Blog

Stripe vs FinanceOps: Why Payment Processors Fail at Collections Recovery

May 25, 2026

Stripe vs FinanceOps Agentic AI: Why Payment Processors Fail at Collections Recovery

Stripe is one of the best payment processors ever built. It is not a collections platform. It was never designed to be one. And every organization that has tried to use it as one has the aging report to prove it.

Here is the precise distinction that makes the entire gap legible: Stripe's Smart Retries, its dunning functionality, and its revenue recovery tooling were built to solve involuntary churn for subscription businesses. Stripe says so directly. Its own engineering blog describes Smart Retries as solving "the problem of involuntary churn for subscription businesses," where 25 percent of lapsed subscriptions result from payment failures the customer never intended. A card expired. A bank flagged a transaction. Insufficient funds on a renewal date. The customer wanted to pay. A technical failure interrupted the transaction. Stripe retries the charge intelligently and recovers the payment. That is what Stripe's dunning does. It retries recoverable technical failures for customers who intended to pay.

That is not what B2C collections recovery does. B2C collections recovery engages customers who have stopped paying, determines why they stopped, re-establishes a payment relationship at the right moment through the right channel with the right tone, and proposes a payment structure the customer can actually sustain. These are not variations of the same problem. They require different data models, different intelligence architectures, different compliance frameworks, and a different pricing structure that ties vendor revenue to recovery outcomes rather than subscription renewal.

This blog is for finance and operations leaders who have watched their B2C delinquency rate climb while their payment processing metrics looked fine. Who have run Stripe dunning sequences and wondered why PTP abandonment kept hitting 40 percent. Who have written off small-balance accounts because the economics of chasing them through a payment gateway never worked.

The gap you are experiencing is not a configuration problem. It is an architecture problem. And it has a specific fix.

Blog Summary

Stripe's dunning and Smart Retries were built to recover failed payments from customers who intended to pay but experienced a technical interruption.

They were not built for B2C collections recovery, where the customer has stopped paying and requires behavioral intelligence, sentiment-adjusted outreach, omnichannel continuity, Skip-A-Pay, affordable payment plans, and structural FDCPA compliance to be recovered.

FinanceOps Agentic AI was built specifically for that problem. It charges 1.5 percent of collections recovered, zero if no collections occur, and no upfront cost or subscription. This blog explains the five structural gaps between what Stripe offers and what B2C collections recovery actually requires.

Table of Contents

What Stripe Was Actually Built to Do

The Five Ways Payment Processors Structurally Fail at B2C Collections Recovery

What B2C Collections Recovery Actually Requires

Skip-A-Pay: The Collections Tool No Payment Processor Offers

Flexible Payment Plans That Customers Can Actually Complete

FinanceOps Agentic AI vs Stripe: Head-to-Head for B2C Collections Recovery

Why 1.5% of Collections Is the Only Pricing Model That Aligns Incentives

Key Takeaways

FAQs

What Stripe Was Actually Built to Do

Being precise about what Stripe was designed to accomplish matters here because the gap with FinanceOps is not about quality. Stripe is exceptional at the problem it was built to solve.

Stripe was built around a single foundational assumption: the customer intends to pay. The system's job is to make the payment mechanics as frictionless as possible. Every machine learning model across each of these platforms was trained on authorized payment behavior: what does a legitimate transaction look like, when do authorization rates peak, and what retry timing reduces involuntary churn on subscription billing.

Stripe's Smart Retries, the most sophisticated element of its revenue recovery suite, uses machine learning trained on billions of transactions to optimize retry timing by card type, decline reason code, and issuer behavior patterns. Stripe's own published data states that Smart Retries recovers an average of 55 percent of failed payments and has recovered $8.2 billion across the platform. Those numbers are real. They reflect Stripe doing exactly what it was built to do for exactly the accounts it was built to handle: subscription customers whose payment method failed for a recoverable technical reason.

Stripe's dunning functionality within Billing sends up to four reminder emails per invoice. The outreach is email-only. Templates are Stripe-branded. The copy does not adapt to the underlying decline reason. No SMS. No voice outreach. No chat. No variation by customer hardship signal or engagement pattern. And critically, Stripe's own documentation describes the entire Smart Retries architecture as designed to solve "involuntary churn for subscription businesses," not delinquent B2C account recovery.

The moment you understand what Stripe was optimized for, every failure mode downstream becomes structurally predictable.

The Five Ways Payment Processors Structurally Fail at B2C Collections Recovery

Structural Failure 1: No behavioral intelligence for delinquent accounts

Stripe's intelligence layer was trained on authorized payment behavior. It knows what a successful transaction looks like. It has no model for what a delinquent account communicates.

It cannot detect that a customer opened the payment link four times this week without completing the transaction. It cannot infer from that behavioral signal that the customer wants to pay but is facing a financial barrier. It cannot distinguish that account from one where the customer has actively decided not to pay and is avoiding contact entirely.

A customer who opened the payment link four times this week is communicating something specific. Stripe's architecture has no mechanism to read that signal or act on it. FinanceOps Agentic AI analyzes exactly these behavioral patterns at the individual account level, before any outreach attempt is made, and calibrates the next action accordingly.

Structural Failure 2: No real-time sentiment adjustment

Stripe's dunning sequence sends the same email on day 3, day 7, and day 14 regardless of what the customer communicated in any prior message. It does not adjust if the customer replies with a hardship explanation. It does not change tone if the customer has engaged repeatedly but not completed a payment. There is no sentiment layer. There is a retry schedule.

A customer experiencing a short-term cash flow disruption who receives firm, escalatory payment demands will not complete the payment. They will disengage. In a B2C context, that disengagement frequently becomes permanent churn. The account does not just become uncollectable. The customer relationship ends.

According to Deloitte's 2024 Financial Services AI Outlook, sentiment-aware AI interactions reduce formal consumer complaints in collections by up to 35 percent and improve payment commitment rates by 22 percent. Stripe has no sentiment layer. It has a retry schedule and four email templates.

Structural Failure 3: No channel continuity across contact switches

A customer who receives a Stripe dunning email, replies explaining their situation, and then calls in to discuss payment options arrives at a payment processor's contact environment as a new interaction. The email reply is in one system. The call is handled separately. The customer re-explains everything. The agent has no context from the prior email exchange.

At the exact moment the customer's payment intent is highest, the platform introduces maximum friction. This is not a workflow problem that better configuration solves. It is an architecture problem. Stripe was not designed to maintain a unified conversation record across channels because that problem does not arise in its intended use case: a subscription customer updating a card number does not need omnichannel context continuity.

A B2C collections recovery platform is designed around exactly that requirement. FinanceOps Agentic AI maintains a single unified conversation record across SMS, email, Voice AI, webchat, and self-service portals. Every channel switch is a continuation of the existing conversation, not a reset.

Structural Failure 4: No FDCPA and TCPA compliance governance at the account level

FDCPA contact frequency limits, TCPA consent requirements, state-specific contact rules, and the FCC Revoke All consent enforcement that took effect in April 2026 all apply at the individual account level across every channel simultaneously. Stripe was built to manage PCI DSS compliance and payment security for authorized transactions. It was not built to enforce FDCPA safe-hour requirements, track consent revocation across all lines of business, or generate audit-ready documentation for every collections interaction at the account level.

For B2C collections operations managing accounts across multiple US states with varying contact consent rules, this compliance gap is not a minor operational inconvenience. It is direct regulatory exposure that scales with every account in the delinquent portfolio.

FinanceOps Agentic AI encodes FDCPA, TCPA, CFPB Regulation F, and state-specific contact rules as structural workflow properties before the system contacts any customer. Not tracked manually after the fact. Enforced before first contact, with timestamped audit documentation at every touchpoint.

Structural Failure 5: No performance-aligned pricing

Stripe Billing charges 0.7 percent of billing volume processed, or a flat fee depending on plan, regardless of whether your delinquency rate improves. The subscription fee is identical whether your aging report gets better or worse. Stripe has no financial stake in your collections performance because collections performance is not what Stripe was built to produce.

This incentive structure creates a platform oriented toward payment processing volume, not recovery outcomes. The roadmap serves the median subscription business managing involuntary churn. It does not serve the B2C collections recovery operation trying to improve an aging report.

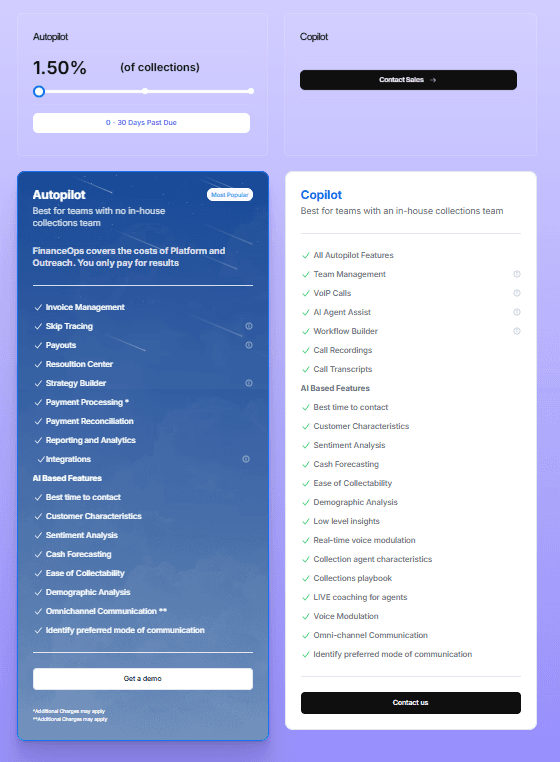

FinanceOps Agentic AI charges 1.5 percent of collections recovered. If no collections occur, the fee is zero. Every dollar of FinanceOps revenue is produced by a dollar of customer account restoration. That alignment is not a marketing claim. It is the structural proof of a collections recovery platform.

What B2C Collections Recovery Actually Requires

B2C collections recovery in 2026 requires six capabilities that Stripe does not provide and that cannot be added through configuration or third-party integration bolted onto a payment processor.

Account-level behavioral intelligence: The system must analyze each specific customer account's payment history, behavioral patterns, device usage, channel responsiveness, and real-time engagement signals before any contact attempt is made. Not portfolio-level ML that optimizes aggregate authorization rates. Account-level intelligence that determines what this specific customer is communicating right now.

Live sentiment analysis: The system must detect tone, hardship cues, engagement likelihood, and compliance risk indicators in real time across every channel and adjust outreach automatically. The customer who replies "I lost my job last month" must receive different follow-up than the customer who has been actively avoiding contact for three weeks.

Omnichannel context continuity: The system must maintain a single unified conversation record across SMS, email, voice, webchat, and self-service portals so that every channel switch is a continuation of the existing conversation, not a reset. According to McKinsey Global Institute research on financial services customer engagement, customers who experience channel continuity are 2.4 times more likely to complete a payment commitment.

Structural compliance governance: FDCPA, TCPA, state-specific contact rules, and the FCC Revoke All consent enforcement must be encoded as structural workflow properties before the system contacts any customer. Not tracked manually. Not checked after the fact. Enforced before first contact with audit-ready documentation at every touchpoint.

Skip-A-Pay and flexible payment plans: The system must offer customers who cannot pay today a structured path to staying current that does not result in a write-off. Payment processors retry the transaction. Collections recovery platforms restructure the payment relationship.

Performance-aligned pricing: The vendor must have a direct financial stake in the recovery outcome. A vendor paid on subscription volume has no institutional reason to optimize for your recovery rate. A vendor paid on successful collections does.

Skip-A-Pay: The Collections Tool No Payment Processor Offers

Skip-A-Pay is the collections capability that most clearly illustrates the gap between what Stripe does and what B2C collections recovery requires. It is also the capability that most directly prevents the outcome every B2C business is trying to avoid: a customer who cannot pay today becomes a customer you never recover.

Here is what Stripe does when a customer cannot make a payment: it retries the original transaction amount on a schedule. Up to four attempts. If retries fail, dunning emails go out. If emails fail, the account ages. The customer receives escalating notifications until the account is written off or sent to a third-party agency. Stripe's architecture has no mechanism to cover the customer's obligation, keep the account current, and collect repayment in installments. It was not designed for that problem.

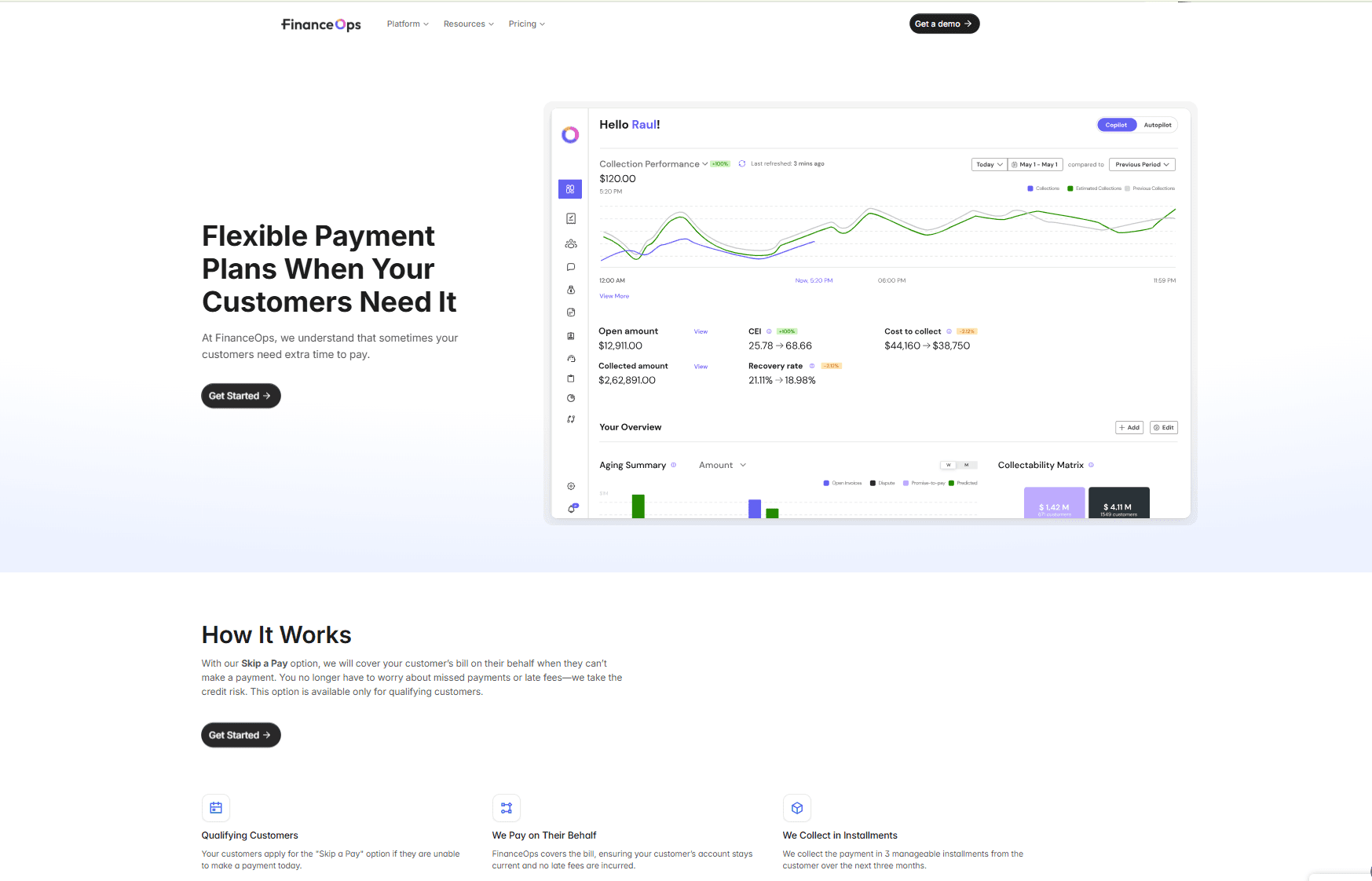

Here is what FinanceOps Agentic AI's Skip-A-Pay does: it covers the customer's bill on their behalf when they cannot make a payment today. The customer's account stays current. No late fees are incurred. No relationship damage occurs. The customer repays FinanceOps in three manageable installments over the following three months. FinanceOps assumes the credit risk.

How Skip-A-Pay works in practice:

The customer applies for the Skip-A-Pay option when they cannot make a payment. FinanceOps evaluates the account for qualification. For qualifying customers, FinanceOps covers the bill immediately, ensuring the account remains current and no late fees are applied. FinanceOps then collects repayment in three installments from the customer over the following three months.

For businesses that require immediate cash flow certainty, FinanceOps also offers a recourse financing option: FinanceOps pays the business the full amount immediately and assumes complete responsibility for collecting repayment from the customer. The business receives the cash. FinanceOps carries the collection risk.

What this means for your delinquency portfolio:

An account that would have aged past 30 days, then 60 days, and eventually been written off stays current. A customer who would have disengaged because the payment system had no path for their situation remains engaged and remains a customer. The relationship is preserved. The account is recovered. And FinanceOps absorbs the credit risk on every qualified account. No payment processor offers this. No dunning sequence produces this outcome.

Flexible Payment Plans That Customers Can Actually Complete

Promise-to-pay abandonment is one of the most expensive and least discussed problems in B2C collections. PTP abandonment rates in traditional collections operations average between 38 and 45 percent. Nearly half of every payment commitment made does not result in a completed payment.

The primary cause is not bad intent. It is bad plan design. A payment plan structured around the balance owed rather than what the customer can actually sustain is a plan that will fail. The commitment made in the conversation is real. The payment structure proposed to produce it is not realistic for that specific customer. The gap between those two things is exactly where abandonment lives.

Stripe retries the original transaction amount. If the customer cannot pay the full amount, the retry fails. No alternative structure is evaluated. No affordability assessment occurs. The account ages.

FinanceOps Agentic AI evaluates each customer's actual repayment capacity before proposing any payment structure. The system draws on payment behavior history, income and expense signals, real-time sentiment indicators from the current interaction, and transaction pattern data. The output is a realistic payment schedule calibrated to what this specific customer can sustain, not a generic installment structure designed for the median account.

Flexible payment schedule options:

Weekly installments for customers managing tight cash flow windows

Bi-weekly installments aligned with paycheck timing

Monthly installments for customers with irregular income

Custom installment structures for accounts with specific financial constraints

The goal is not to get the customer to agree to a payment plan. It is to get the customer to agree to a payment plan they will actually complete. A plan that holds is an account that never ages into the late-stage portfolio. A plan that fails is an account that rolls forward, costs more to resolve, and strains the customer relationship further.

FinanceOps Agentic AI's affordability-first approach reduces PTP abandonment from the 38 to 45 percent industry average to under 20 percent. Every honored plan is a customer relationship that survives the financial hardship intact. Every honored plan is revenue that does not require a write-off or a third-party agency.

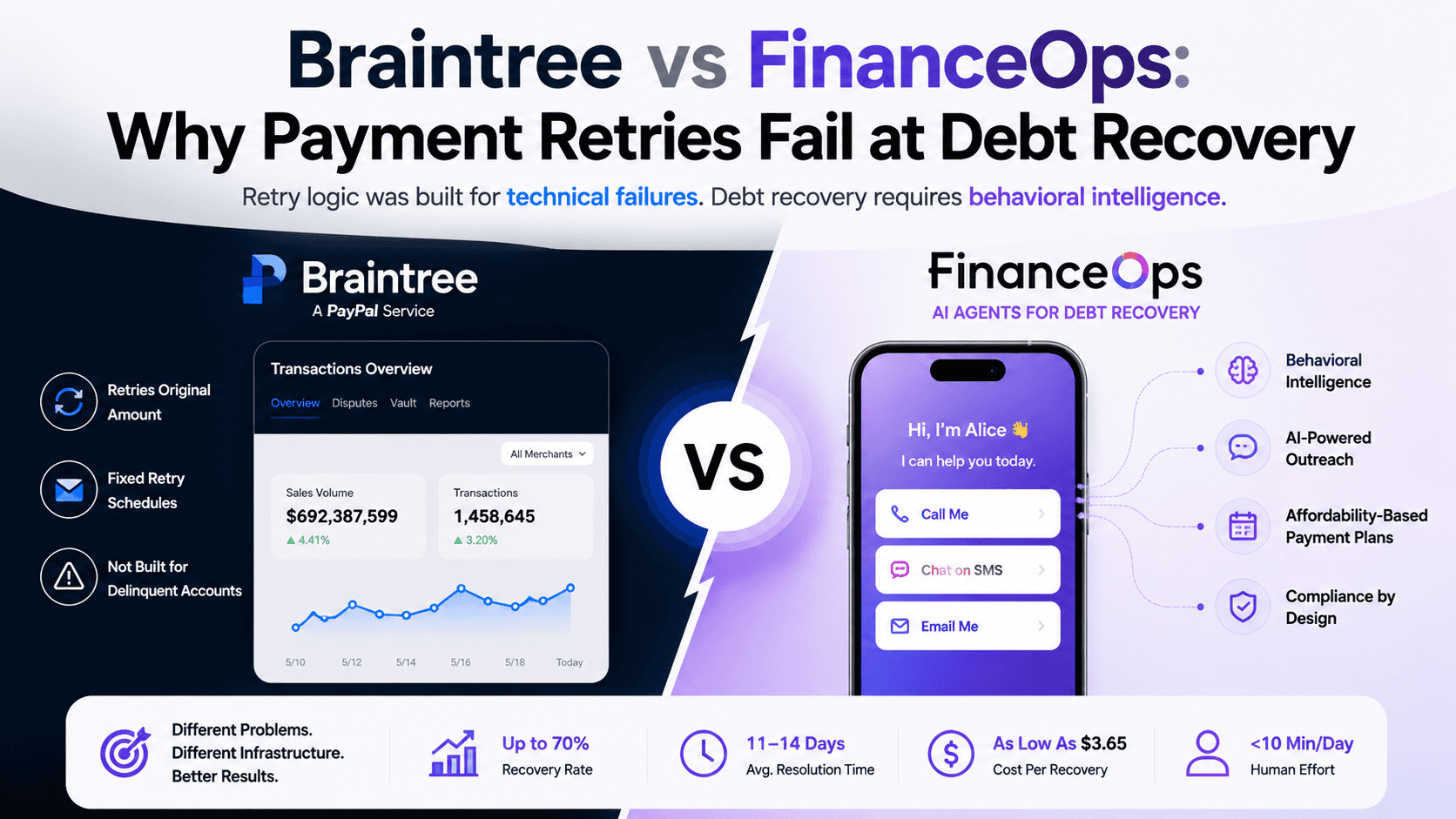

FinanceOps Agentic AI vs Stripe: Head-to-Head for B2C Collections Recovery

Capability | Stripe | FinanceOps Agentic AI |

Primary design purpose | Subscription payment processing, involuntary churn recovery | B2C collections recovery for delinquent accounts |

Dunning / collections | Smart Retries, up to 4 email reminders, email-only | Behavioral intelligence, sentiment analysis, adaptive omnichannel outreach |

Account-level intelligence | None | Full, real-time, per account |

Sentiment analysis | None | Real-time across all channels |

Channel outreach | Email only | SMS, email, Voice AI, webchat, self-service portals |

Channel continuity | None | Full context maintained across every channel switch |

Skip-A-Pay | Not available | Full capability, credit risk assumed by FinanceOps |

Flexible payment plans | Retry original amount only | Affordability-based, calibrated to actual repayment capacity |

PTP abandonment rate | 38 to 45 percent industry average | Under 20 percent |

FDCPA and TCPA compliance | Not applicable, built for PCI DSS | Structural, per account, encoded before first contact |

Multilingual outreach | Not applicable | 150+ languages natively |

Pricing model | 0.7 percent of billing volume processed, subscription-based | 1.5 percent of collections recovered only |

Fee if no collections occur | Charged regardless of recovery outcome | Zero |

Right-party contact rate | Not applicable | 12 to 15 percent versus 2 percent industry norm |

Cost per recovery | Not applicable | As low as $3.65 versus $50 to $150 traditional |

Average resolution time | Not applicable | 11 to 14 days |

Human effort required | Manual AR team management | Under 10 minutes per day |

Audit documentation | Manual | Automated at every touchpoint |

Brand relationship model | None | Tone-calibrated at account level, always respectful |

This is not a feature comparison between two competing products. It is an architecture comparison between two platforms built for structurally different problems. Stripe is the right tool for subscription payment processing and involuntary churn recovery. FinanceOps Agentic AI is the right tool for B2C delinquent account recovery. For organizations trying to use Stripe to solve the second problem, the table above is a description of why the gap in your aging report is not going to close.

Why 1.5% of Collections Is the Only Pricing Model That Aligns Incentives

Most collections technology vendors are paid regardless of whether you recover revenue. The subscription fee is the same whether your delinquency rate improves or worsens. Whether your bad debt write-off line grows or shrinks. Whether your customer relationships are preserved or destroyed in the collections process.

Stripe Billing charges 0.7 percent of billing volume processed. That fee is identical whether the dunning sequence recovers 10 percent of your delinquent accounts or 60 percent. Stripe's institutional revenue is not affected by your collections performance. Its roadmap and development priorities reflect that reality.

FinanceOps Agentic AI charges 1.5 percent of collections recovered. There is no upfront cost. There is no subscription fee. There is no credit card required to start. If no collections occur, the fee is zero and FinanceOps absorbs all platform and outreach costs.

What 1.5 percent means in practice:

If FinanceOps Agentic AI recovers $500,000 from your delinquent B2C portfolio, the fee is $7,500 and the net recovery is $492,500. Compare that to traditional third-party collection agencies, which charge between 25 and 40 percent of recovered amounts. On the same $500,000 recovery, a traditional agency charges between $125,000 and $200,000. FinanceOps charges $7,500. The difference is not incremental. It is structural.

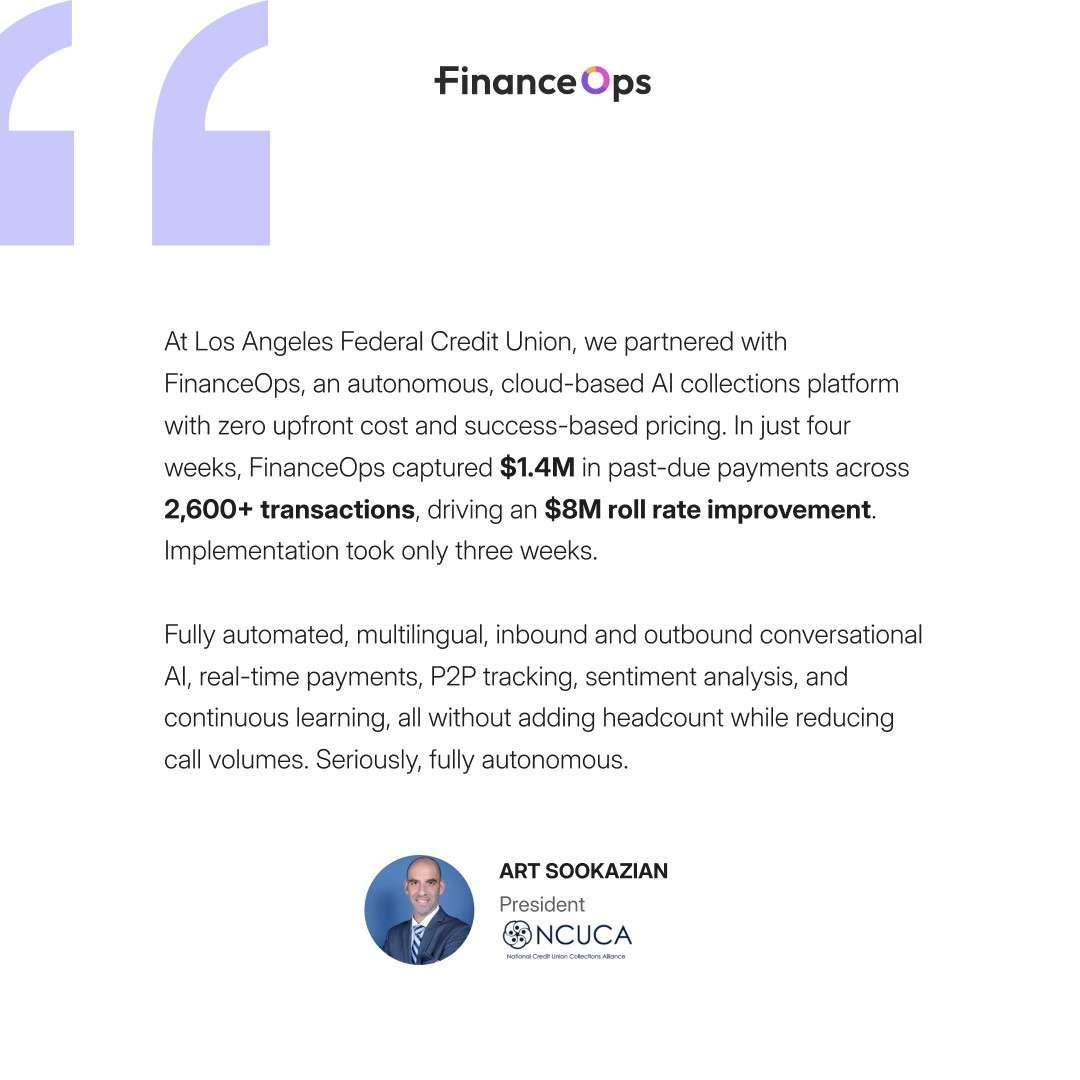

NCUCA Testimonial for FinanceOps Agentic AI

What the pricing model signals about vendor accountability:

A vendor that charges 1.5 percent of what it recovers has every institutional reason to recover as much as possible, as quickly as possible, in a way that preserves the customer relationship so that future recovery cycles remain viable. A vendor paid on subscription volume or processing fees has no such incentive. The misalignment is not incidental. It produces different development priorities, different support structures, and categorically different levels of accountability for your specific collections outcome.

The 1.5 percent model is not a pricing strategy. It is the structural proof that FinanceOps Agentic AI's revenue depends entirely on yours improving.

Key Takeaways

Stripe's dunning was built for involuntary churn, not delinquent account recovery. Stripe says this explicitly in its own documentation. Smart Retries solves the problem of subscription customers whose payment failed for a recoverable technical reason. It retries the charge intelligently and recovers payments from customers who intended to pay. That is a genuinely valuable capability for the problem it was built for. It is the wrong architecture for B2C collections recovery, where the customer has stopped paying and requires behavioral intelligence, sentiment-adjusted outreach, and structural flexibility to be recovered.

Skip-A-Pay and affordability-based payment plans are the capabilities that determine whether a customer stays or churns permanently. A customer who cannot pay today is not a write-off. They are an account that needs a different path than a retry schedule provides. FinanceOps covers the bill, assumes the credit risk, and collects in three installments. That is the difference between a permanently lost customer and a recovered one. No payment processor architecture produces that outcome.

1.5 percent of collections is the only pricing model in the market where the vendor's revenue depends directly on your recovering. Stripe charges on billing volume regardless of collections performance. FinanceOps charges nothing if nothing is recovered and 1.5 percent of what is actually collected when recovery occurs. Start free, no credit card required, and pay only when your customers pay.

Ready to see what Recovery Architecture delivers in your B2C portfolio?

Book a free 20-minute demo with FinanceOps Agentic AI. Your delinquent accounts, your aging bucket, your customer relationship model, mapped against what behavioral intelligence, Skip-A-Pay, flexible payment plans, and FDCPA-compliant autonomous outreach actually produce in your specific portfolio.

No upfront cost. No subscription. 1.5 percent of collections recovered. You pay only when your customers pay.

FAQs

Why does Stripe's dunning fail to recover delinquent B2C accounts?

Stripe's dunning and Smart Retries were designed to recover failed payments from subscription customers who intended to pay but experienced a technical payment interruption. Stripe retries the original charge amount on an optimized schedule and sends up to four email reminders. It does not analyze why a customer stopped paying, adjust outreach tone based on hardship signals, offer alternative payment structures like Skip-A-Pay, or enforce FDCPA compliance at the account level. For genuinely delinquent B2C accounts, where the customer has stopped paying and needs a different kind of engagement entirely, Stripe's architecture produces retries, generic email reminders, and eventually aged balances. FinanceOps Agentic AI was built specifically for delinquent account recovery using behavioral intelligence, sentiment-adaptive outreach, and affordability-based payment plans.

What is Skip-A-Pay and how does it help B2C collections recovery?

Skip-A-Pay is a FinanceOps Agentic AI capability that covers a customer's bill on their behalf when they cannot make a payment today, keeping the account current and avoiding late fees or relationship damage. FinanceOps then collects repayment in three manageable installments while assuming the credit risk. Businesses can also select a recourse financing option where FinanceOps pays the business immediately and handles repayment collection directly. Stripe has no equivalent capability. Its architecture retries the original amount and escalates through email notifications if retries fail.

How is FinanceOps Agentic AI different from Stripe for B2C collections?

Stripe is built to move authorized payments and optimize payment success rates for subscription businesses. FinanceOps Agentic AI is built to recover delinquent payments using account-level behavioral intelligence, real-time sentiment analysis, omnichannel context continuity across SMS, email, Voice AI, webchat, and self-service portals, affordability-based payment plans, and structural FDCPA and TCPA compliance enforcement before first contact. Stripe charges 0.7 percent of billing volume regardless of collections outcome. FinanceOps charges 1.5 percent only on successfully recovered payments.

What does 1.5% of collections mean compared to a traditional collection agency?

Traditional collection agencies typically charge 25 to 40 percent of recovered balances. FinanceOps Agentic AI charges 1.5 percent of collections recovered with no upfront cost, no subscription fee, and no fee if no collections occur. On a $150,000 recovery, FinanceOps charges $2,250. A traditional agency charging 30 percent charges $45,000 on the same recovery. The pricing model also aligns FinanceOps directly to recovery performance because its revenue is generated only when collections occur.

Can FinanceOps Agentic AI handle B2C collections across the US and Canada without damaging customer relationships?

Yes. FinanceOps Agentic AI recovers delinquent B2C payments while preserving customer relationships through live sentiment analysis that adjusts outreach tone based on detected hardship and engagement signals, Skip-A-Pay for customers who cannot pay today, and affordability-based payment plans calibrated to actual repayment capacity. The platform enforces FDCPA, TCPA, CFPB Regulation F, and applicable Canadian compliance rules as structural workflow properties before any outreach begins. All communication is multilingual, brand-compliant, and produces timestamped audit documentation at every touchpoint.

Does Stripe offer any B2C debt collections or delinquent account recovery capability?

No. Stripe's revenue recovery suite, including Smart Retries and Billing dunning, was explicitly built to address involuntary churn for subscription businesses: situations where a payment failed due to a recoverable technical reason and the customer intended to pay. Stripe does not offer behavioral intelligence for delinquent accounts, sentiment-adjusted outreach, Skip-A-Pay, affordability-based payment restructuring, FDCPA compliance governance, or any pricing model tied to delinquent account recovery outcomes. These capabilities require a platform built specifically for collections recovery, not payment processing.

Stripe vs FinanceOps Agentic AI: Why Payment Processors Fail at Collections Recovery

Stripe is one of the best payment processors ever built. It is not a collections platform. It was never designed to be one. And every organization that has tried to use it as one has the aging report to prove it.

Here is the precise distinction that makes the entire gap legible: Stripe's Smart Retries, its dunning functionality, and its revenue recovery tooling were built to solve involuntary churn for subscription businesses. Stripe says so directly. Its own engineering blog describes Smart Retries as solving "the problem of involuntary churn for subscription businesses," where 25 percent of lapsed subscriptions result from payment failures the customer never intended. A card expired. A bank flagged a transaction. Insufficient funds on a renewal date. The customer wanted to pay. A technical failure interrupted the transaction. Stripe retries the charge intelligently and recovers the payment. That is what Stripe's dunning does. It retries recoverable technical failures for customers who intended to pay.

That is not what B2C collections recovery does. B2C collections recovery engages customers who have stopped paying, determines why they stopped, re-establishes a payment relationship at the right moment through the right channel with the right tone, and proposes a payment structure the customer can actually sustain. These are not variations of the same problem. They require different data models, different intelligence architectures, different compliance frameworks, and a different pricing structure that ties vendor revenue to recovery outcomes rather than subscription renewal.

This blog is for finance and operations leaders who have watched their B2C delinquency rate climb while their payment processing metrics looked fine. Who have run Stripe dunning sequences and wondered why PTP abandonment kept hitting 40 percent. Who have written off small-balance accounts because the economics of chasing them through a payment gateway never worked.

The gap you are experiencing is not a configuration problem. It is an architecture problem. And it has a specific fix.

Blog Summary

Stripe's dunning and Smart Retries were built to recover failed payments from customers who intended to pay but experienced a technical interruption.

They were not built for B2C collections recovery, where the customer has stopped paying and requires behavioral intelligence, sentiment-adjusted outreach, omnichannel continuity, Skip-A-Pay, affordable payment plans, and structural FDCPA compliance to be recovered.

FinanceOps Agentic AI was built specifically for that problem. It charges 1.5 percent of collections recovered, zero if no collections occur, and no upfront cost or subscription. This blog explains the five structural gaps between what Stripe offers and what B2C collections recovery actually requires.

Table of Contents

What Stripe Was Actually Built to Do

The Five Ways Payment Processors Structurally Fail at B2C Collections Recovery

What B2C Collections Recovery Actually Requires

Skip-A-Pay: The Collections Tool No Payment Processor Offers

Flexible Payment Plans That Customers Can Actually Complete

FinanceOps Agentic AI vs Stripe: Head-to-Head for B2C Collections Recovery

Why 1.5% of Collections Is the Only Pricing Model That Aligns Incentives

Key Takeaways

FAQs

What Stripe Was Actually Built to Do

Being precise about what Stripe was designed to accomplish matters here because the gap with FinanceOps is not about quality. Stripe is exceptional at the problem it was built to solve.

Stripe was built around a single foundational assumption: the customer intends to pay. The system's job is to make the payment mechanics as frictionless as possible. Every machine learning model across each of these platforms was trained on authorized payment behavior: what does a legitimate transaction look like, when do authorization rates peak, and what retry timing reduces involuntary churn on subscription billing.

Stripe's Smart Retries, the most sophisticated element of its revenue recovery suite, uses machine learning trained on billions of transactions to optimize retry timing by card type, decline reason code, and issuer behavior patterns. Stripe's own published data states that Smart Retries recovers an average of 55 percent of failed payments and has recovered $8.2 billion across the platform. Those numbers are real. They reflect Stripe doing exactly what it was built to do for exactly the accounts it was built to handle: subscription customers whose payment method failed for a recoverable technical reason.

Stripe's dunning functionality within Billing sends up to four reminder emails per invoice. The outreach is email-only. Templates are Stripe-branded. The copy does not adapt to the underlying decline reason. No SMS. No voice outreach. No chat. No variation by customer hardship signal or engagement pattern. And critically, Stripe's own documentation describes the entire Smart Retries architecture as designed to solve "involuntary churn for subscription businesses," not delinquent B2C account recovery.

The moment you understand what Stripe was optimized for, every failure mode downstream becomes structurally predictable.

The Five Ways Payment Processors Structurally Fail at B2C Collections Recovery

Structural Failure 1: No behavioral intelligence for delinquent accounts

Stripe's intelligence layer was trained on authorized payment behavior. It knows what a successful transaction looks like. It has no model for what a delinquent account communicates.

It cannot detect that a customer opened the payment link four times this week without completing the transaction. It cannot infer from that behavioral signal that the customer wants to pay but is facing a financial barrier. It cannot distinguish that account from one where the customer has actively decided not to pay and is avoiding contact entirely.

A customer who opened the payment link four times this week is communicating something specific. Stripe's architecture has no mechanism to read that signal or act on it. FinanceOps Agentic AI analyzes exactly these behavioral patterns at the individual account level, before any outreach attempt is made, and calibrates the next action accordingly.

Structural Failure 2: No real-time sentiment adjustment

Stripe's dunning sequence sends the same email on day 3, day 7, and day 14 regardless of what the customer communicated in any prior message. It does not adjust if the customer replies with a hardship explanation. It does not change tone if the customer has engaged repeatedly but not completed a payment. There is no sentiment layer. There is a retry schedule.

A customer experiencing a short-term cash flow disruption who receives firm, escalatory payment demands will not complete the payment. They will disengage. In a B2C context, that disengagement frequently becomes permanent churn. The account does not just become uncollectable. The customer relationship ends.

According to Deloitte's 2024 Financial Services AI Outlook, sentiment-aware AI interactions reduce formal consumer complaints in collections by up to 35 percent and improve payment commitment rates by 22 percent. Stripe has no sentiment layer. It has a retry schedule and four email templates.

Structural Failure 3: No channel continuity across contact switches

A customer who receives a Stripe dunning email, replies explaining their situation, and then calls in to discuss payment options arrives at a payment processor's contact environment as a new interaction. The email reply is in one system. The call is handled separately. The customer re-explains everything. The agent has no context from the prior email exchange.

At the exact moment the customer's payment intent is highest, the platform introduces maximum friction. This is not a workflow problem that better configuration solves. It is an architecture problem. Stripe was not designed to maintain a unified conversation record across channels because that problem does not arise in its intended use case: a subscription customer updating a card number does not need omnichannel context continuity.

A B2C collections recovery platform is designed around exactly that requirement. FinanceOps Agentic AI maintains a single unified conversation record across SMS, email, Voice AI, webchat, and self-service portals. Every channel switch is a continuation of the existing conversation, not a reset.

Structural Failure 4: No FDCPA and TCPA compliance governance at the account level

FDCPA contact frequency limits, TCPA consent requirements, state-specific contact rules, and the FCC Revoke All consent enforcement that took effect in April 2026 all apply at the individual account level across every channel simultaneously. Stripe was built to manage PCI DSS compliance and payment security for authorized transactions. It was not built to enforce FDCPA safe-hour requirements, track consent revocation across all lines of business, or generate audit-ready documentation for every collections interaction at the account level.

For B2C collections operations managing accounts across multiple US states with varying contact consent rules, this compliance gap is not a minor operational inconvenience. It is direct regulatory exposure that scales with every account in the delinquent portfolio.

FinanceOps Agentic AI encodes FDCPA, TCPA, CFPB Regulation F, and state-specific contact rules as structural workflow properties before the system contacts any customer. Not tracked manually after the fact. Enforced before first contact, with timestamped audit documentation at every touchpoint.

Structural Failure 5: No performance-aligned pricing

Stripe Billing charges 0.7 percent of billing volume processed, or a flat fee depending on plan, regardless of whether your delinquency rate improves. The subscription fee is identical whether your aging report gets better or worse. Stripe has no financial stake in your collections performance because collections performance is not what Stripe was built to produce.

This incentive structure creates a platform oriented toward payment processing volume, not recovery outcomes. The roadmap serves the median subscription business managing involuntary churn. It does not serve the B2C collections recovery operation trying to improve an aging report.

FinanceOps Agentic AI charges 1.5 percent of collections recovered. If no collections occur, the fee is zero. Every dollar of FinanceOps revenue is produced by a dollar of customer account restoration. That alignment is not a marketing claim. It is the structural proof of a collections recovery platform.

What B2C Collections Recovery Actually Requires

B2C collections recovery in 2026 requires six capabilities that Stripe does not provide and that cannot be added through configuration or third-party integration bolted onto a payment processor.

Account-level behavioral intelligence: The system must analyze each specific customer account's payment history, behavioral patterns, device usage, channel responsiveness, and real-time engagement signals before any contact attempt is made. Not portfolio-level ML that optimizes aggregate authorization rates. Account-level intelligence that determines what this specific customer is communicating right now.

Live sentiment analysis: The system must detect tone, hardship cues, engagement likelihood, and compliance risk indicators in real time across every channel and adjust outreach automatically. The customer who replies "I lost my job last month" must receive different follow-up than the customer who has been actively avoiding contact for three weeks.

Omnichannel context continuity: The system must maintain a single unified conversation record across SMS, email, voice, webchat, and self-service portals so that every channel switch is a continuation of the existing conversation, not a reset. According to McKinsey Global Institute research on financial services customer engagement, customers who experience channel continuity are 2.4 times more likely to complete a payment commitment.

Structural compliance governance: FDCPA, TCPA, state-specific contact rules, and the FCC Revoke All consent enforcement must be encoded as structural workflow properties before the system contacts any customer. Not tracked manually. Not checked after the fact. Enforced before first contact with audit-ready documentation at every touchpoint.

Skip-A-Pay and flexible payment plans: The system must offer customers who cannot pay today a structured path to staying current that does not result in a write-off. Payment processors retry the transaction. Collections recovery platforms restructure the payment relationship.

Performance-aligned pricing: The vendor must have a direct financial stake in the recovery outcome. A vendor paid on subscription volume has no institutional reason to optimize for your recovery rate. A vendor paid on successful collections does.

Skip-A-Pay: The Collections Tool No Payment Processor Offers

Skip-A-Pay is the collections capability that most clearly illustrates the gap between what Stripe does and what B2C collections recovery requires. It is also the capability that most directly prevents the outcome every B2C business is trying to avoid: a customer who cannot pay today becomes a customer you never recover.

Here is what Stripe does when a customer cannot make a payment: it retries the original transaction amount on a schedule. Up to four attempts. If retries fail, dunning emails go out. If emails fail, the account ages. The customer receives escalating notifications until the account is written off or sent to a third-party agency. Stripe's architecture has no mechanism to cover the customer's obligation, keep the account current, and collect repayment in installments. It was not designed for that problem.

Here is what FinanceOps Agentic AI's Skip-A-Pay does: it covers the customer's bill on their behalf when they cannot make a payment today. The customer's account stays current. No late fees are incurred. No relationship damage occurs. The customer repays FinanceOps in three manageable installments over the following three months. FinanceOps assumes the credit risk.

How Skip-A-Pay works in practice:

The customer applies for the Skip-A-Pay option when they cannot make a payment. FinanceOps evaluates the account for qualification. For qualifying customers, FinanceOps covers the bill immediately, ensuring the account remains current and no late fees are applied. FinanceOps then collects repayment in three installments from the customer over the following three months.

For businesses that require immediate cash flow certainty, FinanceOps also offers a recourse financing option: FinanceOps pays the business the full amount immediately and assumes complete responsibility for collecting repayment from the customer. The business receives the cash. FinanceOps carries the collection risk.

What this means for your delinquency portfolio:

An account that would have aged past 30 days, then 60 days, and eventually been written off stays current. A customer who would have disengaged because the payment system had no path for their situation remains engaged and remains a customer. The relationship is preserved. The account is recovered. And FinanceOps absorbs the credit risk on every qualified account. No payment processor offers this. No dunning sequence produces this outcome.

Flexible Payment Plans That Customers Can Actually Complete

Promise-to-pay abandonment is one of the most expensive and least discussed problems in B2C collections. PTP abandonment rates in traditional collections operations average between 38 and 45 percent. Nearly half of every payment commitment made does not result in a completed payment.

The primary cause is not bad intent. It is bad plan design. A payment plan structured around the balance owed rather than what the customer can actually sustain is a plan that will fail. The commitment made in the conversation is real. The payment structure proposed to produce it is not realistic for that specific customer. The gap between those two things is exactly where abandonment lives.

Stripe retries the original transaction amount. If the customer cannot pay the full amount, the retry fails. No alternative structure is evaluated. No affordability assessment occurs. The account ages.

FinanceOps Agentic AI evaluates each customer's actual repayment capacity before proposing any payment structure. The system draws on payment behavior history, income and expense signals, real-time sentiment indicators from the current interaction, and transaction pattern data. The output is a realistic payment schedule calibrated to what this specific customer can sustain, not a generic installment structure designed for the median account.

Flexible payment schedule options:

Weekly installments for customers managing tight cash flow windows

Bi-weekly installments aligned with paycheck timing

Monthly installments for customers with irregular income

Custom installment structures for accounts with specific financial constraints

The goal is not to get the customer to agree to a payment plan. It is to get the customer to agree to a payment plan they will actually complete. A plan that holds is an account that never ages into the late-stage portfolio. A plan that fails is an account that rolls forward, costs more to resolve, and strains the customer relationship further.

FinanceOps Agentic AI's affordability-first approach reduces PTP abandonment from the 38 to 45 percent industry average to under 20 percent. Every honored plan is a customer relationship that survives the financial hardship intact. Every honored plan is revenue that does not require a write-off or a third-party agency.

FinanceOps Agentic AI vs Stripe: Head-to-Head for B2C Collections Recovery

Capability | Stripe | FinanceOps Agentic AI |

Primary design purpose | Subscription payment processing, involuntary churn recovery | B2C collections recovery for delinquent accounts |

Dunning / collections | Smart Retries, up to 4 email reminders, email-only | Behavioral intelligence, sentiment analysis, adaptive omnichannel outreach |

Account-level intelligence | None | Full, real-time, per account |

Sentiment analysis | None | Real-time across all channels |

Channel outreach | Email only | SMS, email, Voice AI, webchat, self-service portals |

Channel continuity | None | Full context maintained across every channel switch |

Skip-A-Pay | Not available | Full capability, credit risk assumed by FinanceOps |

Flexible payment plans | Retry original amount only | Affordability-based, calibrated to actual repayment capacity |

PTP abandonment rate | 38 to 45 percent industry average | Under 20 percent |

FDCPA and TCPA compliance | Not applicable, built for PCI DSS | Structural, per account, encoded before first contact |

Multilingual outreach | Not applicable | 150+ languages natively |

Pricing model | 0.7 percent of billing volume processed, subscription-based | 1.5 percent of collections recovered only |

Fee if no collections occur | Charged regardless of recovery outcome | Zero |

Right-party contact rate | Not applicable | 12 to 15 percent versus 2 percent industry norm |

Cost per recovery | Not applicable | As low as $3.65 versus $50 to $150 traditional |

Average resolution time | Not applicable | 11 to 14 days |

Human effort required | Manual AR team management | Under 10 minutes per day |

Audit documentation | Manual | Automated at every touchpoint |

Brand relationship model | None | Tone-calibrated at account level, always respectful |

This is not a feature comparison between two competing products. It is an architecture comparison between two platforms built for structurally different problems. Stripe is the right tool for subscription payment processing and involuntary churn recovery. FinanceOps Agentic AI is the right tool for B2C delinquent account recovery. For organizations trying to use Stripe to solve the second problem, the table above is a description of why the gap in your aging report is not going to close.

Why 1.5% of Collections Is the Only Pricing Model That Aligns Incentives

Most collections technology vendors are paid regardless of whether you recover revenue. The subscription fee is the same whether your delinquency rate improves or worsens. Whether your bad debt write-off line grows or shrinks. Whether your customer relationships are preserved or destroyed in the collections process.

Stripe Billing charges 0.7 percent of billing volume processed. That fee is identical whether the dunning sequence recovers 10 percent of your delinquent accounts or 60 percent. Stripe's institutional revenue is not affected by your collections performance. Its roadmap and development priorities reflect that reality.

FinanceOps Agentic AI charges 1.5 percent of collections recovered. There is no upfront cost. There is no subscription fee. There is no credit card required to start. If no collections occur, the fee is zero and FinanceOps absorbs all platform and outreach costs.

What 1.5 percent means in practice:

If FinanceOps Agentic AI recovers $500,000 from your delinquent B2C portfolio, the fee is $7,500 and the net recovery is $492,500. Compare that to traditional third-party collection agencies, which charge between 25 and 40 percent of recovered amounts. On the same $500,000 recovery, a traditional agency charges between $125,000 and $200,000. FinanceOps charges $7,500. The difference is not incremental. It is structural.

NCUCA Testimonial for FinanceOps Agentic AI

What the pricing model signals about vendor accountability:

A vendor that charges 1.5 percent of what it recovers has every institutional reason to recover as much as possible, as quickly as possible, in a way that preserves the customer relationship so that future recovery cycles remain viable. A vendor paid on subscription volume or processing fees has no such incentive. The misalignment is not incidental. It produces different development priorities, different support structures, and categorically different levels of accountability for your specific collections outcome.

The 1.5 percent model is not a pricing strategy. It is the structural proof that FinanceOps Agentic AI's revenue depends entirely on yours improving.

Key Takeaways

Stripe's dunning was built for involuntary churn, not delinquent account recovery. Stripe says this explicitly in its own documentation. Smart Retries solves the problem of subscription customers whose payment failed for a recoverable technical reason. It retries the charge intelligently and recovers payments from customers who intended to pay. That is a genuinely valuable capability for the problem it was built for. It is the wrong architecture for B2C collections recovery, where the customer has stopped paying and requires behavioral intelligence, sentiment-adjusted outreach, and structural flexibility to be recovered.

Skip-A-Pay and affordability-based payment plans are the capabilities that determine whether a customer stays or churns permanently. A customer who cannot pay today is not a write-off. They are an account that needs a different path than a retry schedule provides. FinanceOps covers the bill, assumes the credit risk, and collects in three installments. That is the difference between a permanently lost customer and a recovered one. No payment processor architecture produces that outcome.

1.5 percent of collections is the only pricing model in the market where the vendor's revenue depends directly on your recovering. Stripe charges on billing volume regardless of collections performance. FinanceOps charges nothing if nothing is recovered and 1.5 percent of what is actually collected when recovery occurs. Start free, no credit card required, and pay only when your customers pay.

Ready to see what Recovery Architecture delivers in your B2C portfolio?

Book a free 20-minute demo with FinanceOps Agentic AI. Your delinquent accounts, your aging bucket, your customer relationship model, mapped against what behavioral intelligence, Skip-A-Pay, flexible payment plans, and FDCPA-compliant autonomous outreach actually produce in your specific portfolio.

No upfront cost. No subscription. 1.5 percent of collections recovered. You pay only when your customers pay.

FAQs

Why does Stripe's dunning fail to recover delinquent B2C accounts?

Stripe's dunning and Smart Retries were designed to recover failed payments from subscription customers who intended to pay but experienced a technical payment interruption. Stripe retries the original charge amount on an optimized schedule and sends up to four email reminders. It does not analyze why a customer stopped paying, adjust outreach tone based on hardship signals, offer alternative payment structures like Skip-A-Pay, or enforce FDCPA compliance at the account level. For genuinely delinquent B2C accounts, where the customer has stopped paying and needs a different kind of engagement entirely, Stripe's architecture produces retries, generic email reminders, and eventually aged balances. FinanceOps Agentic AI was built specifically for delinquent account recovery using behavioral intelligence, sentiment-adaptive outreach, and affordability-based payment plans.

What is Skip-A-Pay and how does it help B2C collections recovery?

Skip-A-Pay is a FinanceOps Agentic AI capability that covers a customer's bill on their behalf when they cannot make a payment today, keeping the account current and avoiding late fees or relationship damage. FinanceOps then collects repayment in three manageable installments while assuming the credit risk. Businesses can also select a recourse financing option where FinanceOps pays the business immediately and handles repayment collection directly. Stripe has no equivalent capability. Its architecture retries the original amount and escalates through email notifications if retries fail.

How is FinanceOps Agentic AI different from Stripe for B2C collections?

Stripe is built to move authorized payments and optimize payment success rates for subscription businesses. FinanceOps Agentic AI is built to recover delinquent payments using account-level behavioral intelligence, real-time sentiment analysis, omnichannel context continuity across SMS, email, Voice AI, webchat, and self-service portals, affordability-based payment plans, and structural FDCPA and TCPA compliance enforcement before first contact. Stripe charges 0.7 percent of billing volume regardless of collections outcome. FinanceOps charges 1.5 percent only on successfully recovered payments.

What does 1.5% of collections mean compared to a traditional collection agency?

Traditional collection agencies typically charge 25 to 40 percent of recovered balances. FinanceOps Agentic AI charges 1.5 percent of collections recovered with no upfront cost, no subscription fee, and no fee if no collections occur. On a $150,000 recovery, FinanceOps charges $2,250. A traditional agency charging 30 percent charges $45,000 on the same recovery. The pricing model also aligns FinanceOps directly to recovery performance because its revenue is generated only when collections occur.

Can FinanceOps Agentic AI handle B2C collections across the US and Canada without damaging customer relationships?

Yes. FinanceOps Agentic AI recovers delinquent B2C payments while preserving customer relationships through live sentiment analysis that adjusts outreach tone based on detected hardship and engagement signals, Skip-A-Pay for customers who cannot pay today, and affordability-based payment plans calibrated to actual repayment capacity. The platform enforces FDCPA, TCPA, CFPB Regulation F, and applicable Canadian compliance rules as structural workflow properties before any outreach begins. All communication is multilingual, brand-compliant, and produces timestamped audit documentation at every touchpoint.

Does Stripe offer any B2C debt collections or delinquent account recovery capability?

No. Stripe's revenue recovery suite, including Smart Retries and Billing dunning, was explicitly built to address involuntary churn for subscription businesses: situations where a payment failed due to a recoverable technical reason and the customer intended to pay. Stripe does not offer behavioral intelligence for delinquent accounts, sentiment-adjusted outreach, Skip-A-Pay, affordability-based payment restructuring, FDCPA compliance governance, or any pricing model tied to delinquent account recovery outcomes. These capabilities require a platform built specifically for collections recovery, not payment processing.

6 minutes

Posted by

Arpita Mahato

Content Writer

Other Blogs

View other blogs

Stay Updated with Us

Enter your email below and subscribe to our weekly newsletter

Instant Access

Boost Productivity

Easy Setup

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps