopped paying, and the reason matters enormously:

Genuine financial hardship requires empathetic, flexibility-first outreach with an affordable restructured payment option

A billing dispute requires a structured resolution path, not a payment demand

Life disruption requires timing sensitivity and channel flexibility

Active avoidance requires a different channel and tone entirely from what the consumer has already been ignoring

High-risk consumer receivables, accounts at 60 days, 90 days, and beyond, sit at the extreme end of this spectrum. These are accounts that have already survived standard early-stage outreach unchanged. The consumer has not responded. The balance has grown. The relationship has been strained. Recovery probability drops with every additional day of inaction.

According to ACA International's 2023 Collections Industry Benchmarking Report, acting in the first 1 to 30 days of delinquency recovers 85 percent of early-stage accounts. Waiting until 90 days or beyond drops recovery probability below 20 percent for most portfolio types. The window is not just shorter. The problem is structurally harder. And no payment processor was designed to address it.

The Five Ways Payment Processors Fail at Consumer Receivables Recovery

Failure 1: No Behavioral Intelligence for Delinquent Accounts

Adyen's machine learning was trained on authorized payment behavior. It has no model for what a delinquent consumer account communicates.

It cannot detect that a consumer opened the self-service payment portal three times this week without completing a transaction, a signal that almost certainly indicates a financial barrier rather than deliberate avoidance. It cannot distinguish that account from one where the consumer has made a conscious decision to stop paying. These distinctions are the difference between a recovery strategy that works and one that wastes every outreach attempt on the wrong approach.

FinanceOps Agentic AI analyzes payment history, device usage, channel responsiveness, engagement signals, and timing patterns at the individual account level before any outreach attempt is made. The first contact is already informed.

Failure 2: No Real-Time Sentiment Detection or Tone Adjustment

Adyen does not contact consumers. It processes payments. For collections teams relying on Adyen as their payment infrastructure, this means every consumer interaction, whether handled in-house or by a third-party agency, operates without intelligence about what that specific consumer is communicating in a given moment.

Deloitte's 2024 Financial Services AI Outlook found that sentiment-aware AI interactions reduce formal consumer complaints in collections environments by up to 35 percent and improve payment commitment rates by 22 percent. A consumer signaling financial hardship and a consumer who has been actively avoiding contact for six weeks require different responses. A blunt outreach instrument cannot tell them apart.

Failure 3: No Omnichannel Context Continuity

A consumer who receives an email about an overdue balance, calls in to discuss options, and follows up via SMS arrives at most payment environments as three separate, unconnected interactions. They re-explain their situation every time. At the exact moment payment intent is highest, after they have already reached out and expressed willingness to resolve, the infrastructure introduces maximum friction.

FinanceOps Agentic AI maintains a single unified conversation record across SMS, email, Voice AI, webchat, and self-service portals. Every channel switch is a continuation of the existing conversation. The consumer never repeats themselves. The resolution path stays open.

Failure 4: No Collections Compliance Framework

Adyen's compliance architecture was built for PCI DSS, the standard governing authorized transaction processing. PCI DSS has zero relevance to collections compliance.

FDCPA contact frequency limits, TCPA consent requirements, CFPB Regulation F documentation obligations, state-specific contact rules, and FCC Revoke All consent enforcement, which took effect in April 2026, all apply at the individual account level across every outreach channel simultaneously. Managing these manually at scale is precisely where audit gaps and regulatory exposure originate.

FinanceOps Agentic AI encodes every relevant compliance rule as a structural workflow property before the system contacts any consumer. Not tracked after the fact. Enforced before first contact, with timestamped audit documentation at every touchpoint.

Failure 5: No Performance-Aligned Pricing

Adyen charges on transaction volume. Whether your delinquency rate climbs or falls, whether your charge-off line grows or shrinks, the fee is identical. A platform paid on processing volume has no institutional reason to optimize your recovery rate. Its roadmap serves enterprise merchants managing payment authorization, not receivables teams managing aging portfolios.

FinanceOps Agentic AI charges 1.5 percent of collections recovered. If no collections occur, the fee is zero. That is not a marketing claim. It is the structural proof of a vendor whose revenue is contingent entirely on yours improving.

What High-Risk Consumer Receivables Recovery Actually Requires

Six capabilities define whether a recovery platform can actually move high-risk consumer accounts. Adyen provides none of them:

Account-level behavioral intelligence: Analysis of payment history, behavioral patterns, device usage, channel responsiveness, and real-time engagement signals at the individual account level, before the first outreach attempt is made

Live sentiment analysis: Real-time detection of tone, hardship cues, engagement likelihood, and compliance risk indicators across every channel, with automatic adjustment of outreach approach per interaction

Omnichannel context continuity: A single unified conversation record across SMS, email, voice, webchat, and self-service portals, so every channel switch continues the existing conversation rather than resetting it

Structural compliance governance: FDCPA, TCPA, state-specific contact rules, and FCC Revoke All consent enforcement encoded as workflow properties before first contact, not tracked retroactively

Flexible payment plans: A structured path for consumers who cannot pay today that preserves both the account balance and the consumer relationship rather than converting them into a write-off

Performance-aligned pricing: Vendor revenue tied directly to recovery outcomes, not platform usage or transaction volume

Flexible Payment Plans Built Around Actual Repayment Capacity

Promise-to-pay abandonment is one of the most expensive and least discussed problems in consumer receivables recovery. Industry averages run between 38 and 45 percent, meaning nearly half of every payment commitment made does not result in a completed payment.

The root cause is almost never bad intent. It is bad plan design. A payment plan structured around the balance owed rather than what the consumer can actually sustain is a plan that will fail, regardless of how committed the consumer felt during the outreach interaction. The gap between commitment and completion is where recovery revenue disappears.

Adyen retries authorized payment amounts. It has no mechanism to propose alternatives, assess affordability, or restructure an obligation into something the consumer can realistically complete.

FinanceOps Agentic AI evaluates actual repayment capacity before proposing any payment structure, drawing on payment behavior history, income and expense signals, real-time sentiment indicators from the current interaction, and transaction pattern data. The output is a realistic schedule calibrated to what this specific consumer can sustain, not a generic installment structure built for the median account:

Weekly installments for consumers managing tight cash flow windows

Bi-weekly installments aligned with paycheck timing

Monthly installments for consumers with irregular income

Custom installment structures for accounts with specific financial constraints

The result is PTP abandonment under 20 percent versus the 38 to 45 percent industry average. Every honored plan is a consumer relationship that survives the financial hardship intact. Every honored plan is revenue that does not require a write-off.

Real Results: In the Words of Pragas NanthaKumar, CEO and Co-Founder of FinanceOps Agentic AI

Pragas NanthaKumar has spent his career studying exactly where collections operations break down and why. Speaking at a live FinanceOps webinar, he identified the structural failure directly:

The LAFCU deployment is the clearest proof of what changes when the approach changes. A portfolio of late-stage accounts that legacy agencies had completely given up on was handed to the FinanceOps system. Within 21 days, LAFCU recovered over one million dollars at a 34 percent recovery rate, without adding a single headcount.

The LAFCU result is not an outlier. It is what happens when recovery architecture is designed around consumer psychology rather than collector convenience.

FinanceOps Agentic AI vs Adyen: Head-to-Head Comparison

This is not a feature gap that integration or configuration can close. Adyen and FinanceOps Agentic AI were built for structurally different problems. Attempting to use one in place of the other does not produce a suboptimal result for delinquent accounts. It produces no result at all.

Why 1.5 Percent of Collections Is the Only Pricing Model That Aligns Incentives

Most collections technology vendors are paid regardless of whether you recover anything. The subscription fee is identical whether your delinquency rate is 5 percent or 25 percent. That is not an accident of pricing. It is a structure of misaligned incentives built into every platform that charges before recovery occurs.

Adyen charges on transaction volume. Whether your receivables recovery rate is 20 percent or 70 percent, Adyen's revenue is unaffected. Its roadmap serves enterprise merchants optimizing payment authorization. Your aging report is not their problem to solve, and their pricing model confirms it.

FinanceOps Agentic AI charges 1.5 percent of collections recovered. No upfront cost. No subscription. No fee if nothing is recovered. Every dollar of FinanceOps revenue requires a dollar of your consumer account recovery to exist first.

What that means in practice:

On a $500,000 recovery, FinanceOps charges $7,500 and the net recovery is $492,500

A traditional agency at 35 percent on the same recovery takes $175,000, leaving $325,000

The difference is $167,500 on a single recovery cycle, and it compounds across every cycle in your portfolio

The contingency model also signals something beyond the math. A vendor willing to absorb all platform and outreach costs when collections do not occur is a vendor confident enough in their recovery performance to put their own revenue at risk. That confidence is either earned through results, as the LAFCU one-million-dollar recovery in 21 days demonstrates, or it collapses quickly. The 1.5 percent model makes the accountability visible and unavoidable in a way that no subscription pricing ever can.

Key Takeaways

Adyen is the wrong tool for collections, not a misconfigured one. Its intelligence stack was trained on authorized payment behavior. It has no model for delinquency signals, no outreach capability, no collections compliance framework, and no pricing tied to recovery outcomes. For high-risk consumer receivables, Adyen's architecture produces silence.

The hardest accounts require consumer empathy, not pressure. Collections teams deploying high-pressure outbound calls on 90-day accounts are optimizing for the approach most likely to produce ghosting. Self-directed, low-friction resolution paths convert delinquent consumers faster, preserve brand trust, and produce recovery rates legacy operations cannot replicate.

Compliance in 2026 is structural, not a checklist. FDCPA, TCPA, CFPB Regulation F, and FCC Revoke All enforcement applied manually at scale is where regulatory exposure originates. Pre-contact structural enforcement with automated audit documentation is the minimum operating requirement, not a premium add-on.

1.5 percent of collections is the only pricing model where the vendor's revenue depends directly on yours improving. If FinanceOps does not recover, it charges nothing and absorbs all costs. That is the clearest alignment of vendor accountability available in the collections market today.

Ready to see what recovery architecture actually delivers for your portfolio?

Book a free FinanceOps Agentic AI demo. No upfront cost. No subscription. 1.5 percent of collections recovered. You pay only when your consumers pay.

FAQs

Why does Adyen fail to recover high-risk consumer receivables?

Adyen was built for payment authorization. It has no outreach capability, no behavioral intelligence for delinquent accounts, no sentiment analysis, no FDCPA or TCPA compliance governance, no Skip-A-Pay mechanism, and no pricing tied to recovery outcomes. When a consumer stops paying, Adyen has nothing to engage them with.

What makes consumer receivables high-risk and why do they need specialized recovery?

High-risk consumer receivables are accounts at 60 days or beyond where standard outreach has already failed to produce payment. ACA International's benchmarking data shows early-stage recovery rates of 85 percent drop below 20 percent by 90 days. These accounts require individual behavioral intelligence, empathetic channel-appropriate outreach, and payment structures calibrated to what each specific consumer can actually sustain.

How is FinanceOps Agentic AI different from Adyen for consumer receivables?

Adyen authorizes payments. FinanceOps recovers delinquent ones. These are different problems built on different architectures. FinanceOps applies account-level behavioral intelligence, real-time sentiment analysis, omnichannel context continuity, affordability-based payment plans, and structural compliance enforcement before first contact. Adyen charges on transaction volume regardless of your receivables outcome. FinanceOps charges 1.5 percent only on successful recovery.

What does 1.5 percent of collections mean versus a traditional collection agency?

Traditional agencies charge 25 to 40 percent of recovered balances. FinanceOps charges 1.5 percent with no upfront cost and zero fee if no collections occur. On a $200,000 recovery, FinanceOps charges $3,000. An agency at 35 percent charges $70,000 on the same recovery. The net recovery difference is $67,000 on a single cycle.

Does Adyen offer any delinquent receivables recovery capability?

No. Adyen is a payment processing platform. It does not offer behavioral intelligence for delinquent accounts, consumer outreach, sentiment-adjusted communication, affordability-based payment restructuring, FDCPA or TCPA compliance governance, or pricing tied to recovery outcomes. These capabilities require a platform built specifically for collections recovery, not payment processing.