Blog

Why One Layer of Automation Is Not Enough in Debt Recovery

Mar 4, 2026

Blog Summary: This blog explains why relying on single-layer automation (email reminders, dialers, and workflow triggers) falls short in debt recovery. Rising delinquencies, cash-flow pressure, and shifting borrower behavior in 2026 make traditional automation ineffective. We’ll show how SMBs lose collectible receivables and why automation alone isn’t enough. Learn how unified payments platforms and AI-driven solutions can deliver predictable, high-ROI recovery for SMBs.

Table of Contents:

Why One Layer of Automation Is Not Enough

The Debt Recovery Reality for Small Businesses in 2026

The Single-Layer Automation Trap (Why It Fails)

The Five Layers SMBs Actually Need for High-ROI Debt Recovery

Why SMBs Need Agentic AI, Not Just Automation

What Agentic AI Enables

Must-Haves vs. Red Flags When Evaluating AI Debt Recovery Solutions

What a Unified Payments + Agentic AI System Looks Like

One-Layer Automation vs Agentic AI Automation

Key Takeaway

FAQs

Why One Layer of Automation Is Not Enough

For most SMBs, the challenge isn’t that customers refuse to pay. It’s that their recovery systems can’t keep up with the demands of 2026. In the face of rising delinquencies, volatile repayment behavior, and shrinking cash buffers, traditional one-layer automation (like email reminders or dialers) simply isn’t enough. These systems execute tasks but don’t make decisions. They lack the intelligence needed to prioritize high-risk accounts or engage customers based on their individual repayment behavior.

By relying on single-layer systems, SMBs are allowing 60% of collectible receivables to slip through the cracks, leading to stretched cash cycles, tight liquidity, and expensive short-term financing. What SMBs need is more than just automation, they need intelligent, unified execution powered by Agentic AI. The future of debt recovery isn’t about more reminders; it’s about intelligent decision-making that drives recovery at scale.

The Debt Recovery Reality for Small Businesses in 2026

Small businesses are facing a tough landscape in 2026. Inflation, tighter credit conditions, and rising operational costs have made SMBs more vulnerable to delinquency risks.

Delinquencies are rising: Credit data from TransUnion and Experian show increased repayment stress, with customers rolling from 30-day to 60- and 90-day delinquency buckets.

Excess payment capacity is shrinking: The aggregated Excess Payment (AEP) indicator, which tracks a borrower’s ability to pay above the minimum, continues to decline, leaving less cushion for early-stage corrective actions.

Cash buffers are dangerously thin: The JPMorgan Chase Institute reports that most SMBs operate with less than 27 days of cash on hand, making even modest payment delays highly disruptive.

Manual collections processes and basic automation just can’t keep pace with these challenges. Without intelligent systems that understand borrower behavior, SMBs miss out on critical recovery windows.

The Single-Layer Automation Trap (Why It Fails)

Traditional debt recovery automation often revolves around sending automated reminders: a generic email, an SMS follow-up, and maybe a call after a few days. While this generates activity, it doesn’t produce meaningful results.

The problem is that reminder-only automation is task-focused, not decision-focused. It fails to interpret risk, understand borrower behavior, or guide accounts toward repayment. Effective debt recovery requires systems that can analyze signals and adjust strategies in real time, adapting to borrower intent and engagement.

Where Single-Layer Automation Breaks

No Segmentation: Treating all overdue accounts the same ignores risk levels and borrower behavior.

No Risk-Based Prioritization: Without predictive risk scoring, teams can’t focus on high-impact accounts.

No Predictive Outreach: Fixed schedules aren’t aligned with borrower behavior, reducing engagement.

No Payments Intelligence: Limited payment options create friction, reducing payment completion.

No Escalation Logic: Same messages are sent repeatedly, regardless of engagement signals.

No Affordability Modeling: Lacking flexible payment options, SMBs fail to convert constrained borrowers.

No Context Continuity: Multiple channels lack context, leading to repetitive, inefficient outreach.

Single-layer automation sends reminders but does not manage the repayment journey. Effective debt recovery requires coordination between risk signals, communication strategy, payment infrastructure, and affordability intelligence.

The Five Layers SMBs Actually Need for High-ROI Debt Recovery

Single-layer automation won’t suffice. SMBs need a comprehensive, multi-layered system that integrates risk analysis, outreach, payment systems, and workflow orchestration. When these layers are combined, debt recovery becomes a predictable, working-capital function, not a reactive task.

Layer 1: Predictive Risk Scoring

Identify which accounts matter most. Predictive risk scoring evaluates repayment patterns and delinquency signals to prioritize accounts that need immediate attention. This ensures resources are directed to high-risk, high-reward accounts.

Layer 2: Intelligent, Multi-Channel Outreach

Move beyond single-channel outreach. Multi-channel communication (email, SMS, WhatsApp, voice) with personalized messaging ensures better engagement and faster recovery. AI determines the best timing and channel for outreach, improving response rates.

Layer 3: Unified Payments Platform

Make payments seamless with an integrated system. A unified payments platform allows immediate payments through links, secure portals, or installment options, ensuring higher conversion rates and faster recovery.

Layer 4: Autonomous Workflow Orchestration

Automate the entire process with intelligent workflows. Autonomous orchestration eliminates manual tasks, ensures timely follow-ups, and automates escalations based on borrower behavior and risk.

Layer 5: Recovery Intelligence Dashboard

Gain real-time visibility into recovery performance. Track key metrics like portfolio health, channel-level yield, and team efficiency. This data enables quick adjustments to strategies, ensuring recovery efforts are always optimized.

Why SMBs Need Agentic AI, Not Just Automation

Automation alone is task-based. It executes reminders but doesn’t make decisions or analyze real-time signals. Agentic AI goes further, it interprets borrower behavior, adapts strategies, and guides accounts toward repayment. Instead of just sending reminders, Agentic AI makes decisions, analyzes signals, and takes action like a digital collections operator.

For SMBs choosing AI debt collection services, Agentic AI is the game-changer. It transforms debt recovery into a strategic asset that can scale and deliver results immediately.

What Agentic AI Enables

Platforms such as FinanceOps Agentic AI combine multiple intelligence capabilities into a single execution system.

Best Time • Best Channel • Best Person

AI determines the optimal moment, communication channel, and contact to maximize engagement and right-party contact rates.

Live Sentiment Analysis

Real-time analysis of borrower tone and language helps detect confusion, hesitation, or hardship signals and adjust messaging accordingly.

Multilingual Omnichannel Communication

AI agents can interact two-way across email, SMS, voice, chat, and messaging platforms while maintaining context continuity across every interaction.

User-Controlled Strategy Builder

Collections teams can configure outreach strategies, escalation rules, and compliance guardrails while the AI executes those strategies automatically.

Automated Invoice Cycle

The platform manages the entire invoice lifecycle, from issuance and reminders to payment tracking and reconciliation.

Affordability-Based Payment Plans

Instead of demanding full repayment, AI can recommend installment structures based on behavioral patterns and repayment capacity (Weekly, Bi-weekly, or Monthly).

Must-Haves vs. Red Flags When Evaluating AI Debt Recovery Solutions

Must-Have Capabilities | Red Flags to Watch For |

Risk-based prioritization | Reminder-only communication systems |

Multi-channel outreach (email, SMS, voice) | Static outreach schedules |

Embedded payment infrastructure | No embedded payment options |

Adaptive communication logic | Rigid, non-adaptive workflows |

Real-time recovery analytics | Limited recovery visibility |

Integrated risk scoring and prioritization | No segmentation or prioritization |

What a Unified Payments + Agentic AI System Looks Like

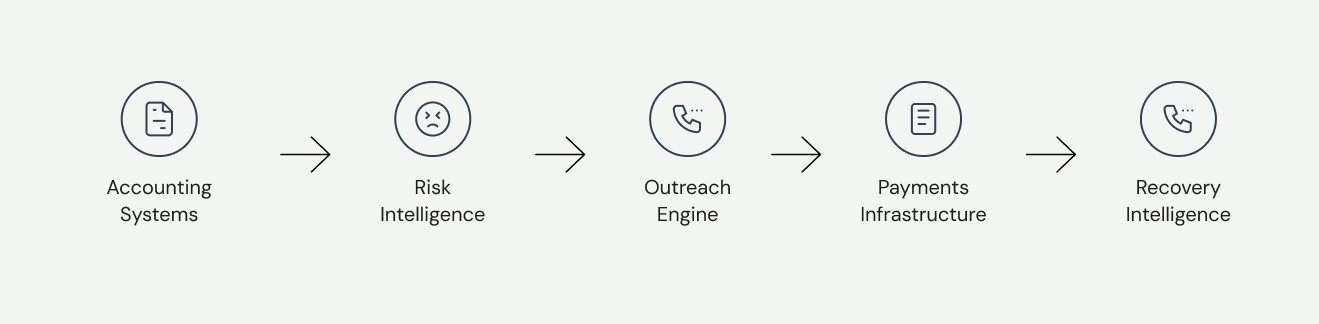

Accounting and Billing Data: Financial records provide real-time visibility into outstanding invoices, balances, and payment history.

Risk Intelligence Layer: AI models analyze repayment patterns and identify accounts with the highest liquidity impact.

Outreach Engine: Intelligent communication sequences engage borrowers through the most effective channels and timing.

Unified Payments Infrastructure: Embedded payment options allow customers to resolve balances immediately through secure links, portals, or installment plans.

Recovery Intelligence Layer: Real-time analytics measure recovery yield, channel performance, and portfolio health.

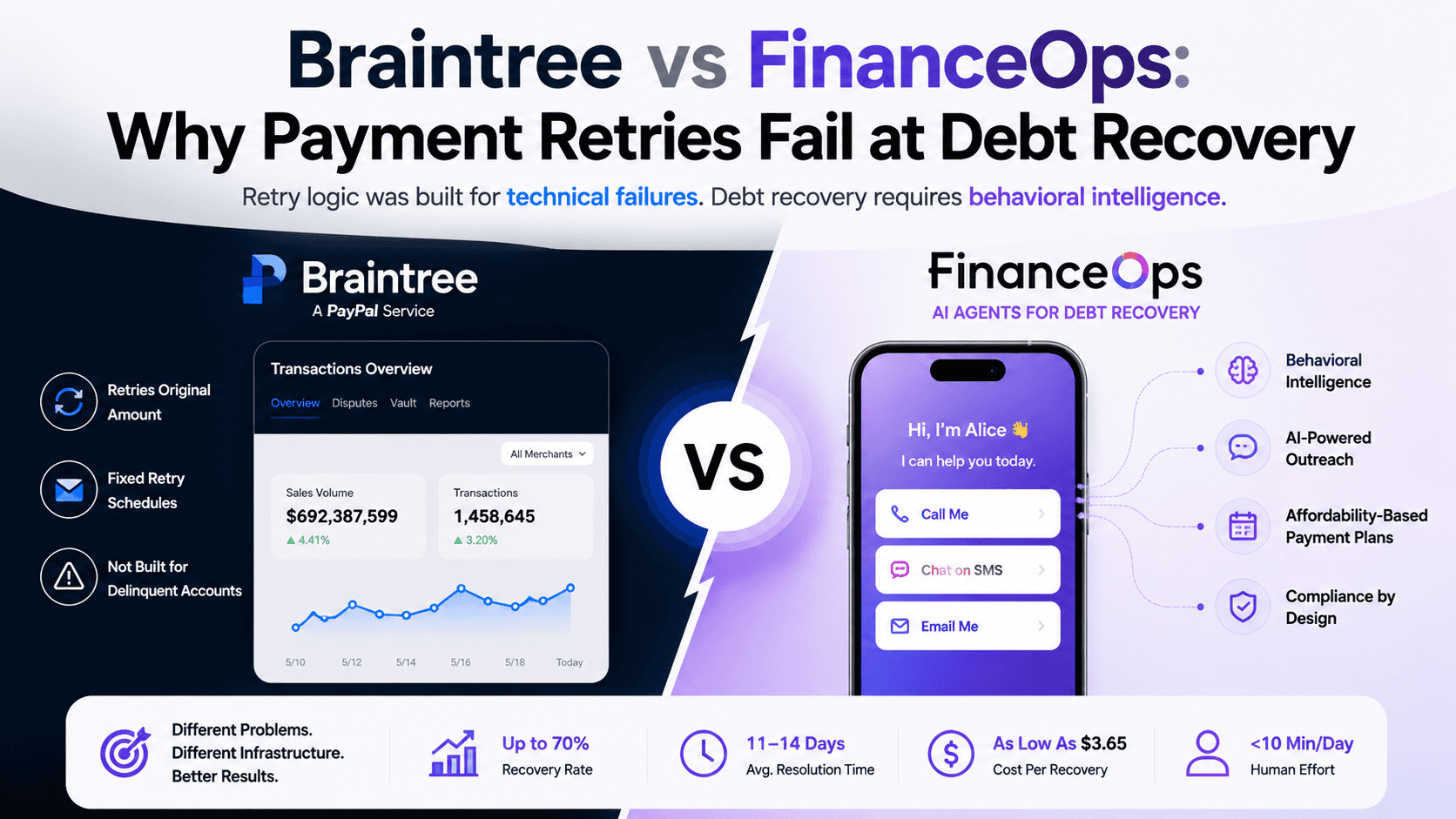

One-Layer Automation vs Agentic AI Automation

Capability | One-Layer Automation | Agentic AI Automation |

Core Function | Sends reminders and simple workflows | Acts as an execution layer for entire recovery |

Decision-Making | Rule-based triggers | AI-driven decisions based on real-time data |

Account Prioritization | Treats all accounts equally | Uses predictive risk scoring to prioritize high-value accounts |

Customer Segmentation | Minimal or static segmentation | Dynamic segmentation based on risk and behavior |

Communication Strategy | Fixed reminders | Multi-channel outreach with personalized messaging |

Payment Enablement | Separate from communication | Embedded payments with flexible options |

Adaptability | Static workflows | Continuously adapts based on engagement signals |

Escalation Logic | Limited escalation | Automated escalation based on risk |

Operational Effort | Requires frequent manual intervention | Mostly autonomous with minimal human oversight |

Recovery Visibility | Limited reporting | Real-time dashboards and performance insights |

Financial Impact | Marginal improvement | Higher recovery rates, lower DSO, and predictable cash flow |

Key Takeaway

The future of debt recovery is about intelligent execution. Agentic AI combines advanced analytics, multi-channel outreach, and real-time decision-making to optimize the entire recovery journey. Instead of replacing your current systems, FinanceOps seamlessly integrates to drive immediate results, improving recovery rates by up to 70% and reducing costs by 93%.

Ready to transform your debt recovery process? Book a 20-minute demo.

FAQs

Why does basic debt recovery automation fail?

Basic automation only sends reminders and lacks risk scoring, behavioral insights, and payment intelligence. Without segmentation or adaptive communication, engagement stays low, and many accounts remain uncollected.

What is a unified payments platform?

A unified payments platform integrates payment processing into collections workflows, allowing instant payments through secure links or portals, improving completion rates and speeding up cash recovery.

What are the best debt recovery solutions for SMBs?

Top solutions combine AI-driven risk scoring, multichannel communication, and embedded payments. These prioritize high-risk accounts, personalize outreach, and automate workflows, improving recovery rates and reducing costs.

How does AI improve debt recovery?

AI analyzes repayment behavior, optimizing outreach in real-time by selecting the best time, channel, and messaging for each customer, leading to higher engagement and faster payments.

What is agent-based automation?

Agent-based automation, or Agentic AI, uses autonomous digital agents to manage collections workflows.

Blog Summary: This blog explains why relying on single-layer automation (email reminders, dialers, and workflow triggers) falls short in debt recovery. Rising delinquencies, cash-flow pressure, and shifting borrower behavior in 2026 make traditional automation ineffective. We’ll show how SMBs lose collectible receivables and why automation alone isn’t enough. Learn how unified payments platforms and AI-driven solutions can deliver predictable, high-ROI recovery for SMBs.

Table of Contents:

Why One Layer of Automation Is Not Enough

The Debt Recovery Reality for Small Businesses in 2026

The Single-Layer Automation Trap (Why It Fails)

The Five Layers SMBs Actually Need for High-ROI Debt Recovery

Why SMBs Need Agentic AI, Not Just Automation

What Agentic AI Enables

Must-Haves vs. Red Flags When Evaluating AI Debt Recovery Solutions

What a Unified Payments + Agentic AI System Looks Like

One-Layer Automation vs Agentic AI Automation

Key Takeaway

FAQs

Why One Layer of Automation Is Not Enough

For most SMBs, the challenge isn’t that customers refuse to pay. It’s that their recovery systems can’t keep up with the demands of 2026. In the face of rising delinquencies, volatile repayment behavior, and shrinking cash buffers, traditional one-layer automation (like email reminders or dialers) simply isn’t enough. These systems execute tasks but don’t make decisions. They lack the intelligence needed to prioritize high-risk accounts or engage customers based on their individual repayment behavior.

By relying on single-layer systems, SMBs are allowing 60% of collectible receivables to slip through the cracks, leading to stretched cash cycles, tight liquidity, and expensive short-term financing. What SMBs need is more than just automation, they need intelligent, unified execution powered by Agentic AI. The future of debt recovery isn’t about more reminders; it’s about intelligent decision-making that drives recovery at scale.

The Debt Recovery Reality for Small Businesses in 2026

Small businesses are facing a tough landscape in 2026. Inflation, tighter credit conditions, and rising operational costs have made SMBs more vulnerable to delinquency risks.

Delinquencies are rising: Credit data from TransUnion and Experian show increased repayment stress, with customers rolling from 30-day to 60- and 90-day delinquency buckets.

Excess payment capacity is shrinking: The aggregated Excess Payment (AEP) indicator, which tracks a borrower’s ability to pay above the minimum, continues to decline, leaving less cushion for early-stage corrective actions.

Cash buffers are dangerously thin: The JPMorgan Chase Institute reports that most SMBs operate with less than 27 days of cash on hand, making even modest payment delays highly disruptive.

Manual collections processes and basic automation just can’t keep pace with these challenges. Without intelligent systems that understand borrower behavior, SMBs miss out on critical recovery windows.

The Single-Layer Automation Trap (Why It Fails)

Traditional debt recovery automation often revolves around sending automated reminders: a generic email, an SMS follow-up, and maybe a call after a few days. While this generates activity, it doesn’t produce meaningful results.

The problem is that reminder-only automation is task-focused, not decision-focused. It fails to interpret risk, understand borrower behavior, or guide accounts toward repayment. Effective debt recovery requires systems that can analyze signals and adjust strategies in real time, adapting to borrower intent and engagement.

Where Single-Layer Automation Breaks

No Segmentation: Treating all overdue accounts the same ignores risk levels and borrower behavior.

No Risk-Based Prioritization: Without predictive risk scoring, teams can’t focus on high-impact accounts.

No Predictive Outreach: Fixed schedules aren’t aligned with borrower behavior, reducing engagement.

No Payments Intelligence: Limited payment options create friction, reducing payment completion.

No Escalation Logic: Same messages are sent repeatedly, regardless of engagement signals.

No Affordability Modeling: Lacking flexible payment options, SMBs fail to convert constrained borrowers.

No Context Continuity: Multiple channels lack context, leading to repetitive, inefficient outreach.

Single-layer automation sends reminders but does not manage the repayment journey. Effective debt recovery requires coordination between risk signals, communication strategy, payment infrastructure, and affordability intelligence.

The Five Layers SMBs Actually Need for High-ROI Debt Recovery

Single-layer automation won’t suffice. SMBs need a comprehensive, multi-layered system that integrates risk analysis, outreach, payment systems, and workflow orchestration. When these layers are combined, debt recovery becomes a predictable, working-capital function, not a reactive task.

Layer 1: Predictive Risk Scoring

Identify which accounts matter most. Predictive risk scoring evaluates repayment patterns and delinquency signals to prioritize accounts that need immediate attention. This ensures resources are directed to high-risk, high-reward accounts.

Layer 2: Intelligent, Multi-Channel Outreach

Move beyond single-channel outreach. Multi-channel communication (email, SMS, WhatsApp, voice) with personalized messaging ensures better engagement and faster recovery. AI determines the best timing and channel for outreach, improving response rates.

Layer 3: Unified Payments Platform

Make payments seamless with an integrated system. A unified payments platform allows immediate payments through links, secure portals, or installment options, ensuring higher conversion rates and faster recovery.

Layer 4: Autonomous Workflow Orchestration

Automate the entire process with intelligent workflows. Autonomous orchestration eliminates manual tasks, ensures timely follow-ups, and automates escalations based on borrower behavior and risk.

Layer 5: Recovery Intelligence Dashboard

Gain real-time visibility into recovery performance. Track key metrics like portfolio health, channel-level yield, and team efficiency. This data enables quick adjustments to strategies, ensuring recovery efforts are always optimized.

Why SMBs Need Agentic AI, Not Just Automation

Automation alone is task-based. It executes reminders but doesn’t make decisions or analyze real-time signals. Agentic AI goes further, it interprets borrower behavior, adapts strategies, and guides accounts toward repayment. Instead of just sending reminders, Agentic AI makes decisions, analyzes signals, and takes action like a digital collections operator.

For SMBs choosing AI debt collection services, Agentic AI is the game-changer. It transforms debt recovery into a strategic asset that can scale and deliver results immediately.

What Agentic AI Enables

Platforms such as FinanceOps Agentic AI combine multiple intelligence capabilities into a single execution system.

Best Time • Best Channel • Best Person

AI determines the optimal moment, communication channel, and contact to maximize engagement and right-party contact rates.

Live Sentiment Analysis

Real-time analysis of borrower tone and language helps detect confusion, hesitation, or hardship signals and adjust messaging accordingly.

Multilingual Omnichannel Communication

AI agents can interact two-way across email, SMS, voice, chat, and messaging platforms while maintaining context continuity across every interaction.

User-Controlled Strategy Builder

Collections teams can configure outreach strategies, escalation rules, and compliance guardrails while the AI executes those strategies automatically.

Automated Invoice Cycle

The platform manages the entire invoice lifecycle, from issuance and reminders to payment tracking and reconciliation.

Affordability-Based Payment Plans

Instead of demanding full repayment, AI can recommend installment structures based on behavioral patterns and repayment capacity (Weekly, Bi-weekly, or Monthly).

Must-Haves vs. Red Flags When Evaluating AI Debt Recovery Solutions

Must-Have Capabilities | Red Flags to Watch For |

Risk-based prioritization | Reminder-only communication systems |

Multi-channel outreach (email, SMS, voice) | Static outreach schedules |

Embedded payment infrastructure | No embedded payment options |

Adaptive communication logic | Rigid, non-adaptive workflows |

Real-time recovery analytics | Limited recovery visibility |

Integrated risk scoring and prioritization | No segmentation or prioritization |

What a Unified Payments + Agentic AI System Looks Like

Accounting and Billing Data: Financial records provide real-time visibility into outstanding invoices, balances, and payment history.

Risk Intelligence Layer: AI models analyze repayment patterns and identify accounts with the highest liquidity impact.

Outreach Engine: Intelligent communication sequences engage borrowers through the most effective channels and timing.

Unified Payments Infrastructure: Embedded payment options allow customers to resolve balances immediately through secure links, portals, or installment plans.

Recovery Intelligence Layer: Real-time analytics measure recovery yield, channel performance, and portfolio health.

One-Layer Automation vs Agentic AI Automation

Capability | One-Layer Automation | Agentic AI Automation |

Core Function | Sends reminders and simple workflows | Acts as an execution layer for entire recovery |

Decision-Making | Rule-based triggers | AI-driven decisions based on real-time data |

Account Prioritization | Treats all accounts equally | Uses predictive risk scoring to prioritize high-value accounts |

Customer Segmentation | Minimal or static segmentation | Dynamic segmentation based on risk and behavior |

Communication Strategy | Fixed reminders | Multi-channel outreach with personalized messaging |

Payment Enablement | Separate from communication | Embedded payments with flexible options |

Adaptability | Static workflows | Continuously adapts based on engagement signals |

Escalation Logic | Limited escalation | Automated escalation based on risk |

Operational Effort | Requires frequent manual intervention | Mostly autonomous with minimal human oversight |

Recovery Visibility | Limited reporting | Real-time dashboards and performance insights |

Financial Impact | Marginal improvement | Higher recovery rates, lower DSO, and predictable cash flow |

Key Takeaway

The future of debt recovery is about intelligent execution. Agentic AI combines advanced analytics, multi-channel outreach, and real-time decision-making to optimize the entire recovery journey. Instead of replacing your current systems, FinanceOps seamlessly integrates to drive immediate results, improving recovery rates by up to 70% and reducing costs by 93%.

Ready to transform your debt recovery process? Book a 20-minute demo.

FAQs

Why does basic debt recovery automation fail?

Basic automation only sends reminders and lacks risk scoring, behavioral insights, and payment intelligence. Without segmentation or adaptive communication, engagement stays low, and many accounts remain uncollected.

What is a unified payments platform?

A unified payments platform integrates payment processing into collections workflows, allowing instant payments through secure links or portals, improving completion rates and speeding up cash recovery.

What are the best debt recovery solutions for SMBs?

Top solutions combine AI-driven risk scoring, multichannel communication, and embedded payments. These prioritize high-risk accounts, personalize outreach, and automate workflows, improving recovery rates and reducing costs.

How does AI improve debt recovery?

AI analyzes repayment behavior, optimizing outreach in real-time by selecting the best time, channel, and messaging for each customer, leading to higher engagement and faster payments.

What is agent-based automation?

Agent-based automation, or Agentic AI, uses autonomous digital agents to manage collections workflows.

4 minutes

Posted by

Arpita Mahato

Content Writer

Other Blogs

View other blogs

Stay Updated with Us

Enter your email below and subscribe to our weekly newsletter

Instant Access

Boost Productivity

Easy Setup

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps

Transform Your Financial Processes

Join thousands of businesses already saving time and money with FinanceOps