Most lenders still treat delinquency like a single event instead of a clock that starts ticking the second a payment is missed. That mistake is exactly why recovery rates stay stuck near 2%, and why the data below shows it's getting worse, not better, in the segment that matters most right now: below-prime auto.

Blog Summary

A loan is delinquent the moment a payment is missed, not after 30 or 60 days, that's just when it gets reported.

Delinquency and default are not the same thing. Default takes far longer to trigger, 90 days for most consumer loans, 270 days for federal student loans, and is much harder to reverse.

Below-prime auto loans are the clearest live example of delinquency stress in 2026: extension rates and extension interest rates are both climbing, and the borrowers receiving extensions are paying down principal slower than ever.

The first 15 to 60 days past due is the highest-leverage recovery window for lenders. Most legacy collections infrastructure ignores it completely.

AI collections platforms close that gap by predicting the right time, channel, and contact for each borrower, then adapting in real time based on sentiment and behavior.

A live deployment at LA Federal Credit Union took right-party contact rates from ~2% to 12-15% and recovered over $8M in 30 days, with under 10 minutes of human effort per day.

Delinquent Loan vs. Default: What's the Difference?

Most explanations online blur this line on purpose, it makes the lender look more lenient than they actually are. Delinquency and default are legally and operationally distinct, and the gap between them is the entire window in which a loan is still cheaply recoverable.

Every defaulted loan was delinquent first. Not every delinquent loan defaults. The entire economic case for early-stage AI collections rests on that second sentence.

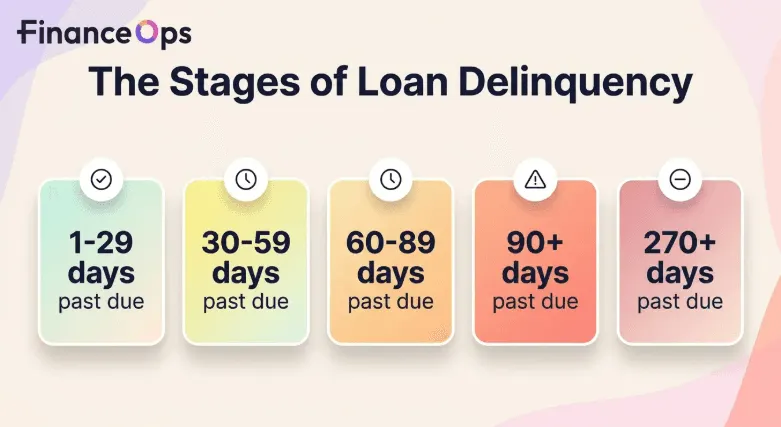

Five Stages of Loan Delinquency

Delinquency isn't binary, it's a curve, and where a lender intervenes on that curve determines almost everything about cost and recovery probability.

1-29 days past due: Technically delinquent, rarely reported yet. Most lenders allow a short grace window here.

30-59 days past due: Now on the credit report for most consumer loan types. Late fees compound. This is where most "automated" collections systems stop, sending a generic reminder and hoping.

60-89 days past due: Default risk accelerates sharply. Contact gets harder, and every week of delay raises the cost of eventual recovery.

90+ days past due: Personal loans and mortgages typically cross into default territory here. Auto loans move toward repossession exposure.

270+ days past due: Federal student loans officially default, by far the longest runway of any common loan category.

The cost of recovery doesn't rise linearly with days past due, it rises exponentially. An account at 20 DPD might cost a few dollars to recover through a well-timed text. The same account at 75 DPD might require multiple call attempts, a negotiated settlement, and possibly a third-party agency, at ten to twenty times the cost, for worse odds.

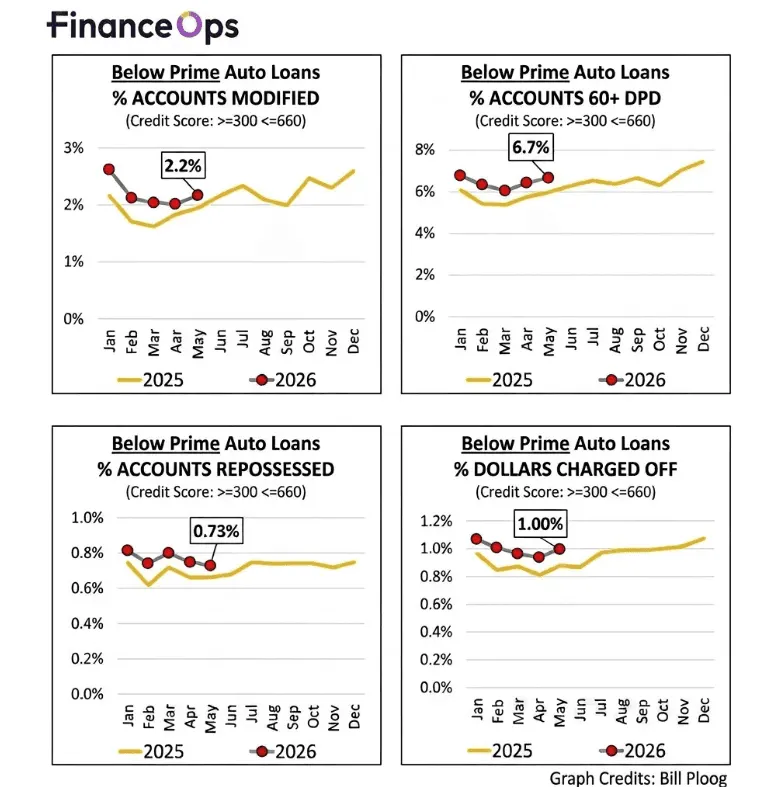

Live Proof of the Problem: Below-Prime Auto Loans in May 2026

Delinquency curves can sound abstract until you look at a portfolio that's actually deteriorating in real time. Below-prime auto loans, those held by borrowers with credit scores between 300 and 660, are the clearest current example, and the SEC filing data tells an uncomfortable story.

According to an analysis of corporate-officer-attested ABS-EE filings submitted to the SEC via EDGAR, the below-prime auto segment continued to weaken through May 2026:

The analysis covers roughly 1.3 million below-prime auto loans outstanding, worth about $24.9 billion, as of May 2026, drawn from the four major servicers and lenders that had filed their May 2026 data with the SEC at the time: Bridgecrest, CarMax, Carvana, and Santander.

Year-over-year, the key stress indicators kept climbing, consistent with the multi-year, record-setting trend that has defined this segment since 2025.

The extension data is where it gets worse. A separate look at roughly 2.3 million below-prime auto loans that had been extended, spanning lenders including Ally, Bridgecrest, CarMax, Carvana, Exeter, Ford, GM, Honda, Hyundai, Nissan, Santander, Toyota, Volkswagen, and World Omni, found that:

The median interest rate on extended below-prime auto loans sat at 21% as of April 2026.

The middle 50% of extended loans (the second-to-third quartile band) has widened and shifted higher over time. The top of that band now approaches 25%, and even the bottom of the middle range sits near 16%.

Extensions themselves are becoming more common, and a growing share of borrowers are receiving multiple or longer extensions rather than a single short-term fix.

Here's why that matters for collections strategy specifically: at a 16-25% rate, a large share of every payment a borrower makes goes straight to interest rather than principal. That stretches out the effective life of the loan, increases total interest paid, and means an extension that looks like relief on paper often just delays the same delinquency event by a few months, at a higher total cost to both the borrower and the lender. A portfolio full of extended, high-rate below-prime auto loans is, in practice, a portfolio of accounts sitting one missed payment away from re-entering the delinquency curve at a worse starting point than before.

This is precisely the kind of stress an early-intervention, behaviorally-aware collections strategy is built to catch before it compounds, not after.

What Are the First Steps to Take With a Past-Due Loan?

For borrowers:

Get the real picture. Pull exact due dates, accrued fees, and total past-due amount, ideally from a centralized source like AnnualCreditReport.com.

Call the lender first, not last. Ignoring notices is the single most expensive mistake in this entire guide. Lenders would rather negotiate than write off the balance.

Don't borrow your way out of it. New debt, or a high-rate extension, to cover an old delinquency almost always compounds the problem, as the below-prime auto data above makes clear.

For lenders and collections teams:

The equivalent move is structural, not tactical: build intervention into the 15-60 DPD window before it ages into the 60+ DPD bucket where recovery economics collapse. This is precisely the stage legacy collections infrastructure was never built to handle well, and it's exactly where agentic AI platforms are now proving their case.

How AI Collections Platforms Recover Delinquent Loans

Most "AI collections" marketing oversells the AI and undersells the architecture problem it's actually solving. Traditional infrastructure was built for the easiest 90% of accounts, borrowers who intend to pay and just need a frictionless nudge. That model breaks completely the moment an account crosses 60 or 90 days past due, or, as the auto loan data shows, the moment an extension at 20%+ interest quietly resets the clock.

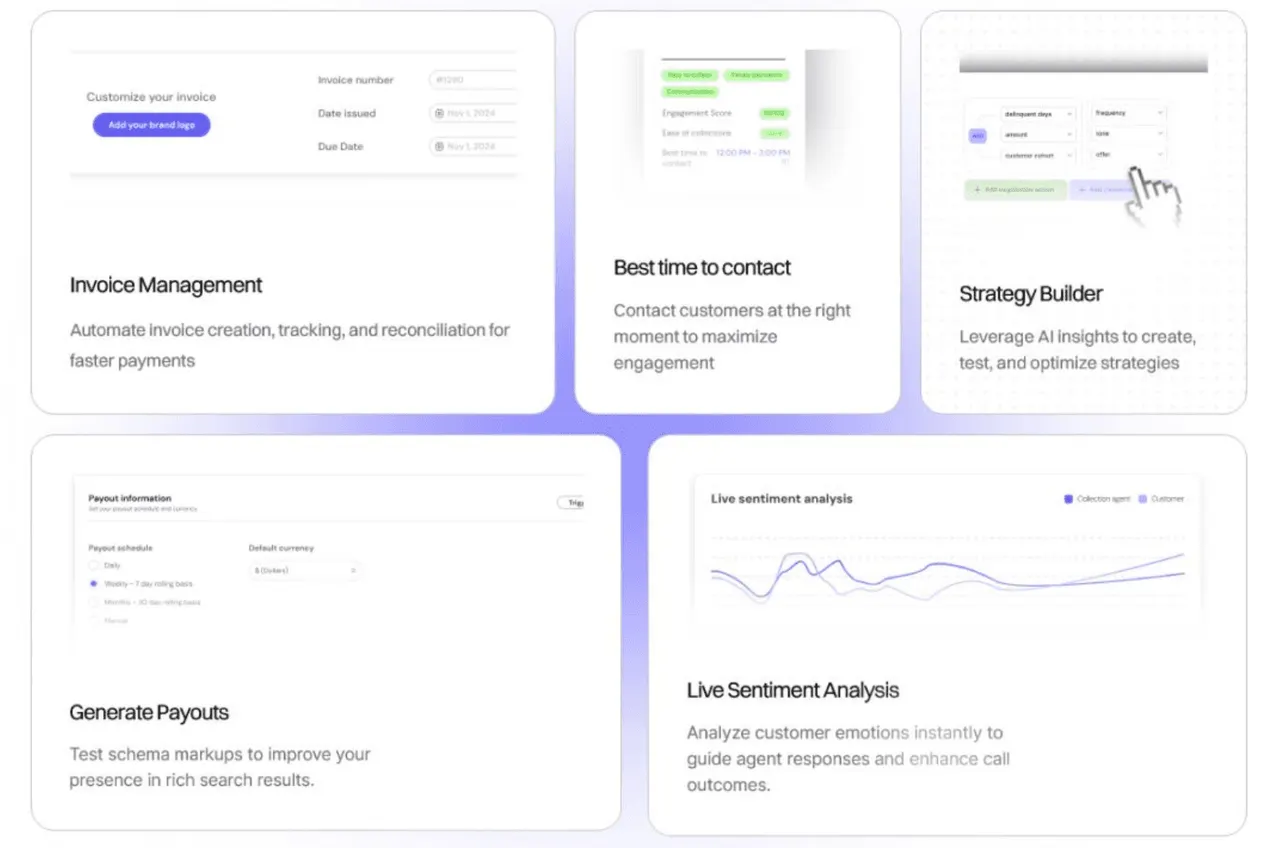

FinanceOps' Agentic AI platform was built specifically to close that gap. The honest version of "how" comes down to six mechanisms working together, not one clever chatbot:

Best time, best channel, best person to contact: Analyzing behavioral patterns, repayment history, engagement, and device signals to predict exactly when, where, and whom to reach. This is the mechanism behind moving right-party contact rates from the ~2% industry norm to 12-15%, a 6-7x multiplier on every downstream metric.

Live sentiment analysis: Scoring tone, hardship cues, payment intent, and compliance risk across every SMS, email, chat, and Voice AI exchange in real time, and shifting tone automatically between empathetic and direct depending on the signal.

Two-way, omnichannel, multilingual communication: Conversational context that persists across SMS, email, Voice AI, webchat, and self-service portals, with native multilingual support so linguistically diverse portfolios aren't quietly failing before a real conversation happens.

User-controlled strategy builder: Collections, servicing, and payments teams define every operational rule, tone threshold, contact cadence, escalation workflow, and compliance limit under TCPA, FDCPA, and CFPB Regulation F. The AI executes inside those boundaries with zero deviation, and every action is timestamped and audit-ready.

Affordability-based flexible payment plans: Evaluating actual repayment capacity rather than offering a flat percentage of balance, which matters enormously in a market where extensions are already running at 16-25% interest and borrowers can't absorb another unaffordable structure.

Automated invoice management: Issuance, behaviorally-timed reminders, retry logic, reconciliation, and audit-ready compliance logging running as a closed system with no manual handoff.

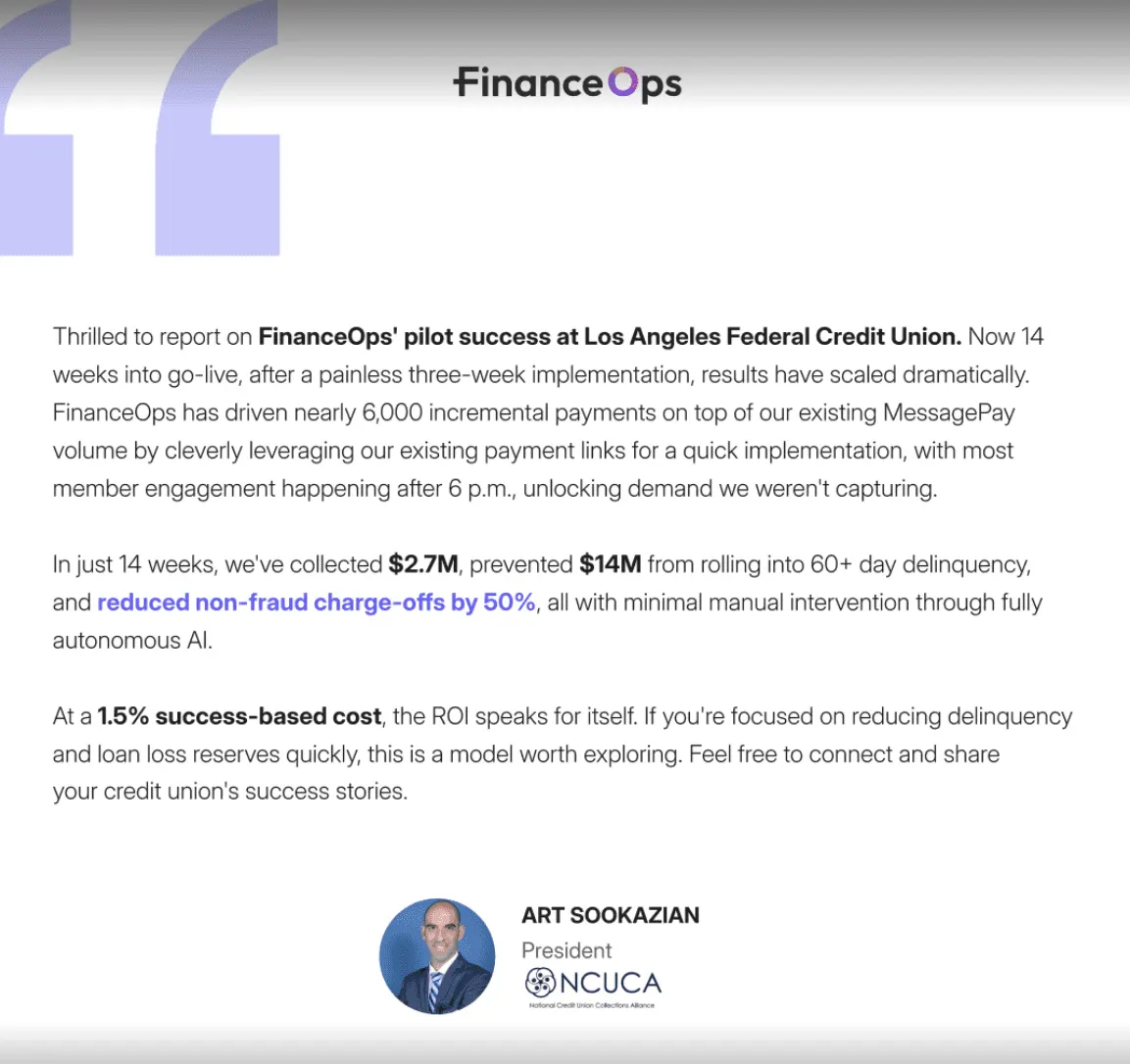

LA Federal Credit Union x FinanceOps Agentic AI

When LA Federal Credit Union deployed FinanceOps Agentic AI across its 15-60 DPD window, results showed up inside the first three weeks:

30-60 DPD delinquency balance fell from roughly $12M to $3.8M, a 65%+ reduction

Approximately 1,650 early-stage payments processed

Right-party contact rate rose from ~2% to 12-15%

48% recovery rate, with under 10 minutes of human effort per day

Only 6 cases out of 1,650+ payments required human specialist review

100% FDCPA-compliant operations across every interaction, from day one

The headline number isn't the dollar figure. It's the six cases requiring human review out of 1,650 payments. That ratio is what governed automation is supposed to look like.

Six AI Collections Platforms Worth Knowing in 2026

If you're evaluating vendors, here's an honest, non-exhaustive snapshot of where the category stands. FinanceOps Agentic AI, leads this list because of the live, auditable deployment data above; the rest are included for comparison context.

FinanceOps Agentic AI: Purpose-built for the 15-60 DPD early-recovery window. Combines best-time/best-channel/best-person targeting, live sentiment analysis, a user-controlled strategy builder, affordability-based payment plans, and automated invoice management in one closed loop. Pricing is performance-based at 1.5%, paid only on successful collections. Best fit for lenders who want governed automation with a documented, FDCPA-compliant track record rather than a black-box promise.

Floatbot.AI: An omnichannel conversational agent platform aimed at touchless account resolution across voice, SMS, WhatsApp, email, and web chat, with built-in compliance controls and human escalation that carries full conversation context to the live agent.

Veritus: Focused on application-funnel outreach and early-stage delinquency engagement, with a dual-agent structure where one agent handles the conversation and a second monitors it for compliance and sentiment.

Kompato AI: A licensed collection agency model that pairs virtual assistants with a 360-degree account analysis approach, adjusting outreach channel and timing based on prior response patterns.

Sedric AI: A compliance-first layer that monitors interactions across channels in real time and flags potential regulatory issues to human agents rather than running the borrower conversation itself.

CollectWise: Geared toward late-stage and pre-legal collections, analyzing debtor records to structure settlement offers and, where needed, routing unresolved accounts toward attorney involvement.

How to Choose

Start by eliminating anything that fails on two non-negotiables: a vendor with no compliance controls built into the platform itself, and one with no human-agent fallback. Either gap alone should end the conversation. From there, evaluate what's left against four practical criteria:

Verification first: The system confirms it's talking to the right person before it takes any action, not after.

Real integration: It connects natively to your existing CRM and payment systems, rather than requiring manual exports or a parallel workflow.

Closed-loop reporting: Every interaction flows back into your system of record at the individual level, not as a summary dashboard you have to reconcile yourself.

Human-owned strategy: Your team sets the policy, the tone thresholds, and the escalation rules. The model executes within those boundaries; it doesn't set them.

That last point is the one worth holding firm on. A vendor that lets the model make policy calls on its own isn't offering you control, it's offering you a black box with better UX.

Key Takeaways

Delinquency and default are different clocks, and confusing them costs money. Delinquency starts the day a payment is missed; default takes 90 to 270 days depending on loan type. The gap between them is the entire window where recovery is still cheap, and most lenders waste it by treating delinquency like a single event.

Waiting has a real, rising price. Cost to recover rises exponentially, not linearly, after 60 DPD, and the below-prime auto data through May 2026 makes the same point in dollar terms: a 21% median rate on extended loans, with the upper band near 25%, means extensions are increasingly a delay tactic, not a fix.

Right-party contact is the multiplier that decides everything else. AI collections platforms don't replace strategy, they execute a human-defined one at scale, and the entire case for them rests on moving contact rates beyond the ~2% industry norm. A platform that doesn't move that number isn't solving the actual problem.

See What This Looks Like for Your Portfolio

Book a free 20-minute walkthrough with FinanceOps Agentic AI and see exactly where your collections infrastructure is creating avoidable delinquency exposure, using your accounts, not a generic deck.

No upfront cost. Performance-based pricing at 1.5%. You pay only on successful collections.

FAQs

1. What is considered a delinquent loan?

A loan becomes delinquent the moment a scheduled payment is missed, not 30 days later. Most lenders simply wait until ~30 days past due to report it to credit bureaus, which is why people conflate "delinquent" with "30 days late." Technically, day one already counts.

2. How many days late is a loan delinquent vs. in default?

Delinquency starts immediately. Default takes substantially longer and depends on loan type: roughly 90 days for personal loans and mortgages, 270 days for federal student loans. The gap between the two is the entire recoverable window.

3. Can a delinquent loan be removed from a credit report?

Not on request. A delinquent account typically stays on a credit report for up to seven years from the original delinquency date. The only legitimate path to early removal is a successful dispute proving the entry was reported in error.

4. What happens if I default on a loan?

Consequences depend on loan type: secured loans (auto, mortgage) can lead to repossession or foreclosure; unsecured loans typically move to collections or legal action. Federal student loans add unique consequences, including offset of tax refunds and Social Security payments.

5. How does AI improve delinquent loan recovery rates?

By predicting the best time, channel, and contact for each borrower, adjusting tone in real time based on sentiment, and offering affordability-based payment plans instead of fixed schedules. In live deployments, this has moved right-party contact rates from ~2% to 12-15% and produced double-digit recovery rate gains within weeks, not months.