Introduction: Delinquent Loans vs. Defaults

Whether you're a business owner, financial institution, or individual borrower, knowing the distinction between delinquency and default is essential for managing debt responsibly. While both terms involve missed payments, they differ significantly in terms of severity, legal consequences, and impact on creditworthiness. Grasping these differences can help stakeholders mitigate risk, protect financial health, and make informed decisions when navigating loan agreements or credit obligations.

What Is a Delinquent Loan?

A delinquent loan refers to any loan where the borrower has failed to make one or more scheduled payments by the due date. Even being one day late can place a loan in delinquent status. Lenders closely monitor the duration and severity of delinquency, and this information is reported to credit bureaus, often beginning once a payment is 30 days past due. If the delinquency continues long enough, the lender may charge off the loan (typically after 120–180 days), which results in an additional negative mark on the borrower’s credit history.

Key Implications of Loan Delinquency

Late Fees and Penalties: Lenders may charge additional fees once a payment is past due.

Credit Score Impact: Payment history is a major factor in credit scoring, and even short-term delinquencies can hurt your score.

Lender Collection Actions: Financial institutions may begin outreach or initiate early-stage collection efforts to recover missed payments on unpaid invoices.

How to Resolve Delinquency:

The good news is that delinquency can often be resolved. Borrowers can bring the account current by paying the overdue amount plus any applicable fees, restoring the loan to good standing and preventing further negative consequences.

What Is a Default?

A loan default occurs when a borrower fails to fulfill the terms of a loan agreement over an extended period, typically after multiple missed payments on outstanding amounts. While delinquency signals a late or missed payment, default represents a more serious failure, often defined by the loan contract or regulatory standards, and usually triggers formal recovery actions by the lender, such as collections, acceleration of the loan balance, or legal proceedings.

Default Definition:

A loan is considered in default when the borrower has not made payments for a specified duration, commonly 90 days for most loans and 270 days for federal student loans. At this point, the lender may declare the loan in default, initiating aggressive recovery or legal measures.

Major Consequences of Default:

Immediate Acceleration of Debt: The full remaining loan balance may become due at once.

Severe Credit Damage: Defaults cause long-lasting harm to credit scores, making future borrowing more difficult.

Legal and Financial Repercussions: Lenders may pursue lawsuits, wage garnishment, or seize tax refunds to recover the debt.

Loss of Borrower Protections: Defaulted borrowers may become ineligible for deferment, forbearance, or new lines of credit.

How Long Does a Default Stay on a Credit Report?

A default can remain on a borrower's credit report for up to seven years, even if the debt is eventually repaid or settled. This extended presence can limit access to financing, employment opportunities, and housing.

Key Differences Between Delinquency and Default

While both delinquency and default involve missed loan payments, they represent different stages of repayment failure and carry distinct implications. Understanding these differences is crucial for managing financial risk like charge-offs and avoiding long-term damage to credit health.

In terms of credit impact, delinquency may cause a temporary dip in a credit score, but it can often be corrected if addressed promptly. A default, however, signals a breakdown in the repayment relationship and is much harder to recover from.

In short:

Delinquency is a warning.

Default is a red flag with legal and financial consequences.

Pro-Tip: Being able to distinguish between these two stages is essential for borrowers to avoid escalation.

Why Understanding Delinquency and Default Matters

Delinquency and default aren’t just financial terms, they represent critical warning signs in a borrower’s credit journey. Recognizing the difference and acting early can mean the difference between a short-term setback and a long-term financial crisis.

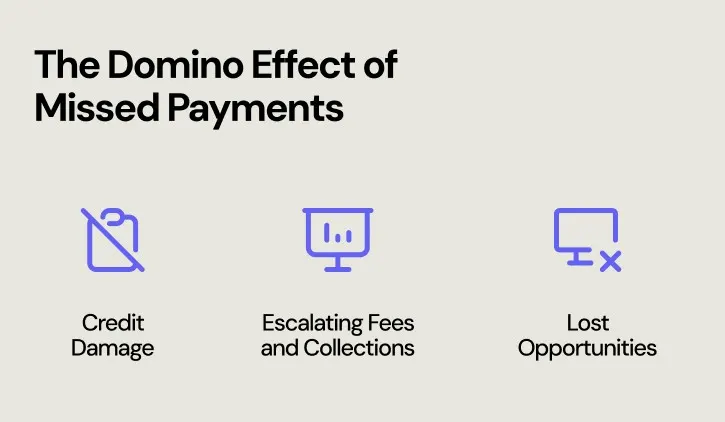

The Domino Effect of Missed Payments

Delinquency begins quietly, with a missed payment. But if left unresolved, it can spiral into default, triggering serious consequences:

Credit Damage: A single missed payment can lower a borrower’s credit score, making future credit more expensive or even inaccessible.

Escalating Fees and Collections: Delinquency often leads to mounting fees, while default may result in legal action or debt recovery through wage garnishment.

Lost Opportunities: Defaults can disqualify borrowers from federal aid, employment screenings, or new credit products.

What starts as a small oversight can quickly escalate into a financial barrier that lingers for years.

What Borrowers Should Do

Whether you're behind on a payment or already in default, it’s not too late to take control:

Take Immediate Action: Delinquency is most manageable in the early stages, don’t wait for it to worsen.

Engage with Your Lender: Lenders often have programs for borrowers facing financial hardship. Options like forbearance, deferment, or loan restructuring may be available.

Stay Credit-Aware: Regularly review your credit reports to catch errors and stay informed about the status of your accounts.

Seek Support: If you're overwhelmed, consult a certified credit counselor or explore debt relief programs.

Federal Loan Borrowers: Special Risks

Delinquency on federal debt carries unique consequences. If you owe back taxes or are behind on federal student loans:

You must disclose it when applying for new federal loans or guarantees.

The government can intercept tax refunds or garnish wages without court orders.

Federal defaults may affect access to public assistance or employment with government-linked agencies.

Final Thought: Prevention is Power

Missing a payment doesn’t have to derail your financial future, but inaction might. Understanding the difference between delinquency and default empowers borrowers to take early, informed steps. For businesses, financial institutions, and individual borrowers alike, staying proactive is the most effective way to protect your credit, your reputation, and your financial goals.

Take Control Before It’s Too Late

Delinquency doesn’t have to turn into default. Whether you manage loans for a business, nonprofit, or financial institution, FinanceOps.ai helps you act fast with AI-powered automation for early-stage collections, payment reminders, and dispute management.

Avoid charge-offs. Protect your cash flow. Maintain borrower relationships.

Start your journey with Financeops today.

FAQs

1. What is the difference between a delinquent loan and a defaulted loan?

A delinquent loan occurs when a borrower misses a payment but still has a chance to catch up. A default happens after prolonged non-payment, typically 90+ days, and signals a breakdown in the loan agreement, often triggering legal or aggressive collection actions.

2. How does loan delinquency affect my credit score and borrowing power?

Even a single missed payment can negatively impact your credit score. While early-stage delinquency is often recoverable, if ignored, it can evolve into default, leading to long-term credit damage and reduced access to future financing or institutional programs.

3. Are you delinquent on any federal debt, what does this mean for institutions and individuals?

Federal debt delinquency, such as unpaid taxes or federal student loans, must be disclosed on applications for new government funding or guarantees. It can result in wage garnishment or tax refund seizure, especially for public-sector employees or institutions seeking federal aid.

4. How long does a loan default stay on a credit report?

A default can remain on your credit report for up to seven years, even if you repay the debt later. This extended negative mark may affect loan approvals, interest rates, and eligibility for public programs or housing.

5. What steps should borrowers take if they are delinquent or in default?

Act immediately: Contact your lender to discuss hardship programs or restructuring options. Monitor your credit reports, pay overdue balances when possible, and consider credit counseling. The earlier you respond, the better your chances of recovery and avoiding legal consequences.