A payment plan is really just a promise to pay. This article covers how that promise gets made, and what happens, for better or worse, when AI is the one helping keep it.

TL;DR

Medical payment plans let patients repay bills in manageable installments, but availability and terms vary widely by provider.

When a plan breaks down, the path runs through a dispute or a collections recovery service. Both are just a promise to pay being renegotiated, not lost revenue.

FinanceOps Agentic AI automates that entire lifecycle: building affordable plans, reaching patients on the right channel at the right time, and staying compliant automatically.

What Is a Payment Plan for Medical Bills?

A medical payment plan is a written agreement that breaks a bill into smaller, scheduled payments instead of requiring the full balance at once.

Example: A $4,800 hospital bill might become 12 monthly payments of $400, or 24 payments of $200.

Where plans come from: directly from a hospital or practice's billing office, through a third-party financing partner, or via a recovery service once an account has aged past the standard billing cycle.

What varies by provider: plan length, payment frequency, whether a down payment is required, and whether interest applies.

Example range: a large academic medical center might offer a 36-month interest-free plan with no down payment for financial-assistance-qualified patients, while a small private practice might offer only a 6-month plan with a 20% deposit upfront.

Because terms vary this widely, it's worth confirming the exact agreement in writing before signing anything.

Do Most Hospitals Offer Payment Plans for Medical Bills?

Yes, most hospitals offer some version of a payment plan, and nonprofit hospitals are generally required to under IRS rules on financial assistance and community benefit.

Not universal: smaller independent practices, urgent care clinics, and specialty providers (dermatology, dental, fertility) aren't bound by the same rules.

Common workaround: providers without an in-house billing office often refer patients to a third-party financing company instead, which functions more like a loan than a provider-managed plan.

Best practice: call the billing department directly, since plan availability is rarely advertised upfront.

How Do I Apply for a Payment Plan to Cover Medical Bills?

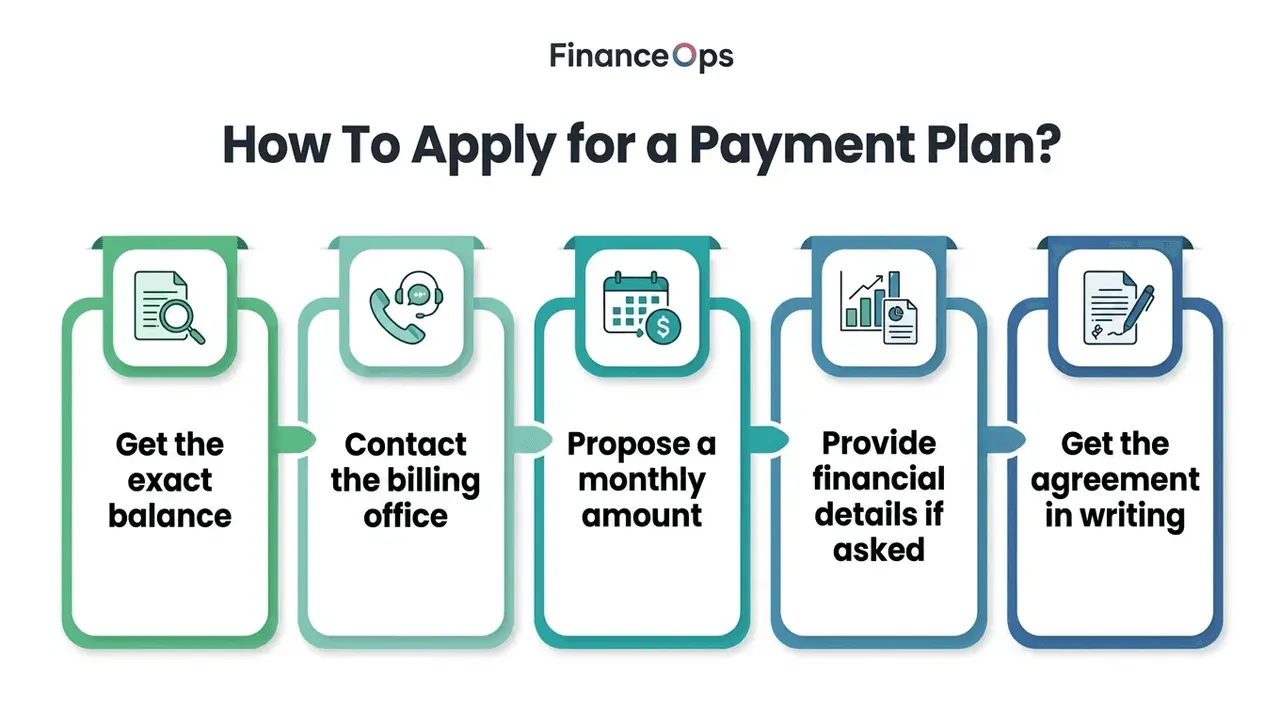

Applying for a payment plan generally follows a predictable sequence:

Get the exact balance: Confirm the bill is finalized and that insurance has already processed the claim, since applying before that can mean negotiating the wrong number.

Contact the billing office: Call, use the patient portal, or visit in person, and ask specifically about payment plan options rather than just asking how to pay.

Propose a monthly amount: Most billing offices will ask what's affordable and work from there, rather than dictating a fixed number.

Provide financial details if asked: Some providers require a short income and expense disclosure to qualify for reduced rates or interest-free terms.

Get the agreement in writing: This should spell out the start date, the installment amount, the payment method (often autopay), and what happens if a payment is missed.

The whole process can often be completed in a single call or portal session, especially for smaller balances.

How Do Interest-Free Payment Plans Work?

An interest-free plan simply divides the balance evenly across a set number of payments with no finance charge added.

Example: a $3,000 bill on a 12-month interest-free plan comes out to exactly $250 a month, no more.

Why providers offer them: a predictable, on-time payment is worth more to them than the small amount of interest they'd otherwise collect, and it lowers the odds of the account reaching collections.

The catch to watch for: many interest-free agreements include a clause that converts the plan to a standard (interest-bearing) structure, or refers the balance to a recovery service, after a set number of missed payments.

Reading that clause before signing is the easiest way to avoid an unpleasant surprise later.

When a Payment Plan Isn't Enough: Disputes and Collections Recovery

A payment plan assumes the bill itself is correct. When it isn't, or when a plan falls apart and goes unpaid, the situation moves into one of two related but different processes: disputing the bill, or having it handed to a collections recovery service.

What Services Help Recover Unpaid Medical Bills?

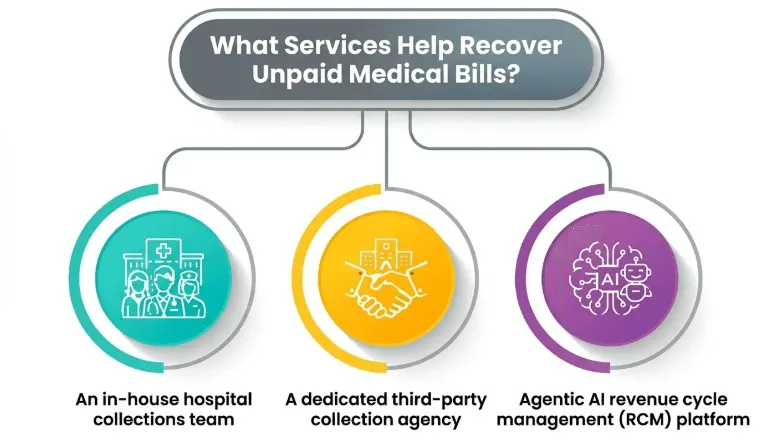

When an account ages past a provider's internal billing timeline, usually somewhere between 90 and 180 days, it typically moves to one of three places:

An in-house hospital collections team that continues outreach internally.

A dedicated third-party collection agency that specializes in healthcare debt.

Agentic AI revenue cycle management (RCM) platform that automates much of that re-engagement.

Their job is the same regardless of who's doing it: re-contact the patient, confirm the balance is accurate, and negotiate a new, workable repayment arrangement. Most providers treat credit reporting or legal action as a last resort, since both damage the patient relationship and rarely improve recovery odds.

Steps to Dispute an Incorrect Medical Bill

If a bill looks wrong, the process generally looks like this:

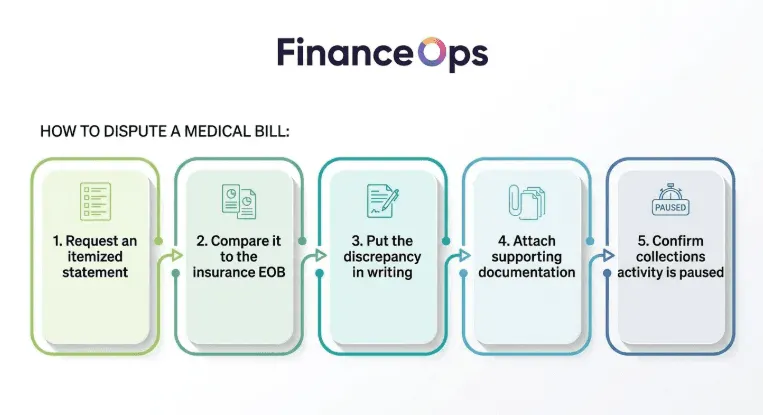

Request an itemized statement: A summary balance won't show individual charges; ask specifically for the line-by-line breakdown.

Compare it to the insurance Explanation of Benefits (EOB): This is where duplicate charges, services never received, or incorrect billing codes usually surface.

Put the discrepancy in writing: A phone call alone rarely creates a record; a written dispute (email or portal message) with the specific line items flagged carries more weight.

Attach supporting documentation: Appointment records, discharge paperwork, or the EOB itself all help substantiate the claim.

Confirm collections activity is paused: Providers are generally required to hold off on further collections action while a documented dispute is actively under review.

Anyone handling that documentation must restrict access to the minimum PHI necessary under HIPAA's Minimum Necessary Rule.

Routing a dispute file to staff outside the billing workflow can itself constitute an access-control violation.

Why Insurance-Related Disputes Are Becoming More Common

A growing share of disputed bills trace back to insurer behavior rather than provider error. Under the No Surprises Act (NSA) and its independent dispute resolution (IDR) process, physicians can challenge an insurer's payment determination, but:

The American Medical Association has reported that insurers increasingly reprocess claims after losing an IDR decision, shifting the cost back onto the patient's bill after the dispute was supposedly resolved.

The AMA has also flagged widespread delays in the statutory 30-day payment window following an IDR win, meaning a balance a patient assumed was settled can resurface weeks or months later as a new, disputed charge.

For collections teams, this matters operationally: an account flagged as resolved can re-enter the dispute queue through no fault of the patient or the billing staff, exactly the kind of edge case a manual, spreadsheet-based process is slow to catch.

How Do I Dispute a Medical Bill With a Recovery Service?

If the account has already moved to a recovery service, the same documentation process applies, but the request goes through the recovery partner instead of the original billing office.

Recovery services are required to verify the debt and provide supporting records on request before continuing collection efforts.

Any PHI included in that exchange falls under the HIPAA Security Rule's transmission safeguards: a recovery partner sharing records over an unencrypted channel, even internally, is a Security Rule gap regardless of whether the underlying debt is valid.

Where Can I Find Companies Specializing in Medical Bill Recovery?

Provider billing departments can usually name the recovery partner handling a specific account. Beyond that, healthcare revenue cycle management directories and state medical billing associations are a more reliable starting point than a general search.

Under the HIPAA Omnibus Rule, any recovery agency handling PHI on a provider's behalf is a business associate.

It must operate under an executed Business Associate Agreement (BAA) before a single record changes hands.

A recovery vendor without a signed BAA is itself a compliance gap, independent of how well it performs.

Step back, and every section above describes the same underlying event: a promise to pay, made or renegotiated. A payment plan is a P2P set up proactively. A dispute is a P2P paused for verification. A collections recovery case is a P2P being rebuilt after it broke down. Most providers manage all three manually, across spreadsheets, call queues, and disconnected billing systems. That's exactly where the friction, and the missed revenue, comes from. This is the problem agentic AI is built to solve.

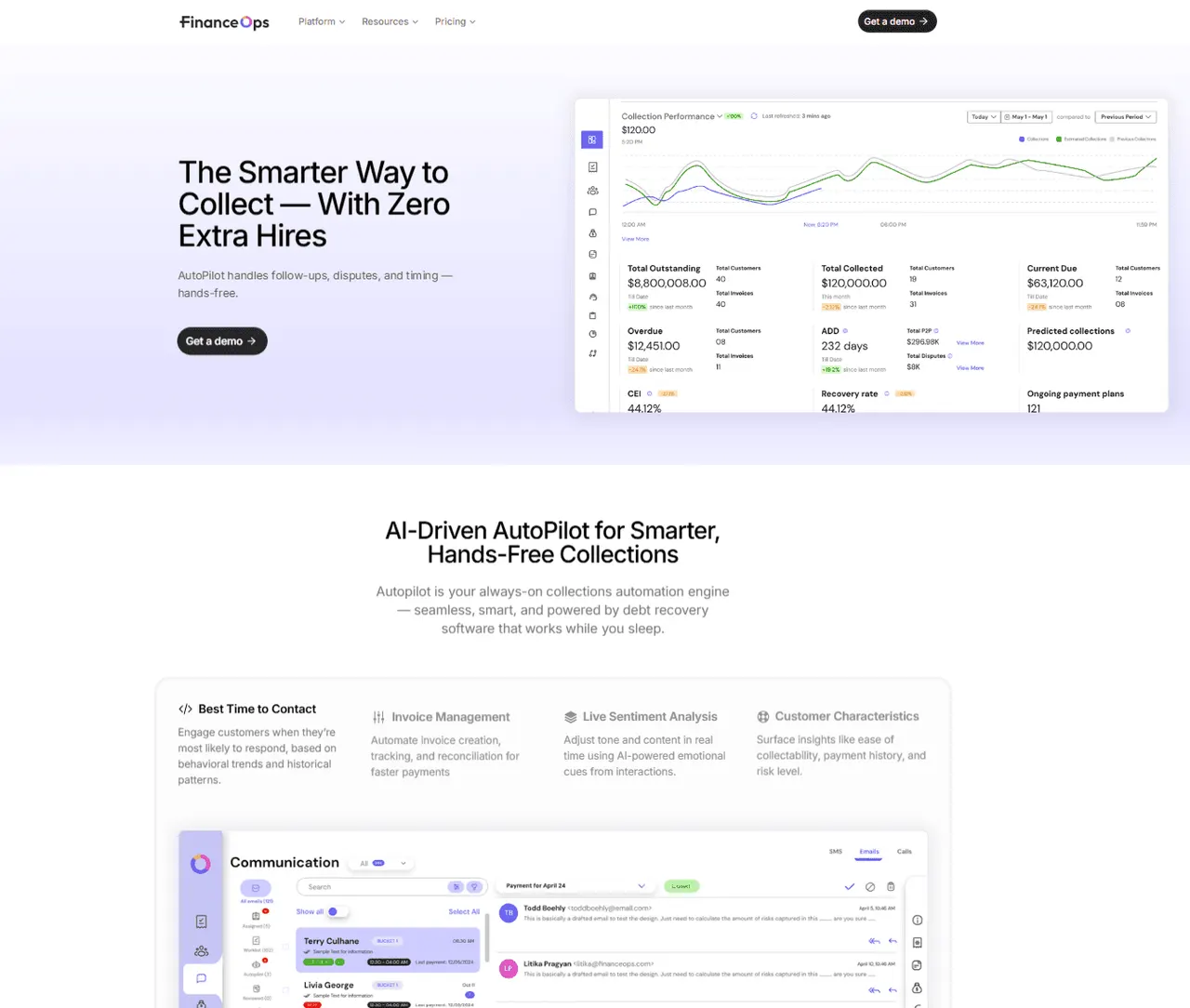

How FinanceOps Agentic AI Automates Collections Recovery

Agentic AI refers to systems that don't just answer questions but take action, within rules a human team has defined in advance:

Initiating outreach

Adjusting a payment plan

Escalating a flagged dispute

Applied to healthcare revenue cycle management, this is what we call FinanceOps Agentic AI: a system built specifically to manage the promise-to-pay lifecycle from first contact through final payment, rather than a generic chatbot bolted onto a billing portal. The capabilities below describe what actually makes a promise to pay stick, and why that takes more than automation alone.

The Six Core Capabilities of FinanceOps Agentic AI

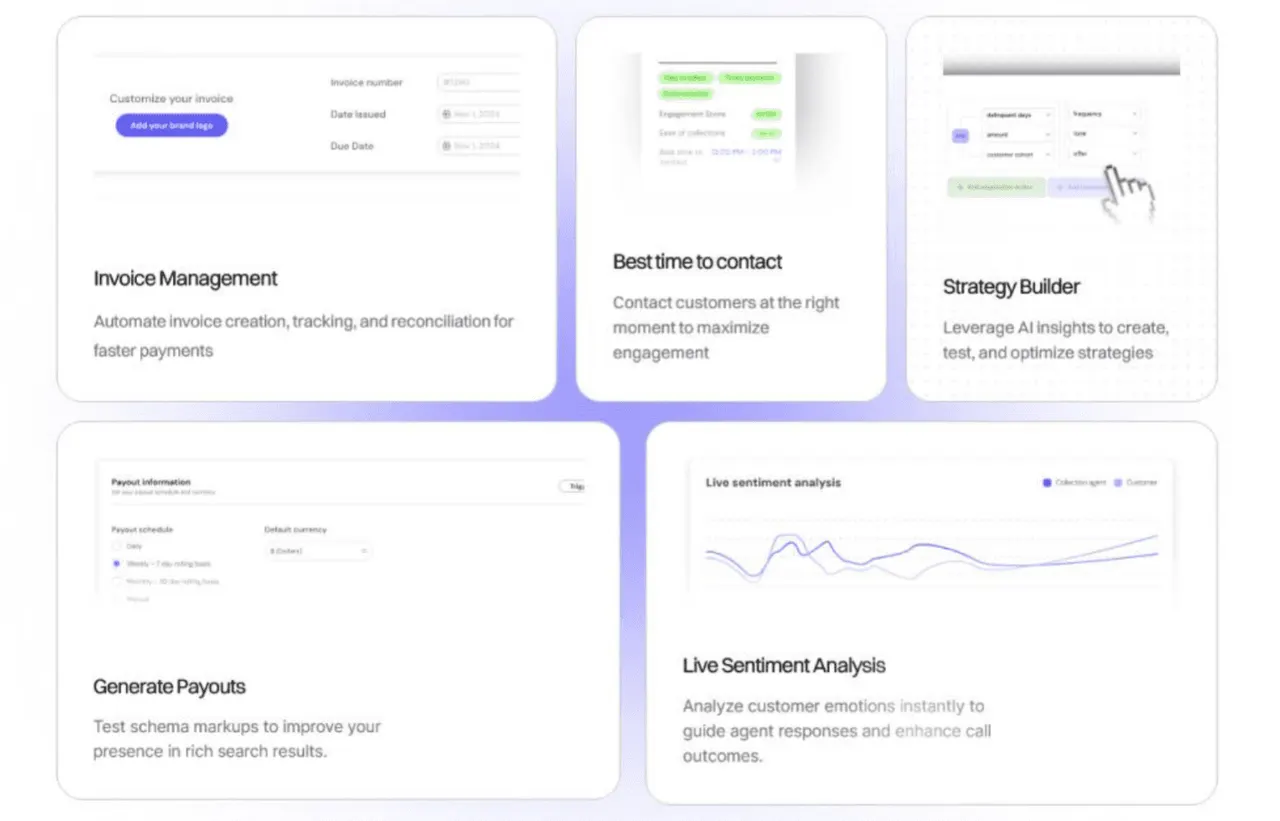

1. Affordability-Based Flexible Payment Plans

FinanceOps builds each plan around what a patient can realistically pay, using account and repayment history instead of a generic template.

Offers weekly, bi-weekly, monthly, or fully custom schedules.

Generated in the moment a patient is already engaged, rather than after a multi-day manual review.

Plans built this way are less likely to collapse midway through, which is usually where liquidation rates move the most.

2. Two-Way, Omnichannel, Multilingual Communication

Patients can move between SMS, email, voice, webchat, and the portal without losing context or repeating themselves.

Communicates in the patient's preferred language rather than defaulting to English.

Results in fewer abandoned applications and fewer accounts lost because the channel didn't fit the patient.

Closes a common HIPAA exposure point: manually re-keying patient details on a channel handoff is how a Use and Disclosure violation happens (for example, a balance or diagnosis-linked charge read out to the wrong contact-of-record). A single, context-persistent thread removes that re-keying step entirely.

3. Automated Invoice Management

Invoice issuance, payment retries, reconciliation, and dispute routing all run continuously rather than in a manual batch process. A missed payment or flagged discrepancy gets caught and acted on the same day, instead of sitting unresolved for weeks.

4. Best Time, Best Channel, Best Person to Contact

FinanceOps learns when a specific patient is likely to respond and on which channel, and knows when to route a sensitive case to a human agent instead of automating it.

Lifts right-party-contact rates and ends the repeated, badly timed calls patients usually associate with collections.

Has a direct compliance dimension: disclosing balance or treatment details to the wrong person on the account is the Use and Disclosure violation category that drove the Mount Sinai–St. Luke's $387,000 HIPAA settlement, where PHI was shared with an unauthorized party.

5. Live Sentiment Analysis

The system reads tone, hardship cues, and escalation language in real time and adjusts its approach accordingly, catching distress before a dispute becomes a formal complaint.

A customer-experience safeguard: prevents another automated nudge from landing on someone already struggling.

A compliance safeguard: under the TCPA, a request to stop contact must be honored, and failing to detect that signal in real time is an enforcement risk independent of the underlying debt's validity.

6. User-Controlled Strategy Builder

Every cadence, message template, and compliance guardrail, including TCPA and FDCPA contact limits, is set by the provider's own team inside the Strategy Builder. The AI executes within those boundaries; it never defines or overrides them.

Enforces HIPAA's Minimum Necessary Rule and Access Controls operationally: a payment-reminder workflow doesn't have standing access to clinical notes it has no reason to read.

Any business associate relationship the platform creates is documented under a signed BAA per the HIPAA Omnibus Rule before any PHI is exchanged.

Why a Governed Agentic System Beats a Pre-Trained AI Model

A generic, pre-trained AI model can draft a fluent message or hold a conversation, but it doesn't carry:

TCPA contact-frequency constraints

FDCPA disclosure language

HIPAA's Minimum Necessary and Access Control standards

A provider's specific SOPs

Any mechanism for detecting a hardship signal and adjusting accordingly

That gap is exactly what the Strategy Builder and Live Sentiment Analysis are built to close, by encoding compliance logic and real-time tone detection as enforced constraints on the model's output, not as suggestions it can ignore. In regulated collections work, governed intelligence beats generic intelligence.

The Business Impact: Better Promises, Better Outcomes

Together, these capabilities reshape the entire promise-to-pay funnel:

More affordable plans mean more promises get made in the first place.

Sentiment-aware outreach means more of those promises get kept.

Continuous invoice management means fewer accounts age unnecessarily while waiting on a human to notice an issue.

The result providers typically see: higher liquidation rates, lower roll rates, and fewer compliance complaints, the same outcomes a manual process aims for, just reached with far less friction.

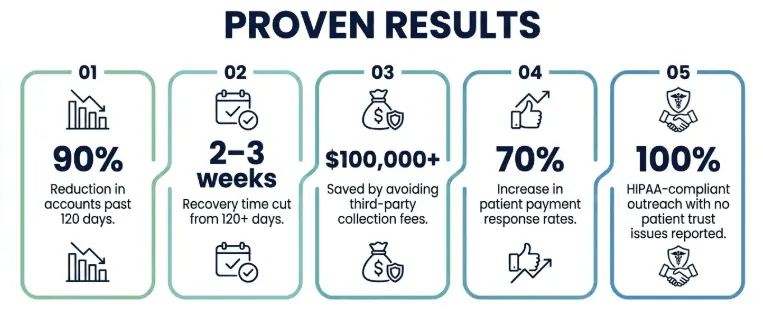

How Enamel Dentistry Cut 120-Day Delinquencies by 90%

Enamel Dentistry, a multi-location practice in Austin, Texas, had a category of accounts most providers simply write off: balances between $100 and $250, more than 120 days past due.

In-house staff couldn't justify the ROI on accounts that small.

Third-party agencies charged 30 to 40 percent in fees, making outsourcing nearly as costly as the write-off itself.

Using FinanceOps' Autopilot AI, applying affordability-aware outreach, best-time-to-contact targeting, live sentiment analysis, and automated invoice management directly to that low-balance segment, Enamel saw within 18 months:

90% cost reduction in accounts past 120 days.

Recovery time cut from 120+ days to 2–3 weeks.

$100,000+ saved by avoiding third-party collection fees.

70% increase in patient payment response rates.

100% HIPAA-compliant outreach throughout, with no patient trust issues reported.

As Enamel's Operations Manager put it, the results let the practice "focus on delivering care, not chasing payments." The case illustrates the core argument of this article in practice: a governed agentic system doesn't just automate outreach, it makes previously unprofitable accounts worth collecting, without adding headcount or compliance risk.

Key Takeaways

A payment plan only succeeds when it's built around real affordability, not a generic installment template.

Disputes and collections recovery are renegotiated promises, not lost revenue. When the process is managed well, most of that balance is still recoverable.

Governed agentic AI, not generic AI, is what makes automation safe and trustworthy in a regulated environment like healthcare billing.

See How FinanceOps Agentic AI Works for Your Team

Every payment plan is a promise. FinanceOps Agentic AI is built to help your team keep more of them, with affordable terms, the right outreach at the right time, and full compliance control, without adding headcount or risk to your collections process.

Schedule a FinanceOps demo to see it on your own accounts.

FAQs

Who pays a medical bill when a patient genuinely can't afford it?

When a patient can't pay, the balance doesn't disappear. It typically moves through financial assistance programs, charity care policies (common at nonprofit hospitals), Medicaid retroactive coverage, or, eventually, collections recovery. Providers generally exhaust internal payment plans and assistance options before an account is referred externally.

Do dental payment plans work differently from medical payment plans?

The mechanics are largely the same (installments based on the balance and an agreed schedule), but dental practices are more likely to be smaller, independent offices without an in-house billing department, so dental payment plans more often run through a third-party financing partner rather than the practice itself.

What happens if I miss a payment on a medical payment plan?

Most plans allow a grace period before the account is flagged, but repeated missed payments can convert an interest-free plan into a different repayment structure or trigger a referral to a collections recovery service. Contacting the provider before a payment is missed is almost always better than after.

Can AI collections systems replace a billing team entirely?

No, and that's by design. FinanceOps Agentic AI is built to execute within rules a billing and compliance team sets through the Strategy Builder, and to escalate sensitive or complex cases to a human agent. It removes manual, repetitive work rather than removing the team's oversight.